ISM Manufacturing to Steer Sentiment Before RBA, BoE Meetings – Action Forex

Trading was subdued in Asia today, with Japan closed for a public holiday and investors awaiting a series of major events later in the week. Aussie led mild gains, supported by positioning for a hawkish hold from the RBA on Tuesday. The British Pound, by contrast, stayed on the defensive as traders reduced exposure ahead of the BoE’s policy decision.

For the RBA, consensus is unanimous that the cash rate will remain at 3.60%, and last week’s upside inflation surprise has raised speculation that Governor Michele Bullock will sound more vigilant on price pressures. The market narrative has shifted from expecting cuts next year to debating how long the RBA would hold its restrictive stance, giving the Aussie an undercurrent of support into the meeting.

Sterling’s tone was softer as uncertainty lingered around the BoE’s Thursday announcement. While the majority expects a steady hold at 4.00%, a small but notable minority — including Goldman Sachs and Barclays — are calling for a 25-bp cut. That divergence has left traders reluctant to buy Sterling aggressively, preferring to hedge against the risk of a dovish surprise amid fragile U.K. growth prospects and fiscal strain.

Dollar opened the week on solid footing after ending October stronger, but the next few days could prove pivotal. A trio of key private-sector releases — ISM Manufacturing today, followed by ISM Services and ADP employment on Wednesday — will help gauge the economy’s resilience following the Fed’s hawkish cut last week. Robust readings could reinforce the case for the Fed to stay cautious into December, keeping yields elevated and Dollar supported.

Asian equities were mixed. South Korea’s KOSPI surged to another record high, brushing off a dip in its manufacturing PMI from 51.2 to 50.6, thanks to robust trade data showing 3.6% yoy export growth. That contrasted with China, where shares lagged as RatingDog PMI and official manufacturing readings both signaled continued softness in factory activity.

For now, traders are content to stay sidelined ahead of event-heavy sessions later in the week. The full market impact of U.S. President Donald Trump’s recent Asia trip and the trade deals announced there may also take time to filter through sentiment. Volatility could return quickly once central banks clarify their tone the policy paths.

In Asia, Japan was on holiday. Hong Kong HSI is up 0.88%. China Shanghai SSE is up 0.31%. Singapore Strait Times is up 0.44%.

China RatingDog PMI manufacturing falls to 50.6; export orders and prices decline

China’s manufacturing activity expanded at a slower pace in October, with the RatingDog PMI easing to 50.6 from 51.2, missing expectations of 50.9. The moderation reflects weaker demand momentum and growing headwinds from global trade tensions, which weighed on both output and new export orders.

According to RatingDog founder Yao Yu, both demand and production expansion softened. Export orders fell “sharply into contraction territory” as heightened trade uncertainty curbed overseas demand. Production growth also cooled, though sub-indices remained in expansion territory. Purchasing activity “slowed significantly”, signaling greater caution among manufacturers heading into year-end.

Price pressures was a drag on profits, as raw material costs rose while finished goods prices fell. Exporters reduced selling prices for the first time since April to stay competitive amid fragile external demand. Still, the survey offered a bright spot: the employment index returned to expansion for the first time since March, reaching its highest level since August 2023.

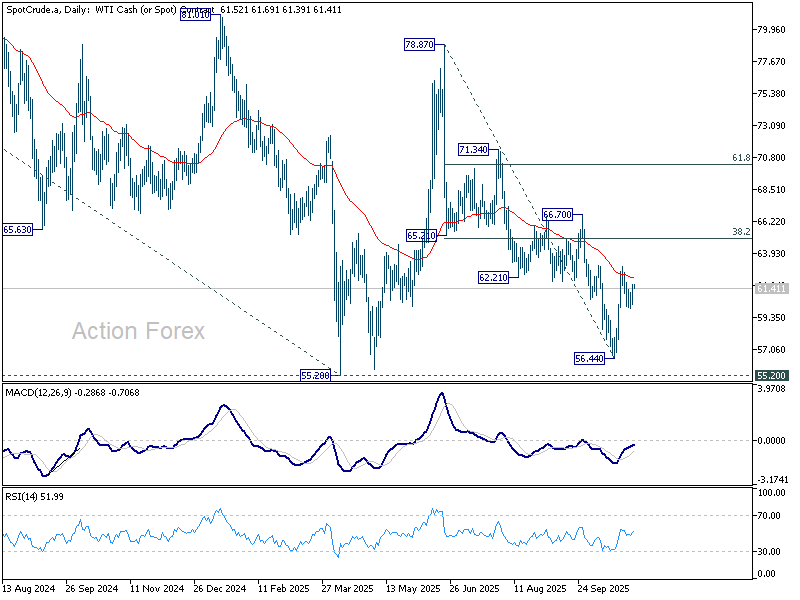

OPEC+ holds Off Q1 increases after Dec hike; WTI eyes rebound toward 65

Oil prices edged higher in Monday’s Asian session as traders welcomed OPEC+’s decision to keep production steady through the first quarter of 2026. The alliance agreed on Sunday to raise December output targets by 137,000 barrels per day — matching the pace set for October and November — but to pause further increases from January to March. The move signals a shift from aggressive supply expansion toward a more cautious approach amid rising uncertainty in global demand and sanctions-related disruptions.

