Loonie Lifts on Strong Jobs Data as Global Risk Mood Stays Sour – Action Forex

Canadian Dollar firmed sharply in early U.S. session after a surprisingly strong set of October employment figures. While the gains were largely driven by part-time positions, the sheer magnitude of the increase — a second consecutive month of robust job creation — underscores that momentum is returning to the Canadian economy even amid lingering trade-related headwinds.

For the BoC, today’s data should come as a welcome relief. It suggests the economy is regaining traction after months of tariff-induced uncertainty, and that further near-term monetary stimulus may not be necessary. The employment resilience aligns with Governor Tiff Macklem’s recent remarks that interest rates are now “at the right level” for policymakers to pause and assess how structural adjustments from trade frictions unfold.

Beyond Canada, global market sentiment remains broadly cautious. Risk aversion continues to dominate, with equity weakness extending from Asia into Europe. The tone remains fragile following renewed concerns about an extended correction in technology and AI-linked stocks, which triggered sharp declines earlier in the week.

Major European indices are trading lower, mirroring losses in Asia. At the time of writing, FTSE is down -0.78%, DAX -0.98%, and CAC -0.47%, while government bond yields are slightly higher, with UK 10-year gilt yield rising to 4.48% and Germany’s bund yield at 2.67%. Earlier in Asia, Nikkei fell -1.19%, Hong Kong HSI -0.92%, and China Shanghai SSE -0.25%, with Singapore’s Strait Times the lone gainer, up 0.16%.

In the U.S., futures are pointing to a weaker open while 10-year Treasury yield has climbed back above 4.1%. The next test for sentiment will be whether the AI selloff that began earlier in the week continues to gather steam into the weekend.

In currency markets, for the week so far, Kiwi and Aussie remain the weakest performers, while the Loonie, though still soft overall, could climb up the ranks if momentum extends. Meanwhile, Yen remains the strongest currency, followed by Euro and Dollar. Sterling and Swiss Franc sit in the middle of the pack.

Canada employment surges 66.6k in October, driven by part-time work

Canada’s labor market surprised to the upside once again in October, as employment jumped by 66.6k, far exceeding expectations of -4k decline. The robust increase followed an already strong 60.4k rise in September, signaling that continuous hiring momentum. Unemployment rate slipped from 7.1% to 6.9%, beating forecasts for 7.2%, while employment rate edged up from 60.6% to 60.8%.

However, the composition of the October gains was less encouraging. The headline strength was largely driven by part-time positions, which rose by 85k, while full-time employment contracted. On a more positive note, private-sector jobs increased by 73k, marking the first rise since June,.

Wage data also showed mild upward pressure, with average hourly pay up 3.5% yoy, accelerating from 3.3% yoy in September.

Fed’s Jefferson: Economy holding up, to proceed cautiously near neutral

Fed Vice Chair Philip Jefferson said in speech today that despite the lack of official data amid the ongoing U.S. government shutdown, private-sector indicators show the overall economy “has not changed much” in recent months. Growth continues at a moderate pace, while the labor market appears to be gradually cooling.

On inflation, Jefferson acknowledged that price growth remains elevated, but he attributed the “lack of progress in headline inflation” largely to tariff effects. He noted that underlying inflation measures continue to “make progress” toward target.

Jefferson reiterated his support for last week’s 25bps rate cut given the shift in risks toward weaker employment. He added that the policy stance remains somewhat restrictive but is now closer to neutral, making it sensible for the Fed to “proceed slowly” from here.

Looking ahead, Jefferson emphasized that future policy decisions will be made on a meeting-by-meeting basis. With the government shutdown likely to continue suppressing key releases before December, “this approach is especially prudent”.

China exports fall -1.1% in October as tariff frontloading fades

China’s trade momentum faltered in October, with exports contracting -1.1% yoy, far below expectations for a 3.0% rise and the weakest reading since February. The figures suggest that the earlier tariff frontloading surge has fully dissipated, exposing underlying fragility in external demand. In particular, shipments to the U.S. tumbled -25.2% yoy, extending a seven-month run of double-digit declines. Exports to the EU inched up 0.9% and to ASEAN gained 8.9%.

Imports increased a modest 1.0% yoy, missing forecasts of 3.2%, as domestic consumption and industrial demand was muted. Purchases from the U.S. fell -23%, underlining the structural damage caused by persistent tariff barriers. Trade surplus stood at USD 90.07 B, reflecting sluggish imports rather than export strength.

