Yen Falls as Takaichi Urges BoJ to Hold Fire; U.S. Fiscal Vote in Focus – Action Forex

Yen extended its broad decline in Asian session as Japanese Prime Minister Sanae Takaichi doubled down on her call for the BoJ to delay further rate hikes. Addressing parliament, Takaichi said consumer prices—up around 3%—are being lifted mainly by food costs, particularly rice, rather than by wage growth or strong demand. She described the current trend as “not good” for households or the broader economy.

Takaichi said such price increases “hurt people’s livelihood and could weigh on the economy,” warning that Japan still faces the risk of returning to deflation if households pull back on spending. Deflation, she cautioned, would damage corporate profits and undermine wage-setting behavior, reversing the progress made since the BoJ’s ultra-loose policy began to unwind. “This is a matter that affects monetary policy in a big way,” she added, pledging close coordination with the BoJ—a signal many traders took as further confirmation that rate hikes are politically discouraged for now.

The remarks extend a theme of political caution surrounding the BoJ’s normalization efforts. While several policymakers, including dissenting board members, have pushed for tightening to resume soon, the message from Tokyo suggests that Governor Kazuo Ueda will face significant pressure to hold off at the next meeting. The dovish overhang has driven fresh weakness in the Yen, which continues to underperform against all major peers this week.

Elsewhere, attention is turning to Washington, where the Republican-controlled House of Representatives is set to vote later today on a compromise bill to restore government funding and end the historic 42-day shutdown. The Senate approved the deal on Monday, and House Speaker Mike Johnson expressed confidence that it will clear his chamber. The bill would reopen shuttered federal departments and extend funding through January 30.

Equity sentiment, however, turned mixed. Technology stocks lagged after SoftBank confirmed plans to sell its stake in Nvidia to fund its own AI investments, dragging semiconductor shares lower and trimming early gains on Wall Street futures. The move came amid broader caution as investors awaited the House vote.

In the currency markets, Yen remains the weakest performer so far this week, followed by Sterling and Dollar. At the top end, Swiss Franc leads the pack, buoyed by optimism over a potential U.S.–Swiss tariff deal. Aussie and Kiwi also gained ground on improving risk appetite, while Loonie and Euro are trading in mid-range positions.

In Asia, at the time of writing, Nikkei is up 0.24%. Hong Kong HSI is up 0.60%. China Shanghai SSE is down -0.23%. Singapore Strait Times is up 0.34%. Japan 10-year JGB yield is down -0.006 at 1.690. Overnight, DOW rose 1.18%. S&P 500 rose 0.21%. NASDAQ fell -0.25%. 10-year yield rose 0.010 to 4.120.

RBA’s Jones warns on geopolitical risk underpricing, notes Gold shift

RBA Assistant Governor Brad Jones cautioned that global markets may be underestimating geopolitical risks and systemic fragmentation. At a conference today, he highlighted that risk premiums across major asset classes have fallen to “concerning lows,” suggesting investors are failing to fully price in potential shocks.

“We’re just surprised that there’s not a bit more reflected in spreads given what we observe,” Jones said, pointing to what he called “a confronting set of potential risks.”

Jones also drew attention to shifting dynamics in global reserve management, noting “emerging evidence of fragmentation” in how central banks allocate their assets. He said a distinct group of countries has driven the recent surge in official Gold holdings, reflecting a growing desire to diversify away from dollar- and euro-denominated assets amid heightened concerns about “risk of asset seizure sanctions”.

FTSE pushes toward 10k, GBP/CHF vulnerable, next hinges on UK GDP

Markets are increasingly convinced the BoE will deliver a rate cut next month, after weak labour data showed the UK economy is losing traction. The shift in sentiment has sent the FTSE 100 powering to fresh record highs, with 10,000 level now within reach. Sterling has come under broad pressure, particularly against its European peers. The labor market’s deterioration—rising unemployment, slower pay growth, and growing slack—suggests more weakness than the MPC’s November forecast assumed.

Attention now turns to Thursday’s Q3 GDP report, expected to show a modest 0.2% qoq expansion and stagnation in September. Such subdued momentum could persist into next year, reinforcing calls for the BoE to resume its gradual easing cycle. The Bank is seen returning to a quarterly cut rhythm, delayed only by uncertainty surrounding last week’s Autumn Budget. A weaker-than-expected GDP print would likely fuel talk of a deeper, more sustained rate-cut trajectory into 2026.