Since April, OPEC+ has raised total output targets by roughly 2.9 million barrels per day, about 2.7% of global supply, but began slowing the pace in October as forecasts pointed to a potential oversupply heading into winter. Sanctions on Russian producers have added fresh uncertainty to the outlook, with Moscow now facing tighter U.S. and U.K. restrictions on Rosneft and Lukoil. These measures could cap Russia’s ability to increase exports.

By opting for a pause, the group is effectively protecting prices and projecting unity at a time when market confidence is fragile. The decision also reflects seasonal realities — January through March is typically the weakest quarter for global oil demand — giving the alliance time to assess the full impact of sanctions and global inventory trends before deciding on its next steps.

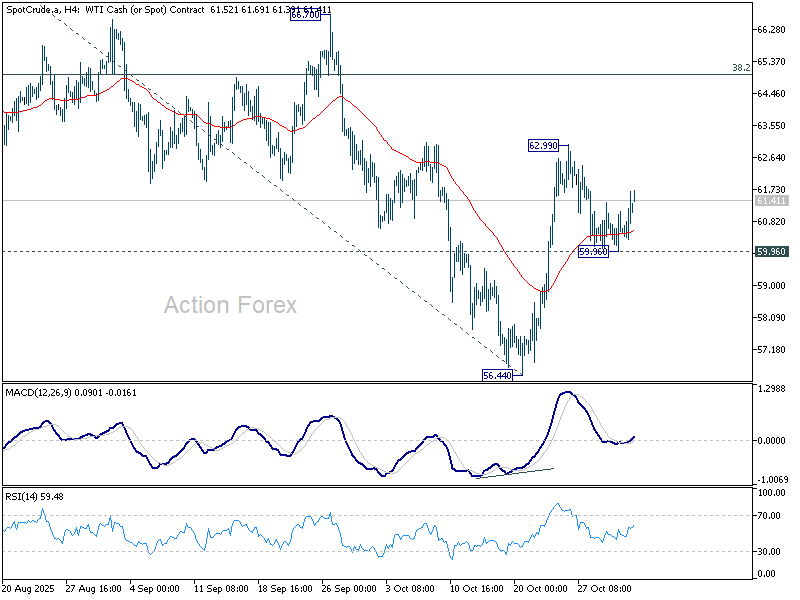

Technically, WTI crude’s decline from 78.87 appears to have completed at 56.44, holding comfortably above 55.20 (2025 low). The structure suggests that the drop was corrective, as the second leg of the pattern from 55.20.

The is room for extended rebound while 59.96 support holds. Break above 62.99 would target the 38.2% retracement of 78.87 to 56.44 to 65.00.

Failure to hold above 59.96, however, would imply renewed downside momentum and the risk of another test of the 55.20 zone before forming a lasting bottom.

