Dollar Eases as Markets Shift to Risk-On Despite Strong NFP – Action Forex

Dollar strength faded mildly after the stronger-than-expected U.S. non-farm payroll report, as traders showed little appetite to extend the post-data rally. The muted reaction reflects a market that had already repriced aggressively after yesterday’s hawkish FOMC minutes, which pushed expectations for a December rate cut sharply lower. In that sense, much of the adjustment had already been done before today’s data even hit.

The jobs report merely reinforces the prevailing view: the Fed may not need to cut again in December, and policymakers can comfortably adopt a wait-and-see approach. Rather than reset expectations, the numbers simply validated what markets had already shifted toward following the minutes. With the pricing for a December cut already pared back, there was limited room for the Dollar to gain further on the headline beat alone.

At the same time, risk sentiment has flipped decisively into positive territory, driven by renewed AI enthusiasm after Nvidia’s earnings report. The resurgence in tech optimism has spilled across global equities and FX markets, providing fresh support to risk-sensitive currencies, even Sterling, and curbing defensive flows into Dollar.

Still, one feature of the FX markets that hasn’t changed this week is the extended and persistent weakness in Yen. Expectations that BoJ will delay its next rate hike — combined with rising global yields and Japan’s pro-stimulus policy backdrop — continue to leave the currency pinned at the bottom of the performance table.

For the week so far, Dollar remains the strongest performer, followed by Loonie and then Aussie. Yen sits firmly at the bottom, trailed by Swiss Franc and Kiwi. Euro and Sterling are positioned in the middle, with the Pound maintaining a slight edge thanks to improved risk appetite.

In Europe, at the time of writing, FTSE is up 0.62%. DAX is up 1.11%. CAC is up 0.90%. UK 10-year yield is down -0.015 at 4.584. Germany 10-year yield is up 0.014 at 2.731. Earlier in Asia, Nikkei rose 2.65%. Hong Kong HSI rose 0.02%. China Shanghai SSE fell -0.40%. Singapore Strait Times rose 0.15%. Japan 10-year JGB yield jumped 0.049 to 1.820.

US NFP beats expectation with 119k growth, but unemployment rate ticks up to 4.4%

U.S. non-farm payrolls surprised strongly to the upside in September, rising 119k versus expectations of 53k, more than making up for August’s downward revision from 22k to -4k. The stronger headline signals that hiring momentum hasn’t stalled as much as feared.

However, the details of the report were more mixed. The unemployment rate edged up from 4.3% to 4.4%, slightly above expectations. Though the increase came alongside a modest rise in participation from 62.3% to 62.4%, suggesting more workers entered the labor force.

Wage growth cooled, with average hourly earnings up only 0.2% mom, below the 0.3% consensus, bringing annual growth to 3.8% yoy. The average workweek held steady at 34.2 hours, pointing to no deterioration in hours worked.

Taken together, the data portray an economy that is still generating jobs but with softer wage pressures—likely welcomed by the Fed as it evaluates the necessity of another rate cut before year-end.

BoJ hawkish voice emerges as Koeda presses for further tightening

BoJ board member Junko Koeda delivered one of the clearest hawkish signals from the Bank in recent months, arguing that real interest rates remain “significantly low” and must be moved back toward “a state of equilibrium” to avoid “unintended distortions” later.

With Japan’s output gap hovering around zero and labor market tightness intensifying amid widespread staff shortages, she said in a speech that current economic backdrop justifies continued normalization. In her view, the BoJ should “continue to raise” the policy rate as economic conditions improve, adjusting monetary support in line with the broader recovery in activity and prices.

Koeda stressed that underlying inflation is running near 2%, but achieving the target sustainably requires the Bank to test how firmly “underlying inflation has remained stable or been anchored”. That means looking beyond headline data to evaluate whether price momentum can hold as temporary factors fade.

Her message contrasted with recent political pressure urging caution on tightening, reinforcing the divide between policymakers seeking gradual normalization and government voices favoring prolonged accommodation.

PBoC stays on hold, but markets still see easing ahead

China kept its benchmark lending rates unchanged for the sixth straight month today, leaving the one-year Loan Prime Rate at 3.0% and the five-year rate at 3.5%. The decision was widely expected, as policymakers continue to balance the need to support the economy with the desire to avoid fuelling financial instability.

