Dollar Ends Mixed as AI Bubble Fears, US Shutdown, and Tariff Court Case Collide – Action Forex

It was another volatile week in global markets, defined less by fresh data and more by the growing weight of unresolved macro risks. With the U.S. government still in shutdown and a raft of key economic reports missing, investors were left to trade sentiment rather than facts — and sentiment turned sharply negative mid-week.

The standout development was the sudden reversal in technology shares, which reignited talk of a possible AI-driven bubble and reminded investors how dependent this year’s rally has become on a narrow group of market leaders.

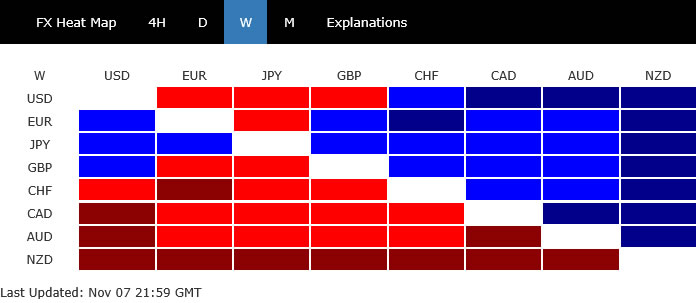

Risk aversion dominated currency trading for most of the week. Kiwi, Aussie, and Loonie sat firmly at the bottom of the performance ladder, all weighed by global risk flows even as their domestic fundamentals diverged.

New Zealand Dollar suffered most after weak labor-market data deepened expectations for another rate cut later this month. Australian Dollar found little comfort in the RBA’s hawkish hold. Investors more focused on fading risk appetite than on policy nuance, even though RBA indicated no more rate hike this year.

Canadian Dollar, meanwhile, lagged early on but found a lifeline in surprisingly strong October employment figures that eased expectations of further BoC easing.

Among the gainers, Yen led the pack, supported by safe-haven demand, though late-week profit-taking erased much of its gains. The Japanese currency’s next moves will likely hinge on how U.S. and European yields evolve in tandem with risk sentiment.

Euro and Sterling rounded out the top three performers, helped by a slightly softer Dollar. BoE narrowly avoided easing in a tense 5-4 vote, but rate cut is still underway after getting more details from the U.K. government’s Autumn Budget later this month. Dollar and Swiss Franc ended in the middle of the pack.

NASDAQ Pullback on AI Fears, But Bulls Still Hold the Line

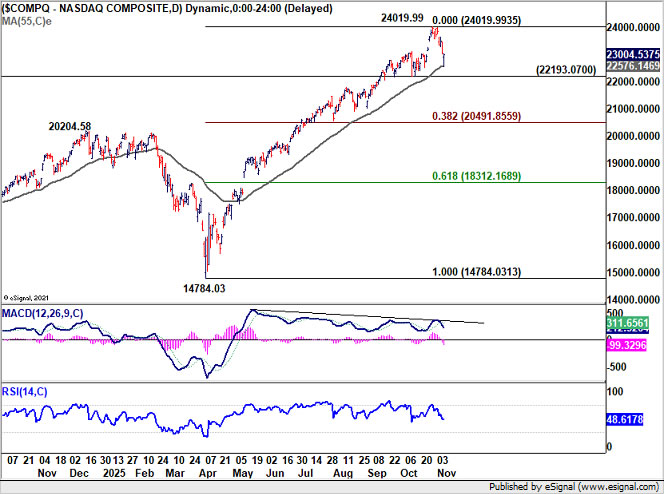

One of the defining stories of the week was the sharp pullback in technology shares, which reignited debate over whether the AI boom has turned from opportunity to overvaluation. The selloff was abrupt and broad, sending NASDAQ down roughly 3% in its worst week since April. S&P 500 and DOW each lost more than 1%, as investors trimmed exposure to crowded positions that had powered this year’s rally.

The correction was triggered less by new data and more by a shift in psychology. Goldman Sachs CEO David Solomon warned that equity markets could face a “likely 10–20% drawdown” over the next two years. His comment added weight to simmering unease that the AI-driven melt-up might have outpaced real earnings growth.

That view was indeed voiced last month by IMF chief economist Pierre-Olivier Gourinchas, who likened the current enthusiasm for artificial intelligence to the late-1990s dot-com frenzy. His warning drew little attention at the time, overshadowed by headlines on trade tensions, the U.S. government shutdown, and shifting central-bank policies. But it has since resurfaced as the AI correction story takes center stage.