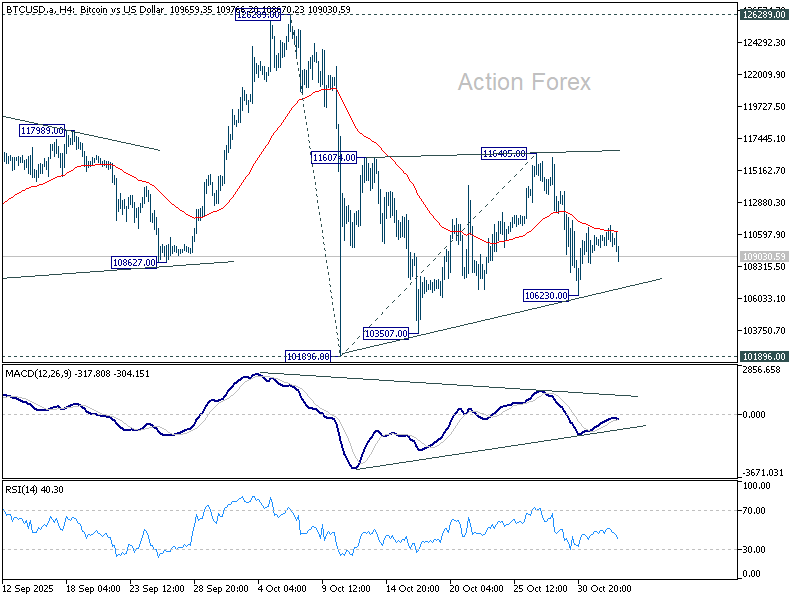

Bitcoin correction to extend after snapping “Uptober” streak

Bitcoin softened in Monday’s Asian session, with sellers gradually regaining control after October ended on a sour note for the bulls. The cryptocurrency lost roughly 5% last month — its first negative “Uptober” in seven years — despite briefly printing a new record high above 126,000.

Last week’s attempted rebound stalled as the Fed’s latest decision delivered a hawkish twist. The 25-bp rate cut came with Chair Powell warning that another reduction in December was “not a foregone conclusion,” a remark that revived Dollar strength and curbed appetite for risk assets, including crypto.

Some optimists argue that the traditional October crypto rally may simply be delayed rather than cancelled, but current technical signals are not supporting that view.

The consolidation pattern from 101,896 appears to have completed in three waves up to 116,405, suggesting that the decline from 126,289 is ready to resume. A drop through 106,230 would confirm renewed downside momentum, opening a move toward 101,896 initially.

Decisive break below 101,896 would extend losses toward the 55 W EMA (now at 98,964) — the line in the sand for preserving the longer-term uptrend from 15,452 (2022 low).

RBA and BoE set to stand pat as markets seek guidance

Markets head into the first week of November braced for another busy stretch dominated by central banks and key data releases. The RBA and the BoE will both meet this week, and while no policy changes are expected, the tone of their communications could shape market expectations into year-end. Investors will also parse incoming data from North America, Europe, and Asia to gauge the global economic trend after a volatile October.

In Australia, Tuesday’s RBA meeting takes center stage after the upside shock in Q3 CPI, which dashed near-term rate-cut bets. Inflation’s re-acceleration was a clear warning that domestic price pressures was stronger than policymakers had anticipated. For Governor Michele Bullock, the task now is to balance the still-soft labor market against the renewed inflation concern — a dynamic that likely keeps the cash rate anchored at 3.60 % for longer.

According to a Reuters poll conducted October 29–30, all 34 economists expect the RBA to hold rates steady this week. Major local banks ANZ, CBA, NAB, and Westpac also see no move in December. The median forecast calls for just one cut by mid-2026, to around 3.35 %, though opinions remain split: twelve see 3.35 %, six project 3.10 %, and ten expect no change at all. Markets will listen closely to Bullock’s remarks for clues on how firmly she views inflation as the dominant risk.

The BoE is likewise expected to stand pat at 4.00 %. In the latest Reuters poll, 87 % of economists anticipated no change this week, and just over half see rates staying on hold through year-end. That marks a clear shift from a month earlier, when nearly 70 % of respondents expected at least one cut this quarter. A small minority still pencil in a 25-bp reduction by December, but with fiscal clouds gathering over Westminster, caution prevails.

Looking further ahead, a slim majority of forecasters see the Bank Rate drifting to 3.75 % by March 2026 and 3.50 % by mid-year, yet such projections remain highly tentative. The Autumn Budget later this month is the wild card: any combination of tighter fiscal measures or fresh spending could quickly alter the BoE’s reaction function. As always, the vote split will be closely watched to gauge how divided the MPC remains after months of internal debate over the pace of easing.

With Washington’s government shutdown still blocking official data releases, traders will turn to private-sector indicators to assess the U.S. outlook. Key reports include ISM manufacturing and services PMIs, ADP employment, and University of Michigan sentiment and inflation expectations. The ADP print in particular will be crucial for a labor-market pulse check as the Fed weighs whether weakness seen in summer hiring has persisted.

Elsewhere, attention will fall on labor figures from Canada and New Zealand. After cutting rates last week, the BoC signaled confidence that policy is now “about the right level,” but August’s shock GDP contraction underscored lingering fragility. A solid October jobs report would help validate the Bank’s upcoming pause and give policymakers breathing space to evaluate tariff impacts and domestic momentum.

In New Zealand, the RBNZ’s 50-bp cut last month has started to show tentative results: business confidence ticked higher and early indicators suggest stabilizing sentiment. Still, officials need hard evidence that these “green shoots” are translating into real activity. A constructive employment print this week would support the view that the easing cycle is nearing its end.

Beyond that, markets will watch Swiss CPI, Japan’s labor cash earnings data, and China’s Caixin and RatingDog PMIs.

