Risk-Off Reigns: Tech Selloff, China Trade Miss, and U.S. Layoffs Hit Sentiment – Action Forex

Global markets turned defensive again as risk aversion returned, led by a renewed wave of selling in technology shares. The U.S. tech rout, which rattled Wall Street overnight, spread to Asia, triggering broad weakness across regional equity markets. Japan was hit especially hard, with SoftBank and semiconductor names leading the decline. Traders noted growing anxiety that the earlier AI rally may have reached overbought extremes, prompting profit-taking and algorithmic unwinds.

Additionally, investor nerves were compounded by signs of strain in the U.S. labor market, as well as poor trade data from China. In the US, layoff tracker data showed that over 153k job cuts were announced in October, marking the worst October figure in more than two decades. The sudden spike in layoffs adds to fears that labor market conditions are softening faster than expected, particularly troubling given the absence of key economic releases during the prolonged U.S. government shutdown. The lack of official data leaves policymakers and markets alike flying partly blind.

Meanwhile, China’s October trade report dealt another blow to sentiment. The fading of tariff frontloading has left China’s export engine sputtering, and with U.S. demand constrained by tariffs and sluggish global trade, Beijing now faces the challenge of reigniting domestic demand to fill the gap. Yet, confidence remains fragile, with investors wary that further delays in stimulus rollouts could deepen the slowdown.

Currency markets reflected the risk-off tone, with Yen leading the pack for the week so far, followed by Euro and Dollar. Kiwi remained the weakest, trailed by Aussie and Loonie, while Sterling and the Franc stayed mid-range.

In Asia, at the time of writing, Nikkei is down -1.72%. Hong Kong HSI is down -0.94%. China Shanghai SSE is down -0.06%. Singapore Strait Times is down -0.10%. Japan 10-year JGB yield is flat at 1.684. Overnight, DOW fell -0.84%. S&P 500 fell -1.12%. NASDAQ fell -1.90%. 10-year yield fell -0.064 to 4.093.

China exports fall -1.1% in October as tariff frontloading fades

China’s trade momentum faltered in October, with exports contracting -1.1% yoy, far below expectations for a 3.0% rise and the weakest reading since February. The figures suggest that the earlier tariff frontloading surge has fully dissipated, exposing underlying fragility in external demand. In particular, shipments to the U.S. tumbled -25.2% yoy, extending a seven-month run of double-digit declines. Exports to the EU inched up 0.9% and to ASEAN gained 8.9%.

Imports increased a modest 1.0% yoy, missing forecasts of 3.2%, as domestic consumption and industrial demand was muted. Purchases from the U.S. fell -23%, underlining the structural damage caused by persistent tariff barriers. Trade surplus stood at USD 90.07 B, reflecting sluggish imports rather than export strength.

The trade figures come amid renewed political friction between Beijing and Washington. Early October saw tensions flare after US President Donald Trump threatened 100% tariffs in response to China’s decision to expand export controls on rare earth metals. A meeting between Trump and President Xi Jinping in South Korea last week helped ease market nerves, resulting in a one-year extension of the bilateral truce that had been due to expire on November 10.

Still, the truce provides only limited near-term relief. U.S.-bound Chinese exports continue to face average tariffs of about 45%, well above the profit-neutral level of 35% identified by analysts.

Fed’s Hammack: Policy barely restrictive, inflation still too high

Cleveland Fed President Beth Hammack struck a notably hawkish tone overnight, warning that monetary policy remains only “barely restrictive” after last week’s rate cut. She remains concerned about high inflation and believes policy should continue “leaning against it.” She reiterated her opposition to the Fed’s decision to lower the federal funds rate by 25bps to 3.75%–4.00%.

Hammack said policy should stay “mildly restrictive” to ensure inflation returns to the 2% objective in a “timely fashion” while minimizing risks to employment. She forecast inflation to end the year near 3%, remaining elevated through 2026 before gradually easing back toward target.

On the labor front, Hammack said she does not assign high odds to a downturn, though subdued hiring may point to “more fragility”.

Fed’s Musalem: Policy near neutral, tariff impact on inflation to fade in 2026

St. Louis Fed President Alberto Musalem said overnight that this year’s interest-rate cuts have been “appropriate”, but warned that policymakers must remain cautious about inflation risks. Speaking at an event, he emphasized the need to “lean against above-target inflation while continuing to provide some insurance to the employment sector,” suggesting that while the easing cycle has helped stabilize growth, vigilance is still warranted as inflation remains above 2%.

