Risk-On Rebound as U.S. Shutdown Nears End – Action Forex

Global risk appetite improved markedly today, with strong gains in Asia carrying over into European trading and U.S. futures pointing higher. Investors found renewed confidence amid signs of political progress in Washington, where the Senate approved the first stage of a bipartisan deal to end the monthslong government shutdown.

The agreement would fund federal operations through January 30 next year and could potentially reverse some of the permanent layoffs that occurred during the 35-day impasse. The development offered a welcome relief to markets reeling from last week’s tech-led selloff, noting that a resolution to the shutdown could restore data flow and remove a key source of uncertainty for investors.

If the Senate’s amended measure clears the House of Representatives and wins President Donald Trump’s signature, the deal would avert further disruptions to federal services and allow normal budget processes to resume. The prospect of restored government operations is also raising hopes that upcoming economic releases will help clarify the Fed’s policy outlook ahead of its December meeting.

The renewed optimism was clearly reflected in the currency markets, where high-beta and commodity-linked currencies led gains. Aussie outperformed, followed by Kiwi and Loonie, as investors re-engaged with risk-sensitive trades.

At the other end of the spectrum, Yen weakened further, extending losses from the Asian session. The currency was weighed by both improved global sentiment and fresh political pressure on the BoJ, after a senior economic adviser to Prime Minister Sanae Takaichi urged policymakers to postpone any rate hike until at least January. His comments reinforced the view that fiscal priorities remain dominant in Tokyo, keeping near-term BoJ tightening expectations subdued.

Swiss Franc also softened as investors rotated out of safe havens, while Dollar traded lower. Meanwhile, Euro and Sterling are trading in the middle.

In Europe, at the time of writing, FTSE is up 0.89%. DAX is up 1.78%. CAC is up 1.34%. UK 10-year yield is up 0.016 at 4.485. Germany 10-year yield is up 0.004 at 2.676. Earlier in Asia, Nikkei rose 1.26%. Hong Kong HSI rose 1.55%. China Shanghai SSE rose 0.53%. Singapore Strait Times fell -0.09%. Japan 10-year JGB yield rose 0.023 to 1.702.

Fed’s Daly: Policy must avoid trading one mistake for another

San Francisco Fed President Mary Daly said the FOMC has appropriately reduced policy rates by a total of 50bps this year as part of a “prudent risk management approach”, noting that the adjustments provide “needed insurance” for the labor market while keeping policy “modestly restrictive” to further curb inflation.

In an essay published today, Daly posed the central question now facing the Fed: Will more rate cuts be needed? She argued that while policymakers must remain alert to inflation risks—drawing lessons from the 1970s and the post-pandemic surge—they must also avoid overcorrecting and stifling growth.

“We don’t want to work so hard to not be the 1970s that we cut off the possibility of the 1990s,” she wrote, warning that an excessive focus on inflation history could trade one mistake for another.

Daly emphasized that getting policy right will require “an open mind” and careful evaluation of evidence on both sides of the debate.

Eurozone Sentix falls to -7.4, growth outlook darkens, debt fears persist

Eurozone investor sentiment deteriorated again in November, reinforcing concerns that the bloc’s economy remains mired in stagnation. Sentix Investor Confidence Index fell sharply to -7.4 from -5.4 in October, missing expectations of -3.9. Current Situation Index dropped to -17.5 from -16.0. Expectations slipped to 3.3 from 5.8.

Sentix said there was “little sign of an autumn upturn” and that the Eurozone “continues to languish, with no signs of momentum for the future.” The survey noted that the persistence of such gloomy assessments points to an ongoing process of contraction, with the path to 2026 seemingly “predetermined” as the economy remains unable to break free from its slump.

Still, one faint positive emerged from the report: inflation concerns eased notably. The Sentix inflation barometer rose 9 points to -11, suggesting investors see central banks acknowledging weak growth conditions and possibly adjusting policy accordingly. However, Sentix warned that ballooning government debt remains a structural problem, keeping the fiscal policy barometer deeply negative at -32 and limiting how far refinancing conditions can realistically fall.

