Wall Street Rallies But Asia Cools After Early Lift, Yen Stays Weak – Action Forex

U.S. markets surged overnight after lawmakers in Washington moved closer to ending the country’s record-breaking government shutdown, boosting risk sentiment across equities and commodities. The Senate’s approval of a bipartisan deal eased fiscal uncertainty and restored momentum to Wall Street, where Nvidia, Palantir, and Broadcom led a powerful rebound in technology and AI-linked stocks.

The rebound also marked a sharp reversal from last week’s caution when concerns over stretched AI valuations triggered broad profit-taking. Those fears have quickly taken a back seat, replaced by renewed risk appetite as investors welcomed the prospect of a fiscal resolution and an extended runway for the U.S. economy. Greed, it seems, has once again overtaken fear.

The U.S. Senate on Monday approved a bipartisan compromise to end the country’s longest-ever shutdown, passing the measure by 60 votes to 40 with support from nearly all Republicans and eight Democrats. The agreement would restore funding for government agencies that have been shuttered since October 1 and halt President Donald Trump’s drive to downsize the federal workforce, preventing further layoffs until January 30.

The legislation now moves to the Republican-controlled House of Representatives, where Speaker Mike Johnson has pledged swift action, aiming to pass the bill as soon as Wednesday and send it to the President for signature. The resolution would end a damaging impasse that has frozen public-sector activity and delayed key economic data, paving the way for normalization ahead of the Fed’s December meeting.

Wall Street welcomed the news with conviction. DOW rose 0.81%, S&P 500 climbed 1.54%, and NASDAQ Composite surged 2.27%, powered by strong gains in chipmakers and AI-linked names. Treasury yields inched higher, with 10-year yield up 1.7bps to 4.11. Asian markets, however, offered a more tempered response. Initial gains faded through the session, leaving the region mixed. At the time of writing, Nikkei is down -0.17%, Hong Kong’s HSI -0.35%, and Shanghai’s SSE -0.44%, while Singapore’s Straits Times outperforms with a 1.11% advance.

In currency markets, optimism was more restrained. Aussie led gains for the week so far on improving risk tone, followed by Kiwi and Swiss Franc. Yen remained the weakest performer, pressured by Tokyo’s commitment to maintaining easy monetary conditions, while Euro and Dollar both softened modestly within tight ranges. Sterling and the Canadian Dollar traded mid-pack. Most pairs are still confined within last week’s ranges.

Australia Westpac consumer confidence surges to 103.8, marking end of prolonged pessimism

Australian consumer confidence jumped sharply in November, marking a clear break from years of pessimism. The Westpac Consumer Sentiment Index rose 12.8% mom to 103.8, its first positive reading since early 2022 and the highest in seven years, excluding the brief COVID-era spike. The surge was underpinned by a sharp improvement in views on the economy, with the 12-month and five-year outlook sub-indexes rising 16.6% and 15.3%, respectively—both now well above long-run averages.

Westpac said the result “draws a clearer line” under the prolonged period of consumer strain caused by high inflation, elevated interest rates, and rising tax burdens. The rebound likely reflects stronger domestic momentum, particularly in housing and consumer demand, as well as a more stable external backdrop. The recent de-escalation in U.S.–China trade tensions and a new Australia–U.S. deal on critical minerals have also buoyed sentiment.

The real surprise, according to Westpac, is how decisively these positive forces outweighed lingering worries about inflation and future rate settings. The data suggest households are regaining confidence in Australia’s recovery prospects even as monetary policy remains tight—offering a fresh signal that consumer resilience could help underpin growth heading into 2026.

RBNZ survey points to one more cut, then extended hold through 2026

New Zealand’s inflation expectations remain well anchored, while rate projections signal the RBNZ’s easing cycle is nearing its end.

