Sterling Slightly Firmer After Tight BoE Hold; Dollar Eases Broadly – Action Forex

Sterling traded mildly higher following the BoE’s decision to keep interest rates unchanged at 4.00% in a tight 5–4 vote. Overall market reaction was modest as the Pound gained slightly against the Dollar but lacked strong momentum, as traders viewed the decision and accompanying remarks as broadly balanced.

At the post-meeting press conference, Governor Andrew Bailey emphasized that future policy adjustments would hinge on two key factors: the persistence of inflation and the degree of slack in the economy. He noted that inflation remains “well above the Bank’s 2% target” and warned that price expectations could stay elevated, keeping inflation higher for longer. At the same time, he acknowledged that economic activity is running below potential, with falling vacancies and stalling employment growth signaling softer demand.

Bailey added that the Bank will have access to more data on inflation and cost pressures before the next MPC meeting in December. Importantly, policymakers will also be able to assess how the upcoming Budget — expected to deliver a contractionary fiscal impulse — will affect the economic outlook and inflation path.

Elsewhere, Dollar weakened broadly, retracing part of this week’s advance. There was no single catalyst for the decline, though traders appeared to be unwinding long Dollar positions after a string of U.S. data releases, including ISM surveys and ADP employment, failed to provide a clear directional signal.

Fed funds futures continue to price a roughly 67% chance of a December rate cut, keeping monetary expectations anchored for now. U.S. equity futures point to a flat Wall Street open, reflecting a cautious tone too.

In weekly performance terms, Japanese Yen remains the strongest currency, followed by Dollar and Euro. Kiwi is at the bottom, trailed by Loonie and Aussie. Swiss Franc and Sterling sit in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.17%. DAX is down -0.18%. CAC is down -0.54%. UK 10-year yield is down -0.016 at 4.449. Germany 10-year yield is down -0.002 at 2.675. Earlier in Asia, Nikkei rose 1.34%. Hong Kong HSI rose 2.12%. China Shanghai SSE rose 0.7%. Singapore Strait Times rose 1.54%. Japan 10-year JGB yield rose 0.017 to 1.684.

BoE holds at 4.00% in 5–4 vote, inflation peaked, risk more balanced

The BoE held its Bank Rate steady at 4.00% today, as expected, but the 5–4 vote split revealed persistent pressure within the Monetary Policy Committee to continue easing. Governor Andrew Bailey and four others — Megan Greene, Clare Lombardelli, Catherine Mann, and Huw Pill — voted to maintain the current rate. Sarah Breeden, Swati Dhingra, Dave Ramsden, and Alan Taylor backed a 25bps cut. The close decision underscores a deeply divided committee as policymakers weigh the trade-off between disinflation progress and weakening demand.

In its accompanying statement, the BoE acknowledged that headline CPI inflation has peaked, while “progress on underlying disinflation continues.” The Bank noted that the risk of persistent inflation has diminished, while the threat from weaker demand has become more evident — marking a clear shift toward a more balanced risk assessment.

Updated projections painted a mixed picture. The BoE now expects GDP growth of 1.4% in Q4 2025 (down slightly from 1.5%) and the same pace in 2026, before picking up modestly to 1.7% in 2027 and 1.8% in 2028. .

On inflation, the outlook remains largely unchanged: CPI is projected at 3.5% in Q4 2025, easing to 2.5% in 2026 and 2.0% by 2027, with a slight uptick to 2.1% in 2028. The forecasts imply the BoE expects inflation to remain anchored near target in the medium term, providing scope for gradual easing once confidence in disinflation deepens.

Market-implied rates show investors expect the Bank Rate to drift lower toward 3.9% by the end of the year, 3.5% through 2026–27, and 3.6% by 2028.

Eurozone retail sales slip -0.1% mom as non-food demand softens

Eurozone retail sales disappointed in September, falling -0.1% mom, missing expectations of a 0.2% gain. The decline was driven mainly by weaker spending on non-food items, which slipped -0.2%, and a sharp -1.0% drop in automotive fuel sales. Meanwhile, sales of food, drinks, and tobacco were unchanged.

Across the broader EU, retail sales managed a modest 0.1% monthly rise, masking divergent trends among member states. The steepest declines were seen in Lithuania (-1.1%), Latvia and Slovenia (-0.7%), and Italy (-0.6%), while Luxembourg and Malta (+1.7%), along with Estonia (+1.5%) and Slovakia (+1.4%), posted strong rebounds.