BoJ summary show split narrows as members debate near term rate hike

The BoJ’s Summary of Opinions from October 29–30 meeting revealed a growing consensus among policymakers that conditions are nearly in place for a rate hike. Eight opinions either called for raising interest rates soon or outlined conditions under which borrowing costs should rise in the near term—marking the clearest sign yet that the BoJ is preparing for its next move.

Several members emphasized that while immediate action may not be necessary, the Bank “should not miss the timing to raise the policy interest rate.” Others noted that a hike would likely follow if global economic conditions remained stable and corporate wage-setting momentum was sustained. One view stated that “conditions for taking a further step toward normalizing the policy rate have almost been met,” but stressed the need to confirm that underlying inflation is firmly entrenched.

Still, some members urged caution. One participant argued that the BoJ should take “a little more time” to assess the impact of U.S. tariffs and Japan’s new fiscal direction before tightening policy further. The minutes reinforce market expectations that the Bank is leaning toward a rate increase either in December or early 2026, contingent on wage data and external stability.

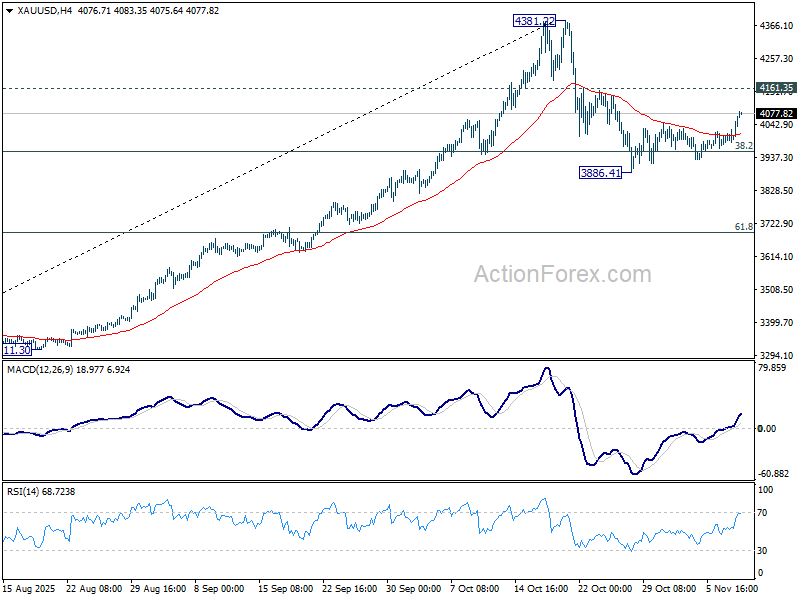

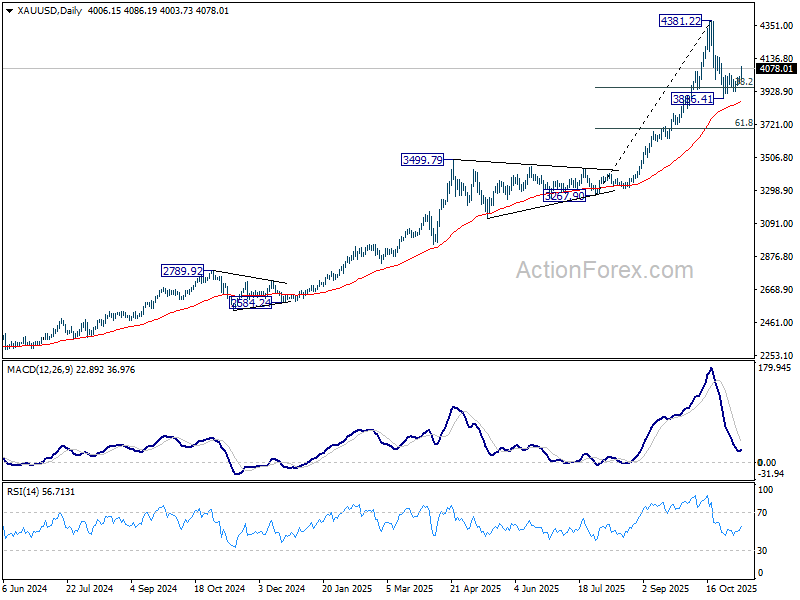

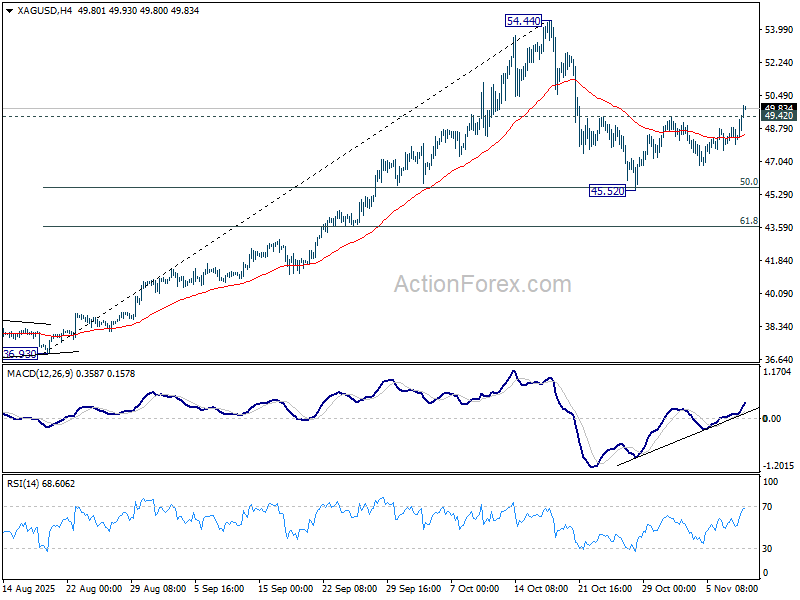

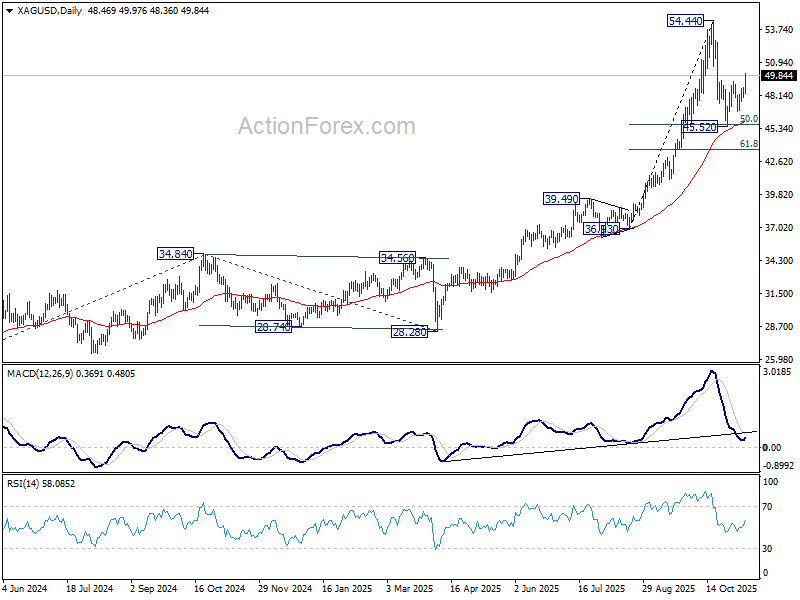

Gold and Silver rebound ahead of 55 D EMAs, first leg of consolidations done.

Gold and Silver advanced sharply today, recovering from recent lows as traders interpreted both technical signals and fresh political developments in Washington as reasons to buy. The rally suggests the first corrective leg from October’s highs may be over, with both metals finding firm support at their moving averages.

The rebound gained a fundamental boost from news that the prolonged U.S. government shutdown could soon end. Reports indicated that centrist Senate Democrats agreed to back a short-term funding bill that would reopen parts of the government through January 30. The agreement, if passed, would restart the flow of federal data—potentially reinforcing market expectations for another Fed rate cut in December.

Renewed rate-cut bets lent support to metals already positioned near key technical floors. Investors also saw the reopening deal as a sign that policy paralysis in Washington may ease, removing one near-term drag on market confidence.