Still, the counter-arguments were also loud. Nvidia’s CEO Jensen Huang pushed back, saying the AI cycle remains in its infancy and comparing the current stage to the early internet build-out. “We’re in the beginning of a very long expansion of artificial intelligence,” he said, dismissing bubble talk as premature. For many investors, that remains the dominant view: short-term volatility may purge excess positioning, but the secular story behind AI remains intact.

Technically, NASDAQ’s intraday behavior told a similar story of nervous but orderly profit-taking. The index hit a low of 22,563.41 on Friday—almost exactly at its rising 55 D EMA at 22,576.14, before rebounding to close above 23,000. The swift turnaround hinted at bargain-hunting and short-covering rather than capitulation.

For now, the uptrend from 14,784.03 (Apr low) remains intact. Further rise should still be seen to 100% projection of 10,088.82 (2022 low) to 20,204.58 (2024 high) from 14,783.03 at 24,899.78. But initial resistance should emerge there on overbought condition, or maybe a little higher at 25,000 psychological level, to cap upside on first attempt.

Conversely, decisive fall below 22,193.07 support would signal that the consolidation is maturing into a deeper correction, targeting the 38.2% retracement of 14,784.03 to 24,019.99 at 20,491.85.

Shutdown, Tariff Court Case, and Yield Jitters

Away from the drama in equities, the U.S. macro environment grew more complicated. The federal government shutdown stretched into another week, marking the longest in history, with no sign of political compromise in Washington. The standoff has now begun to show real-world effects, both logistical and psychological, as federal agencies remain shuttered and workers unpaid.

Late in the week, the Senate once again failed to advance competing funding bills. Republicans rejected a Democrat proposal to reopen the government, while Democrats blocked a GOP measure that would have selectively paid active-duty troops and essential personnel. The result is ongoing paralysis — and growing frustration from both markets and the public sector.

The shutdown’s side effects are no longer theoretical. Hundreds of U.S. flights were cancelled or delayed after the administration ordered schedule reductions to ease pressure on unpaid air traffic controllers. Those cuts, currently around 4%, could rise to 10% if no agreement is reached in the coming week. Investors are increasingly wary that prolonged disruption could start to weigh on growth and confidence.

Compounding the uncertainty, the U.S. Supreme Court opened hearings on the legality of President Donald Trump’s reciprocal and fentanyl-related tariffs. The case hinges on whether such tariffs can be justified under emergency powers normally reserved for national security crises.

A ruling against the administration could overturn significant portions of the tariff framework, creating fresh ambiguity for global trade and corporate planning. Equally important is that refund obligations from invalidated tariffs could materially worsen US fiscal arithmetic. Any revenue shortfall, if not offset by spending cuts, might widen the deficit and steepen the Treasury yield curve — with long-term yields rising even as short-term rates fall under Fed easing. The mere possibility has already stirred unease among bond traders.

That dynamic was already visible last week as the U.S. 10-year yield climbed back above 4.1, touching an intraday high of 4.161 before retreating. Technically, the rebound from the 3.947 short term bottom still looks corrective within the broader downtrend from 4.629. Upside should be capped by 4.205 cluster resistance (38.2% retracement of 4.629 to 3.947 at 4.207). That should set the range for more sideway trading between 3.95/4.20 in the near term.

Decisive break above 4.205, however, would send a very different signal — suggesting that fiscal concerns are overtaking disinflation and that a deeper re-pricing in the bond market may be under way.

Dollar Index’s rebound from 92.61 continued last week and hit 100.36. Further rise is still in favor in the near term, but upside should be limited by 38.2% retracement of 110.17 to 96.21 at 101.54. On the downside, break of 98.56 support will indicate that the corrective rebound has completed and bring deeper fall back to 96.21 low.

However decisive break of 101.54 would argue that Dollar Index is already reversing the whole down trend from 110.17. In particular, if 10-year yield breaks through 4.2 mark decisively in tandem, that would add additional tailwind to Dollar Index for an even stronger rally.

