Indecisive Session as Sterling and Aussie Moves Fizzle – Action Forex

The forex markets were broadly indecisive today, with major currencies struggling to find convictions in their movements. Sterling initially fell after weaker-than-expected Q3 GDP print but the decline proved short-lived. The markets appeared to have already priced in a December BoE cut following earlier labor data. Instead, the focus has shifted toward the pace of rate cuts in 2026, which is heavily dependent on the tone of the Autumn Budget later this month.

Aussie jumped on the back of today’s strong employment report, but momentum faded as markets quickly recognized that the data merely affirm the widely expected RBA hold through year-end. Anything beyond December is still premature to judge. The path for 2026 hinges critically on the Q4 CPI release in late January. In the meantime, more labor market data will arrive, and these could shift expectations at the margin, especially if wage momentum surprises in either direction.

Dollar softened modestly as traders were probably positioning ahead of renewed data flow following the end of the prolonged government shutdown. Nevertheless, with Fed fund futures pricing just over 50% chance of a December 25bps cut, markets are clearly split on whether the Fed will move before year-end or with a delay.

On the trade front, attention turned to comments from EU Trade Commissioner Maros Sefcovic, who proposed accelerating the removal of the de minimis threshold on low-value imports into the bloc. The move—aimed at Chinese e-commerce giants like Shein and Tema—would bring forward new customs duties to Q1 2026, two years earlier than planned, signaling a tougher stance on protecting European competitiveness.

Overall, Swiss Franc continues to outperform on the week. Aussie and Kiwi follow as next-best performers, while the Yen remains pinned at the bottom. Dollar and Sterling are also soft, with Euro and Loonie holding mid-pack.

In Europe, at the time of writing, FTSE is down -0.80%. DAX is down -0.59%. CAC is up 0.34%. UK 10-year yield is up 0.025 at 4.428. Germany 10-year yield is up 0.029 at 2.675. Earlier in Asia, Nikkei rose 0.43%. Hong Kong HSI rose 0.56%. China Shanghai SSE rose 0.73%. Singapore Strait Times rose 0.15%. Japan 10-year JGB yield closed flat at 1.692.

Eurozone industrial production disappoints with 0.2% mom growth, consumer goods weigh

Eurozone industrial production rose only 0.2% mom in September, sharply below expectations of 0.8%. The modest gain reflected mixed sectoral dynamics — output increased for intermediate goods (+0.3%), capital goods (+0.3%), and energy (+1.2%), but fell for durable consumer goods (-0.5%) and non-durable consumer goods (-2.6%).

Across the broader European Union, output performed better, rising 0.8% mom, helped by strong growth in Denmark (+7.2%), Sweden (+5.3%), and Greece (+4.8%). However, steep contractions in Ireland (-9.4%), Luxembourg (-5.7%), and Malta (-1.7%) underscored the fragmented nature .

UK GDP grows 0.1% qoq in Q3, vehicle production plunges

The UK economy barely grew in Q3, with GDP expanding just 0.1% qoq, below expectations for 0.2%, reinforcing concerns about stagnation as demand cools. The latest figures show services output rising 0.2% qoq and construction up 0.1%, while the production sector contracted -0.5%, offsetting modest gains elsewhere. Real GDP per head was flat, underscoring the absence of meaningful growth in living standards.

Monthly data painted an even weaker picture. September GDP fell -0.1% mom, missing forecasts for a flat reading, following zero growth in August (revised from +0.1%) and a -0.1% contraction in July. The decline was driven by a -2.0% drop mom in production, as a steep -28.6% collapse in vehicle manufacturing subtracted 0.17 percentage points from overall GDP. In contrast, services and construction both managed modest 0.2% expansions.

Australia jobs surge 42.2k in October as unemployment rate falls to 4.3%

Australia’s labor market showed renewed strength in October, with employment rising by 42.2k, more than double market expectations of 20.3k. The gain was driven by a 55.3k surge in full-time positions, partly offset by a -13.1k drop in part-time work, highlighting a solid expansion in higher-quality jobs.

The unemployment rate unexpectedly fell from 4.5% to 4.3%, beating forecasts of 4.4%, while the participation rate held steady at 67.0%. Meanwhile, monthly hours worked climbed 0.5% mom, further underscoring the underlying resilience of labor demand.

The upbeat figures reaffirm Australia’s labor market resilience and encourage the RBA to maintain its current cautious tone rather than pivot quickly toward easing. With inflation pressures lingering and employment holding firm, the RBA is likely to wait for clearer signs of slack before signaling rate cuts—keeping February as the earliest plausible window for policy adjustment.

BoJ’s Ueda highlights tight job market, resilient consumption

BoJ Governor Kazuo Ueda told parliament today that Japan’s inflation is gradually aligning with the central bank’s 2% goal, supported by improving wages and steady domestic demand. He reiterated the BoJ aims for moderate inflation accompanied by rising incomes and economic improvement, rather than price gains driven solely by import costs or temporary shocks.