Here are some highlights for the week:

- Monday: China RatingDog PMI manufacturing; Swiss CPI, PMI manufacturing; Eurozone PMI manufacturing final; UK PMI manufacturing final; US ISM manufacturing.

- Tuesday: Japan PMI manufacturing final; RBA rate decision; Canada trade balance.

- Wednesday: New Zealand employment; Japan BoJ minutes; China RatingDog PMI services; Germany factory orders; Eurozone PMI services final, PPI; UK PMI services final; US ADP employment, ISM services.

- Thursday: Japan labor cash earnings; Australia trade balance; Germany industrial production; Swiss unemployment rate; UK PMI construction, BoE rate decision; Eurozone retail sales; Canada Ivey PMI.

- Friday: Japan household spending; China trade balance; Germany trade balance; Swiss foreign currency reserves; Canada employment; US U of Michigan consumer sentiment.

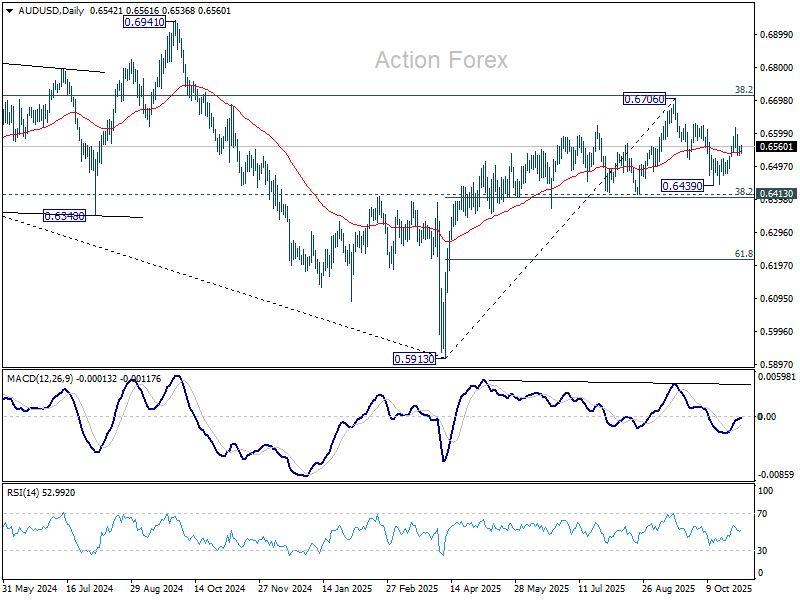

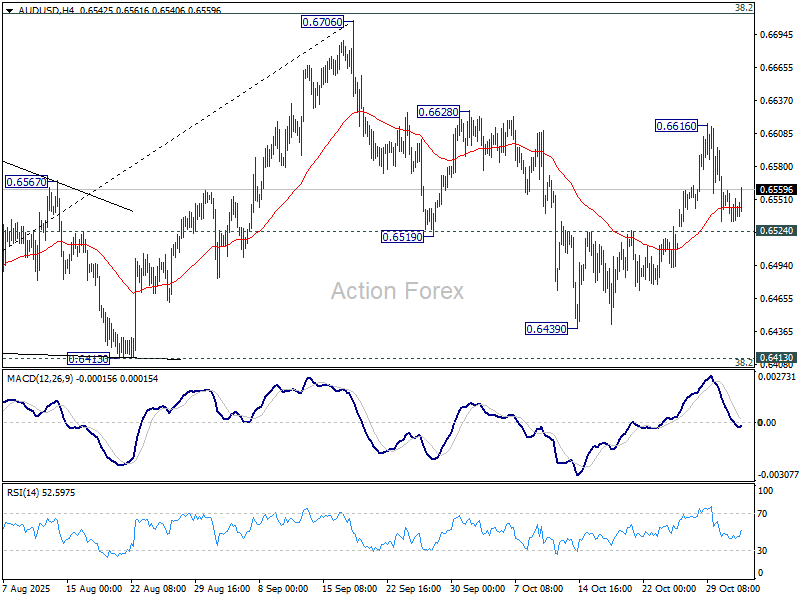

AUD/USD Daily Report

Daily Pivots: (S1) 0.6532; (P) 0.6546; (R1) 0.6559; More...

AUD/USD recovers ahead of 0.6524 resistance turned support but stays well below 0.6616. Intraday bias remains neutral for the moment. On the upside, break of 0.6616 will resume the rise from 0.6439 to retest 0.6706 high. However, break of 0.6524 will turn bias to the downside for 0.6439 and possibly below, to extend the corrective pattern from 0.6706 with another falling leg.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.