Kiwi, Aussie Dominate; Sterling Awaits for High-Stakes Budget – Action Forex

Risk-on sentiment extended through Asian session, from intensifying bets on December Fed rate cut. The shift in sentiment sent US stocks higher overnight, and pushed 10-year yield briefly below 4% handle. Kiwi and Aussie are the biggest beneficiary of this backdrop, with both additionally supported by domestic developments.

Kiwi is the standout performer as markets digested RBNZ’s hawkishly framed rate cut. By signaling that the OCR is likely already at its trough and projecting only a modest lift through 2027, the central bank effectively pushed back against earlier expectations of a deeper easing cycle. Aussie also attracted buyers after Australia’s inflation data showed sharper acceleration than expected. Any RBA rate cut is pushed further into 2026.

Yen, however, remained soft despite renewed chatter around a December BoJ hike. Reuters reported that the central bank is preparing markets for a possible move as early as next month, following a key meeting between Prime Minister Sanae Takaichi and Governor Kazuo Ueda that appeared to remove political hurdles. Even so, sources suggested a close call between a December hike and a delay to January, with the Fed decision a week earlier likely to influence the decision. But for now, Yen traders appear e unconvinced.

Attention turns next to the UK Autumn Budget, which carries unusually high uncertainty after contradictory messaging from Chancellor Rachel Reeves on tax measures. Markets have little guidance on the scope or direction of fiscal changes, leaving room for large surprises. Gilt reaction will be the clearest test of investor confidence in the government’s fiscal stance. Sterling will trade off Gilt yields, but inversely—this is a confidence story, not a yield-seeking one.

For the week so far, Kiwi leads the performance board, followed by Aussie and Sterling. Dollar sits at the bottom, with Loonie and Yen also heavy, while Euro and Swiss Franc hover around the middle of the pack.

In Asia, at the time of writing, Nikkei is up 1.98%. Hong Kong HSI is up 0.44%. China Shanghai SSE is up 0.14%. Singapore Strait Times is up 0.56%. Japan 10-year JGB yield is up 0.015 at 1.819. Overnight, DOW rose 1.43%. S&P 500 rose 0.91%. NASDAQ rose 0.67%. 10-year yield fell -0.036 to 4.002.

RBNZ delivers 25bps cut but signals little room for further easing

RBNZ cut the OCR by 25bps to 2.25% as widely expected, but the tone of the announcement was more hawkish than markets had anticipated.

Policymakers revealed they had debated holding rates at 2.50% versus cutting to 2.25%, and the final decision was reached by a 5–1 vote. The lone dissenter in favour of holding highlights pockets of concern about easing too deeply and reflects a more cautious internal balance than many had assumed.

More importantly for markets, RBNZ’s updated forward guidance showed a notably firmer policy path. The Bank now expects the OCR to bottom at just 2.2% through 2026 before gradually rising to 2.7% by the end of 2027. That trajectory implies minimal scope for further cuts next year if the economic outlook holds, effectively signaling that today’s move may mark the end of the easing cycle.

The accompanying statement reinforced that message. RBNZ said economic activity was weak through mid-2025 but is now improving, with lower interest rates supporting household spending and the labor market stabilizing. The fall in the exchange rate is also lifting exporters’ incomes, reducing the need for more aggressive stimulus from here. Risks to the inflation outlook are now viewed as “balanced”.

Australia CPI surges to 3.8% in October, goods and services prices accelerate

Australia’s CPI accelerated more than expected in October, rising from 3.5% yoy to 3.8%, beating expectations of 3.6%. Underlying pressure also firmed, with trimmed mean CPI moving up from 3.2% to 3.3%.

Both goods and services inflation picked up, with annual goods inflation at 3.8% (up from 3.7%) and services inflation at 3.9% (up from 3.5), signaling renewed price momentum. The combination will keep the RBA wary of easing again too soon.

The details showed broad-based increases. Housing costs was the largest contributor at 5.9%, followed by food and non-alcoholic beverages at 3.2%, and recreation and culture at 3.2%.

The release is also notable as the first in which Monthly CPI replaces the quarterly gauge as Australia’s primary headline measure.