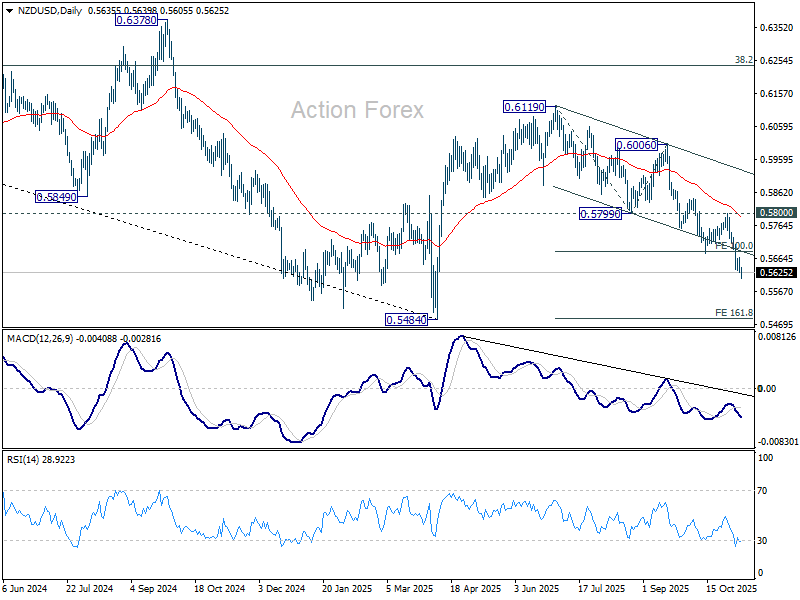

NZD/USD Slide Deepens After Job Data, Pandemic-Era Low Back in Sight

New Zealand Dollar tumbled broadly last week, closing as the weakest performer among major currencies. Global risk aversion remained the dominant drag, but the domestic backdrop offered little to offset it. With labor market momentum stalling and policy expectations leaning dovish, Kiwi continued to lose ground across the board.

The Q3 employment figures were uninspiring. Job growth was flat, and the unemployment rate edged up to 5.3%, its highest level since 2016. While the deterioration was not severe enough to trigger another emergency-sized cut, it nevertheless cemented expectations that the RBNZ will ease by 25 bps to 2.25% at its upcoming meeting.

Whether that move will mark the end of the easing cycle remains uncertain. Much will depend on whether tentative improvements seen in business sentiment surveys can translate into real activity gains over the next two quarters. For now, traders see the odds of another rate cut in 2026 as a coin toss.

Technically, NZD/USD’s fall from 0.6119 continued last week. The strong break of the falling channel support and 100% projection of 0.6119 to 0.5799 from 0.6006 at 0.5687 both indicate downside acceleration. Near term outlook will now stay bearish as long as 0.5800 resistance holds. Next target is the support zone between 0.5484 low and 161.8% projection at 0.5490.

For now, there is little fundamental reason for NZD/USD to collapse through 0.5467 (2020 low) to resume the long term down trend from 0.8835 (2014 high). But the technical risks are growing.