The latest RBNZ Survey of Expectations showed the mean one-year-ahead inflation expectation edging up slightly to 2.39% from 2.37%. Two-year expectation stayed unchanged at 2.28%. Longer-term views were broadly steady, with the five-year expectation easing to 2.22% and the ten-year measure rising modestly to 2.18%—all consistent with the Bank’s 1–3% target midpoint.

Respondents now see the Official Cash Rate, currently at 2.50% following October’s 50bps cut, at 2.25% by year-end, implying just one more 25bps reduction before policy stabilizes. The one-year-ahead OCR expectation fell sharply to 2.31% from 2.86%, indicating that market participants expect the RBNZ to remain on hold through much of 2026 as inflation trends near target and growth moderates.

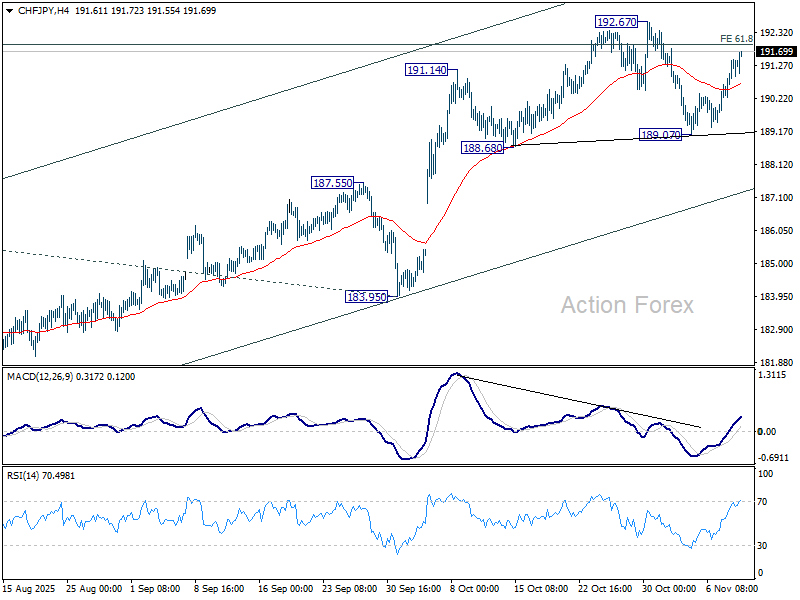

Growth over currency defense: Japan’s low-rate bias to fuel CHF/JPY rally

Yen weakness persisted as comments from Japan’s officials reinforced the view of supporting growth through lower interest rates outweighs concerns about further Yen depreciation.

Economic Revitalization Minister Minoru Kiuchi acknowledged today that a weaker Yen can push up prices prices. However, he also emphasized that “import prices in Yen terms have been falling for eight consecutive months.” The latest BoJ Corporate Goods Price Index showed that annual import price inflation has been negative throughout 2025, except in January. This underlines Kiuchi’s message that the government remains broadly comfortable with current exchange rate trends.

Taken together with recent comments from other officials, Tokyo’s stance appears tolerant of moderate Yen weakness. As long as the moves are not disorderly, authorities seem focused on broader economic stability rather than exchange-rate management.

The stance reflects clear priorities under new Prime Minister Sanae Takaichi, whose administration has emphasized growth and fiscal stimulus over premature monetary tightening. Her economic package leaves little ambiguity as she called it “extremely important” for monetary policy to focus on achieving strong economic growth

Takaichi also explicitly urged the BoJ to reach 2% inflation sustainably through wage gains, not cost-push effects. Her stance effectively discourages early tightening, highlighting that policy coordination now leans toward growth-first rather than currency defense.

This political backdrop makes it increasingly unlikely that Governor Kazuo Ueda will push for a rate hike at the December meeting. While BoJ board members have indicated readiness to tighten if inflation stays resilient, the growing government influence implies that any move may be delayed until early 2026—and that the pace of normalization will remain slow thereafter.

Technically, CHF/JPY’s rebound suggests that the pullback from 192.67 has completed at 189.07. Decisive break above 192.67 would resume the long term uptrend, targeting 100% projection of 173.06 to 186.02 from 183.95 at 196.91.