Technically, Gold has broken decisively above its 55 4H EMA, indicating that the pullback from 4,381.22 likely completed at 3,886.41, ahead of 55 D EMA. Decisive break above 4,161.35 resistance would confirm upside momentum toward 4,381.22. However, strong resistance is expected near that level, to bring another fall to extend the consolidation, before the longer-term uptrend resumes.

Silver’s structure shows a similar setup. Its decline from 54.44 seems to have ended at 45.20, ahead of 55 D EMA. Sustained trade above 49.42 resistance would target a retest of 54.44. As with Gold, resistance there should limit gains and set the stage for another short-term retreat—potentially toward 45.52—before the broader bullish trend resumes later.

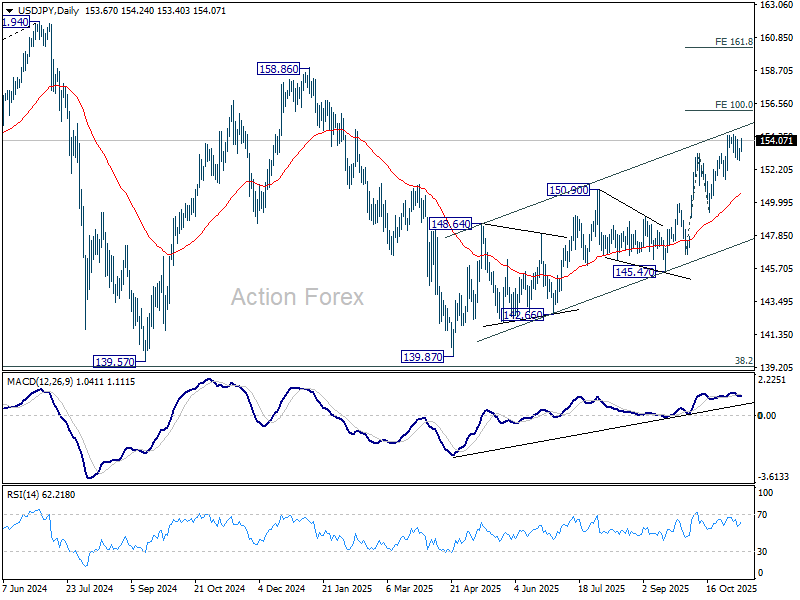

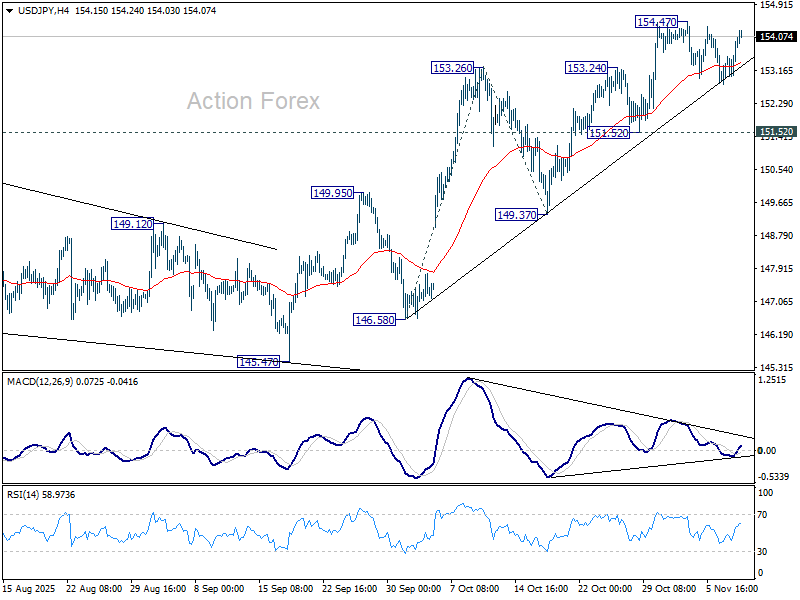

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.97; (P) 153.28; (R1) 153.75; More…

USD/JPY rebounded notably today but stays below 154.47 resistance. Intraday bias remains neutral and more consolidations could still be seen. Further rally is expected as long as 151.52 support holds. Above 154.47 will resume larger rise from 139.87 and target 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Break there will pave the way to 158.85 key structural resistance.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 149.37 support will dampen this bullish view and extend the corrective pattern with another falling leg.