Japan wage growth at 1.9%, but real income falls for ninth month

Japan’s real wages declined for a ninth consecutive month in September as inflation-adjusted earnings fell -1.4% yoy, following a revised -1.7% drop in August, extending a contraction streak that began in January.

Nominal wages rose 1.9% yoy, slightly below expectations of 2.0% and well short of the 3.4% increase in consumer prices, which accelerated for the first time since April.

While regular pay rose 1.9% yoy, matching August’s pace, and overtime pay ticked up to 0.6% yoy, these gains were insufficient to offset higher living costs. Special payments, largely seasonal bonuses, rose 4.5% after a -7.8% fall in August, offering some temporary relief.

Japan’s PMI composite finalized at 51.5, price risks intensify

Japan’s PMI Services was finalized at 53.1 in October, slightly below September’s 53.3. PMI Composite edged up to 51.5 from 51.3 as strength in services offset continued weakness in manufacturing.

According to Annabel Fiddes, Economics Associate Director at S&P Global Market Intelligence, the survey signaled “further solid expansion” in services output, though other indicators were “not quite as upbeat.”

New business growth slowed sharply, expanding at its weakest pace in 16 months, and foreign demand remained in contraction. At the same time, inflationary pressures intensified, with both input and output prices rising faster, largely due to higher labor costs. Confidence also softened as firms expressed concern about labor shortages and subdued customer demand.

The main risk now lies in intensifying price pressures in both manufacturing and services, which “will be important to monitor in the coming months”.

RBNZ’s Hawkesby: Slowdown within expectations, not out of the worst yet

RBNZ Governor Christian Hawkesby said the recent deterioration in the country’s labour market was within expectations. Speaking before a parliamentary committee, Hawkesby noted that the rise in unemployment to its highest level since 2016 reflects where the economy stands in the current cycle. “It is hard out there,” he said, adding that the RBNZ expected this period of softness as part of the adjustment following its recent easing moves.

Despite the alignment with forecasts, Hawkesby warned that risks remain elevated, citing a long list of concerns led by global trade fragmentation and intensifying trade wars. He remarked that “we don’t think we’re out of the worst yet,” pointing to persistent global uncertainty that continues to cloud the medium-term outlook.

The Governor also described New Zealand as a multi-speed economy, with regions and industries responding differently to the current slowdown. While some sectors continue to show resilience, others are struggling under higher costs and weaker demand.

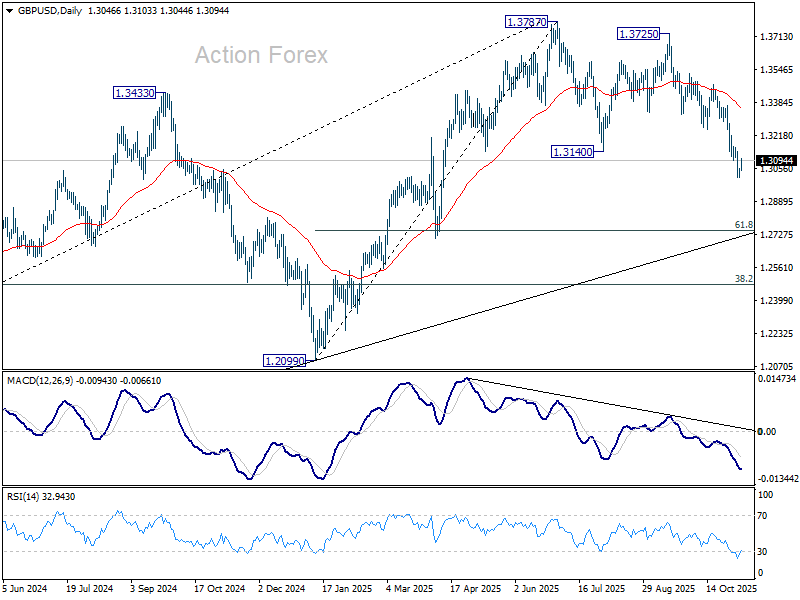

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3023; (P) 1.3038; (R1) 1.3067; More…

GBP/USD’s recovery from 1.3008 temporary extends higher, but stays well below 1.3247 support turned resistance. Intraday bias remains neutral and further decline is expected. On the downside, break of 1.3008 will resume the fall from 1.3787 and target 61.8% retracement of 1.2099 to 1.3787 at 1.2744. Sustained break there will pave the way to 1.2099 support next.

In the bigger picture, the break of 55 W EMA (now at 1.3185) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2780) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.