On the downside, however, firm break of 189.07 support would risk completing a head-and-shoulders top, signaling the end of the five-wave rally from 165.83.

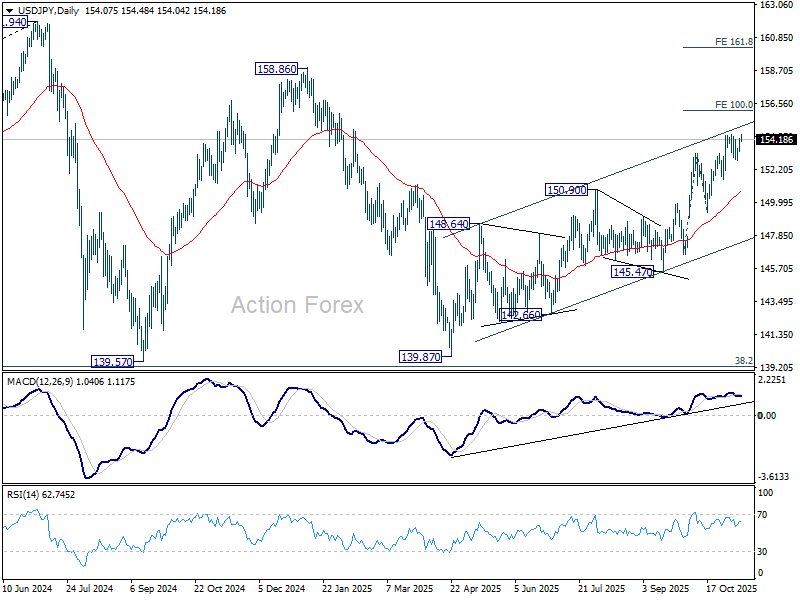

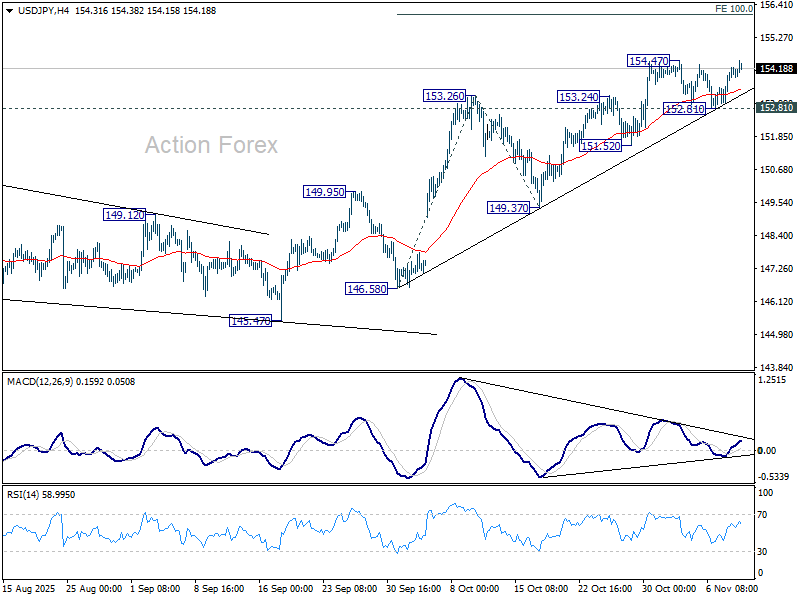

USD/JPY Daily Outlook

Daily Pivots: (S1) 153.64; (P) 153.95; (R1) 154.43; More…

Immediate focus is now on 154.47 resistance in USD/JPY. Decisive break there will confirm resumption of whole up trend from 139.87. Next target is 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Break there will pave the way to 158.85 key structural resistance. However, break of 152.81 support will turn bias back to the downside for 149.37 support for deeper correction.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 149.37 support will dampen this bullish view and extend the corrective pattern with another falling leg.