Despite the steady stance, markets remain convinced that monetary easing has merely been delayed, not abandoned. Expectations are building for a “dual cut” — both policy rates and banks’ reserve requirement ratio — in the first quarter of 2026.

A run of softer October activity data has strengthened that view. Exports contracted, retail sales slowed further, and the property-related drag has shown little sign of easing. Combined, these have heightened concerns that Q4 will bring more headwinds rather than signs of stabilization.

Adding to the pressure, new bank lending fell sharply in October as both households and businesses remained reluctant to take on fresh debt amid weak confidence and ongoing US-China trade tensions. Without a meaningful pickup in credit demand, Beijing may soon have little choice but to act more decisively to shore up activity in early 2026.

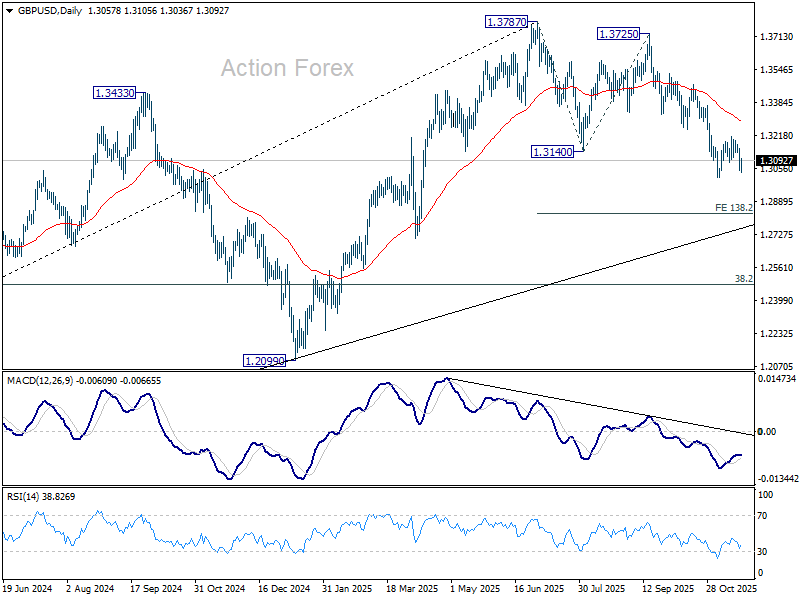

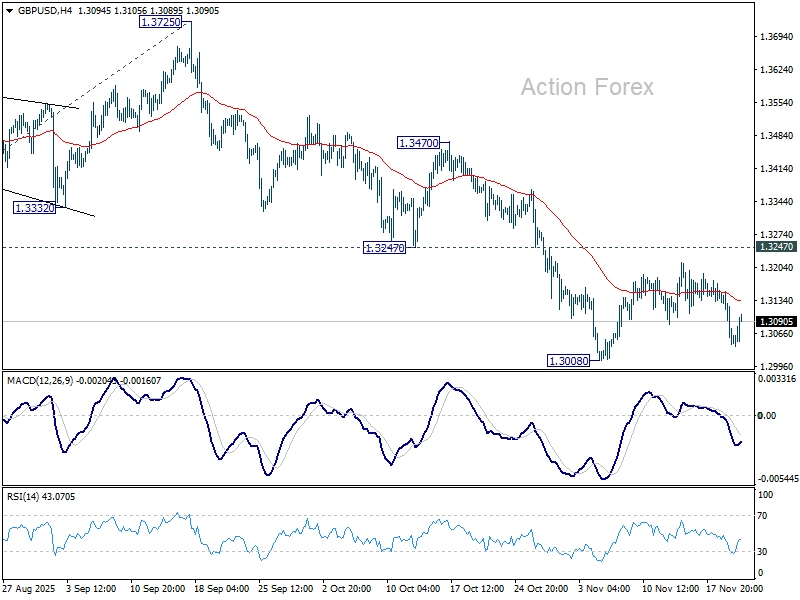

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3018; (P) 1.3087; (R1) 1.3129; More…

GBP/USD recovers mildly today as range trading continues. Intraday bias remains neutral and outlook is unchanged. Further decline is expected as long as 1.3247 support turned resistance holds. Break of 1.3008 will resume the fall from 1.3787, and target 138.2% projection of 1.3787 to 1.3140 from 1.3725 at 1.2831. Nevertheless, firm break of 1.3247 will suggest that fall from 1.3787 has completed as a corrective move already.

In the bigger picture, the break of 55 W EMA (now at 1.3182) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2824) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.