In markets, FTSE’s decisive break above its recent channel signals strong bullish acceleration. Near term outlook will stay bullish as long as 9638.98 support holds. Further rise should be seen through 10k psychological level at 100% projection of 8707.65 to 9577.08 from 9276.91 at 10146.34.

GBP/CHF is still bounded in range above 1.0499 support despite yesterday’s dip. Yet, outlook remains bearish with 1.0658 support turned resistance intact. Firm break of 1.0499 will resume the larger down trend to 100% projection of 1.1204 to 1.0658 from 1.0959 at 1.0413.

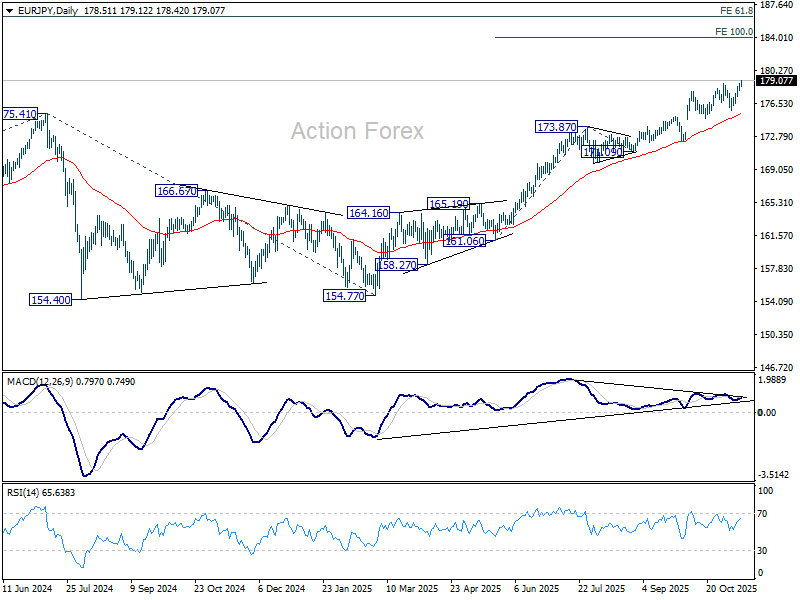

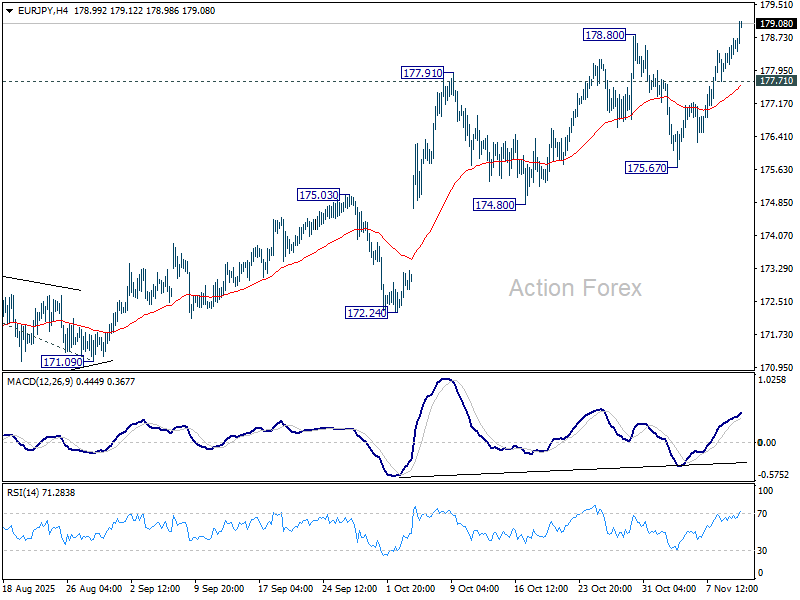

EUR/JPY Daily Outlook

Daily Pivots: (S1) 178.11; (P) 178.43; (R1) 178.87; More…

EUR/JPY’s up trend resumed by breaking through 178.80 resistance and intraday bias is now on the upside. Next target is 100% projection of 161.06 to 173.87 from 171.09 at 183.90. On the downside, below 177.71 minor support will turn intraday bias neutral and bring consolidations. But outlook will stay bullish as long as 175.67 support holds, in case of retreat.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Outlook will continue to stay bullish as long as 55 W EMA (now at 168.56) holds, even in case of deep pullback.