Musalem described current monetary settings as “somewhere between modestly restrictive and neutral,” noting that financial conditions are now close to neutral and “rather supportive of economic activity and the labor market.”

On inflation drivers, Musalem highlighted U.S. trade tariffs as a lingering source of upward price pressure but said their impact has so far been blunted by corporate pricing restraint. He expects this effect to dissipate in the second half of 2026, paving the way for inflation to resume its gradual return toward the 2% target.

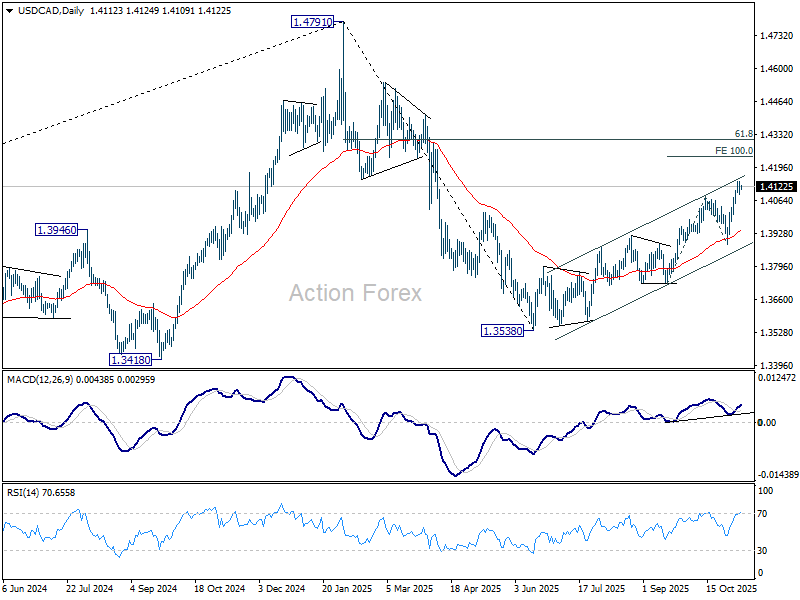

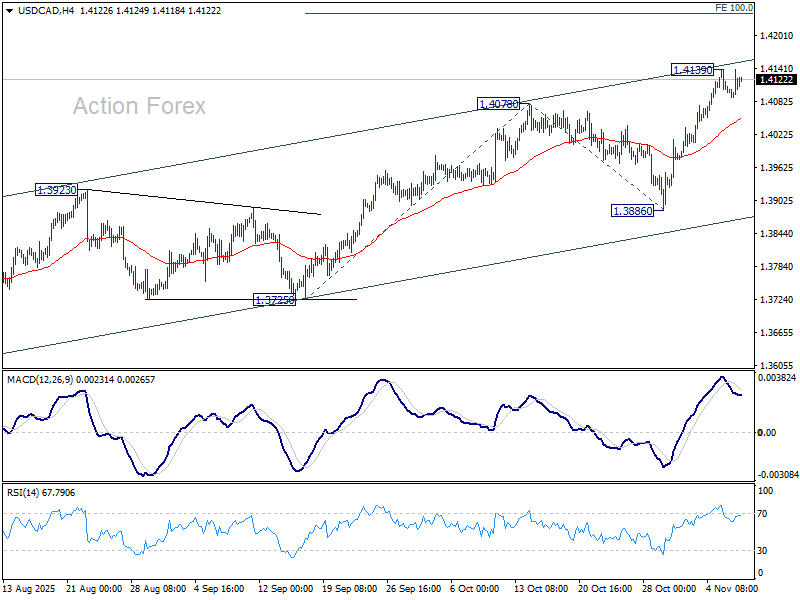

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4091; (P) 1.4116; (R1) 1.4141; More…

Intraday bias in USD/CAD remains neutral and more consolidations could be seen below 1.4139 temporary top. On the upside break of 1.4139 will resume larger rally from 1.3538 to 100% projection of 1.3725 to 1.4078 from 1.3886 at 1.4239. However, sustained break of 55 4H EMA (now at 1.4052) will bring deeper fall back to 1.3886 support instead.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low). Based on current momentum, rise from 1.3538 is the second leg, and a third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3886 support holds. However, firm break of 1.3886 will revive the case that fall from 1.4791 is indeed a larger scale correction.