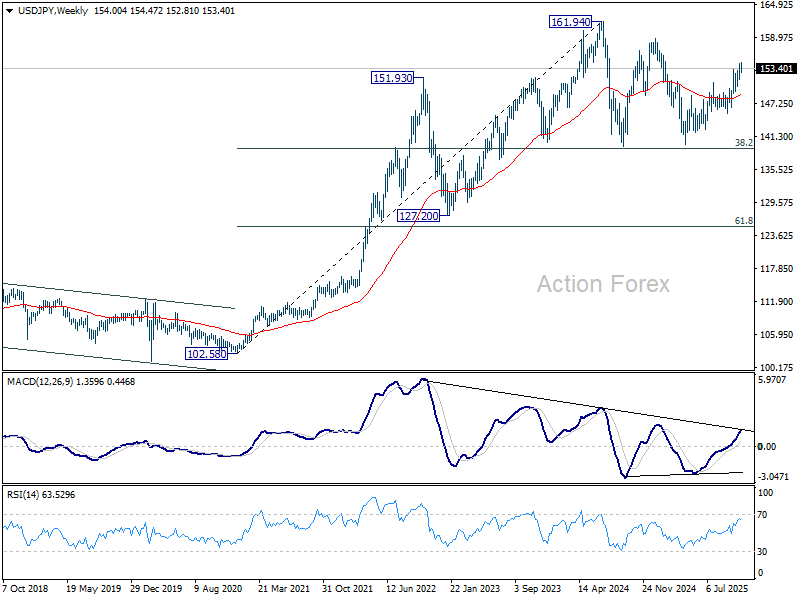

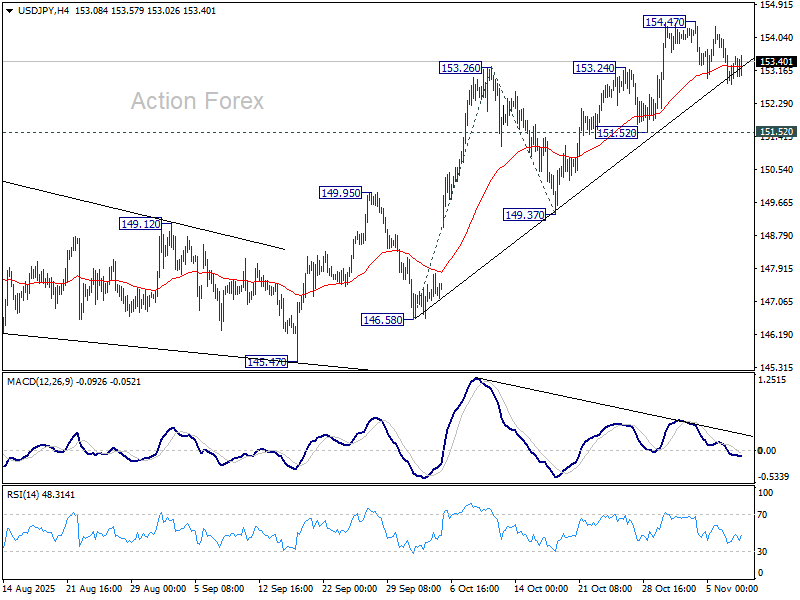

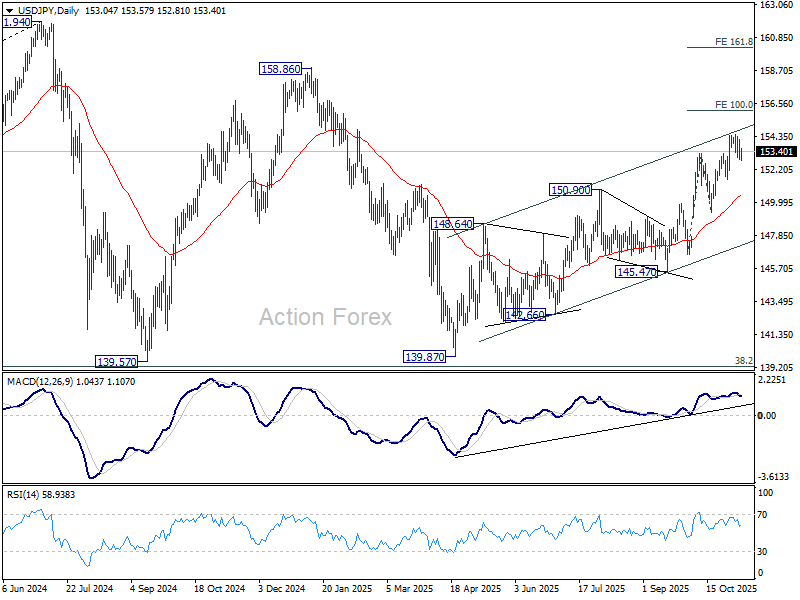

USD/JPY Weekly Outlook

USD/JPY edged higher to 154.47 last week but retreated again. Initial bias remains neutral this week for some more consolidations. Further rally is expected as long as 151.52 support holds. Above 154.47 will resume larger rise from 139.87 and target 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Break there will pave the way to 158.85 key structural resistance.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 149.37 support will dampen this bullish view and extend the corrective pattern with another falling leg.

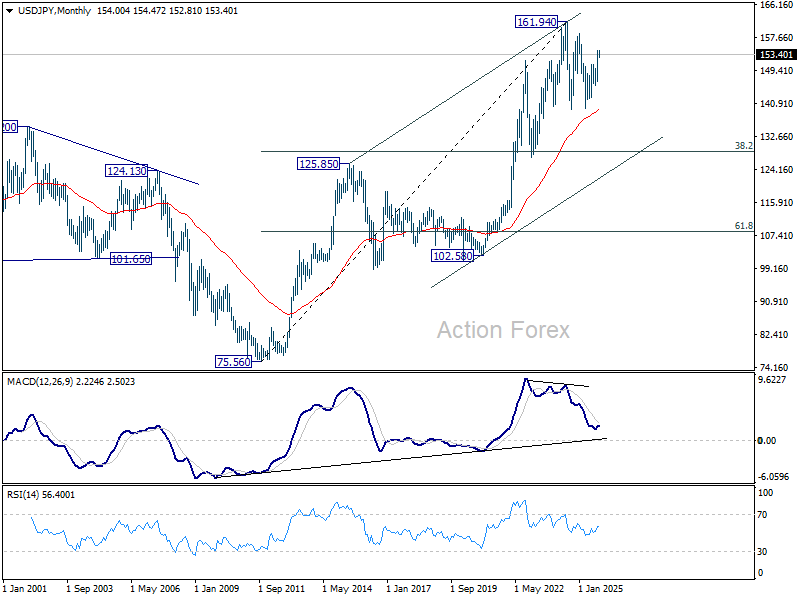

In the long term picture, there is no sign that up trend from 75.56 (2011 low) has completed. But then, firm break of 161.94 is needed to confirm resumption. Otherwise, more medium term range trading could still be seen.