The trade figures come amid renewed political friction between Beijing and Washington. Early October saw tensions flare after US President Donald Trump threatened 100% tariffs in response to China’s decision to expand export controls on rare earth metals. A meeting between Trump and President Xi Jinping in South Korea last week helped ease market nerves, resulting in a one-year extension of the bilateral truce that had been due to expire on November 10.

Still, the truce provides only limited near-term relief. U.S.-bound Chinese exports continue to face average tariffs of about 45%, well above the profit-neutral level of 35% identified by analysts.

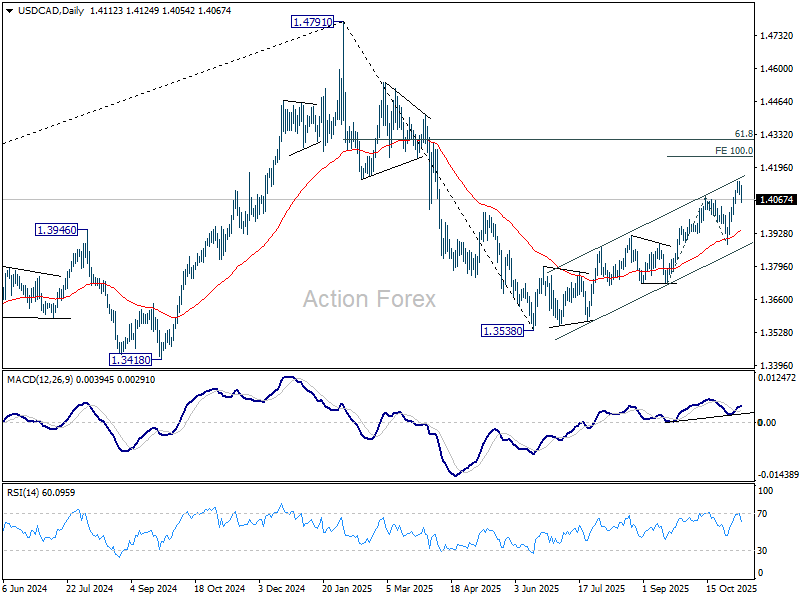

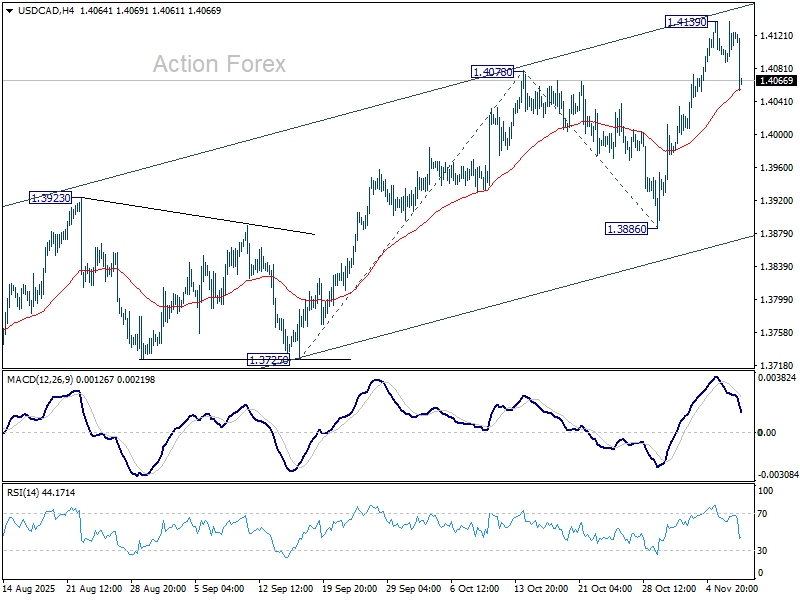

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.4091; (P) 1.4116; (R1) 1.4141; More…

USD/CAD dips notably in early US session but stays above 55 4H EMA (now at 1.4055) so far. Intraday bias remains neutral first. On the upside break of 1.4139 will resume larger rally from 1.3538 to 100% projection of 1.3725 to 1.4078 from 1.3886 at 1.4239. However, sustained break of 55 4H EMA (now at 1.4052) will bring deeper fall back to 1.3886 support instead.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3886 support holds. However, firm break of 1.3886 will revive the case that fall from 1.4791 is indeed a larger scale correction.