Ueda noted that while demand for food and other non-durable goods has softened, household consumption remains resilient thanks to higher incomes and a tight labor market. He highlighted that stronger wage growth is helping sustain a moderate cycle of rising prices and pay—an essential precondition for durable inflation in the BoJ’s framework.

He added that underlying inflation—stripping out volatile components—is gradually accelerating toward the 2% target, driven not only by food but also by price increases across a broader range of goods and services.

“When we look at underlying inflation that strips away temporary factors, it is gradually accelerating toward our 2% target,” he said.

Japan CGPI rises 2.7% yoy in October, weak yen fails to lift import prices

Japan’s Corporate Goods Price Index rose 2.7% yoy in October, easing slightly from 2.8% in September but exceeding expectations of 2.5%, according to Bank of Japan data.

Notably, the Yen-based import price index fell -1.5% from a year earlier, marking its ninth straight month of decline. The persistent drop indicates that the weak Yen is not translating into renewed cost-push inflation—contradicting the typical currency-inflation link.

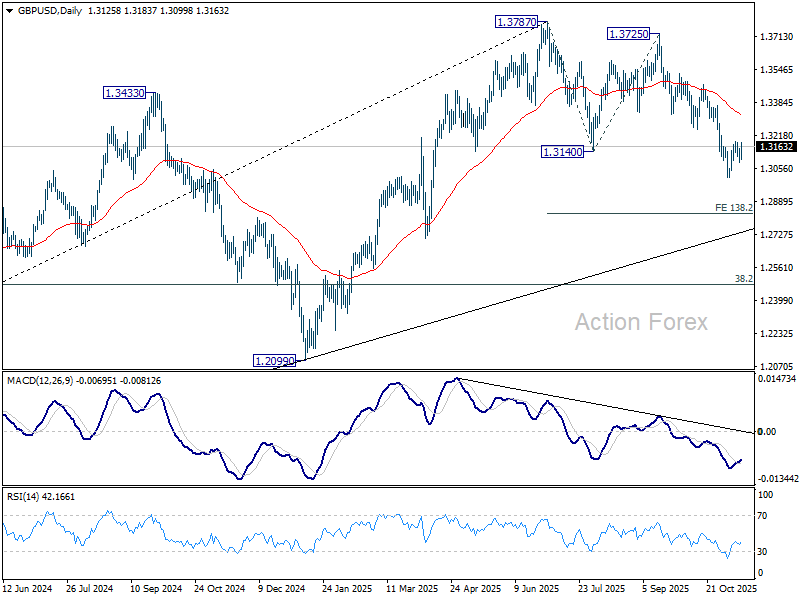

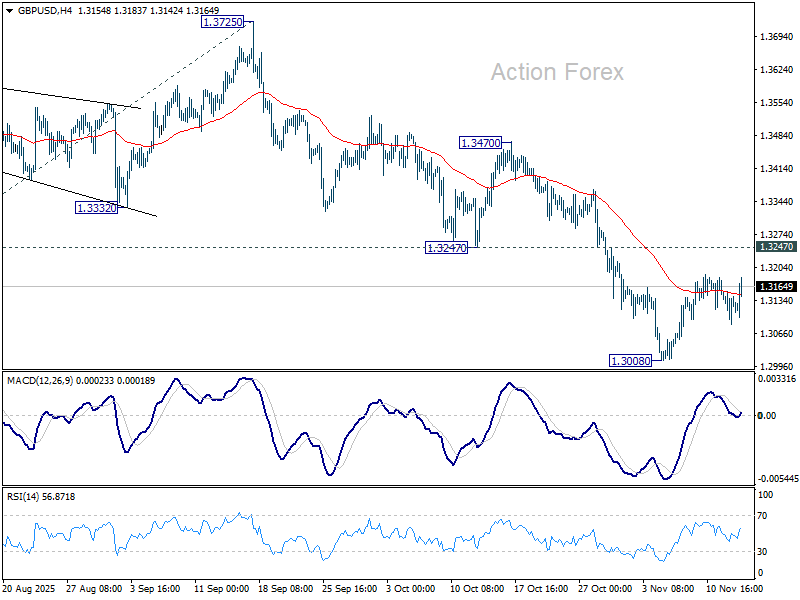

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3089; (P) 1.3128; (R1) 1.3171; More…

GBP/USD dipped briefly today but quickly recovered. Intraday bias remains neutral as range trading continues. Further decline is expected as long as 1.3247 support turned resistance holds. Break of 1.3008 will target 138.2% projection of 1.3787 to 1.3140 from 1.3725 at 1.2831. Nevertheless, firm break of 1.3247 will suggest that fall from 1.3787 has completed as a corrective move already.

In the bigger picture, the break of 55 W EMA (now at 1.3185) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2780) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.