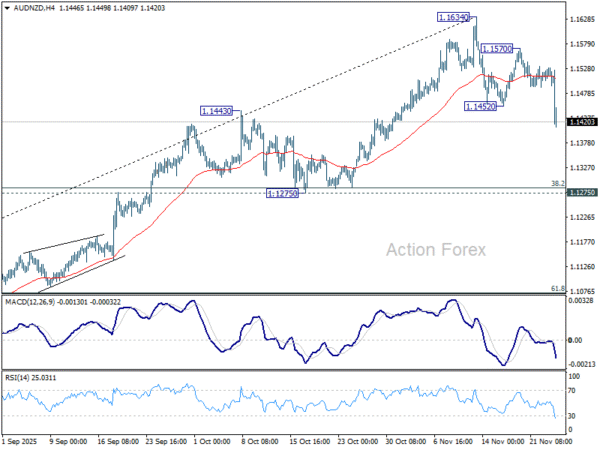

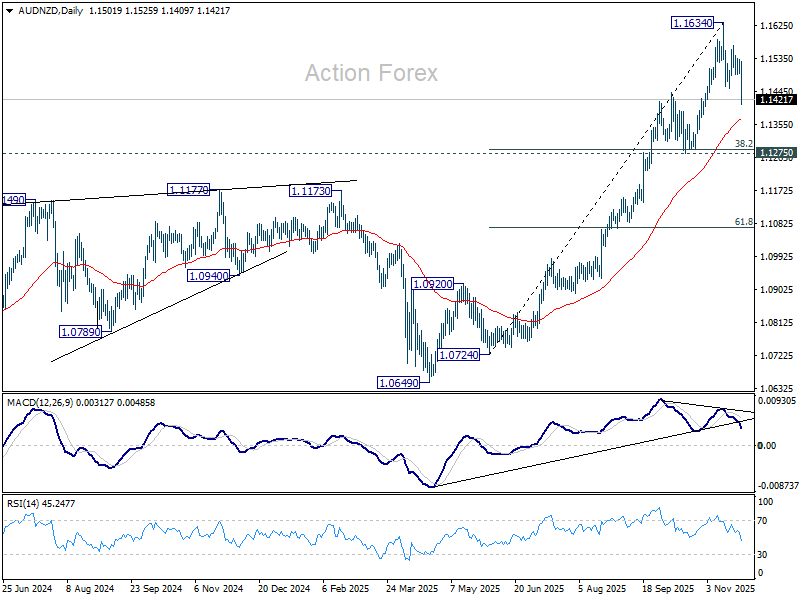

AUD/NZD drops as hawkish RBNZ cut overpowers hot Australia CPI

AUD/NZD tumbled sharply today as markets digested two major releases: RBNZ’s widely expected 25bps cut and Australia’s stronger-than-forecast CPI print. Despite the upside surprise on inflation, AUD buying was no match for the hawkish tone embedded in RBNZ’s announcement, which effectively signaled that the easing cycle is now complete.

That distinction proved decisive. With RBNZ projecting the OCR to bottom near current levels and rise gradually into 2027, the case for deeper easing has evaporated. Although the RBA is also expected to stay on hold through early 2026, the interest-rate differential is now set to remain stable rather than widening. Investors who previously bet on wider divergence, a trend accelerated by New Zealand’s sharp Q2 economic contraction, are now unwinding positions.

Technically, AUD/NZD’s break of 1.1452 support confirms resumption of the decline from 1.1634 short term top. Considering bearish divergence condition in D MACD, fall from 1.1634 is likely correcting rise from 1.0724. Deeper fall should be seen to 55 D EMA (now at 1.1367) and possibly below.

But strong support is expected from 1.1275 cluster (38.2% retracement of 1.0724 to 1.1634 at 1.1286) to bring rebound and set the range for sideway trading.

Rise from 1.0649 is still expected to have another rising leg through 1.1634 to complete a five-wave impulsive pattern. But that’s unlikely to happen soon. The move may only come when the markets start to bet that RBA would hike interest rate earlier than RBNZ, which won’t be in the near future.

That next leg, however, would require a significant shift in rate expectations—specifically, a scenario where markets begin to see the RBA tightening earlier than RBNZ, which is not on the horizon at present.

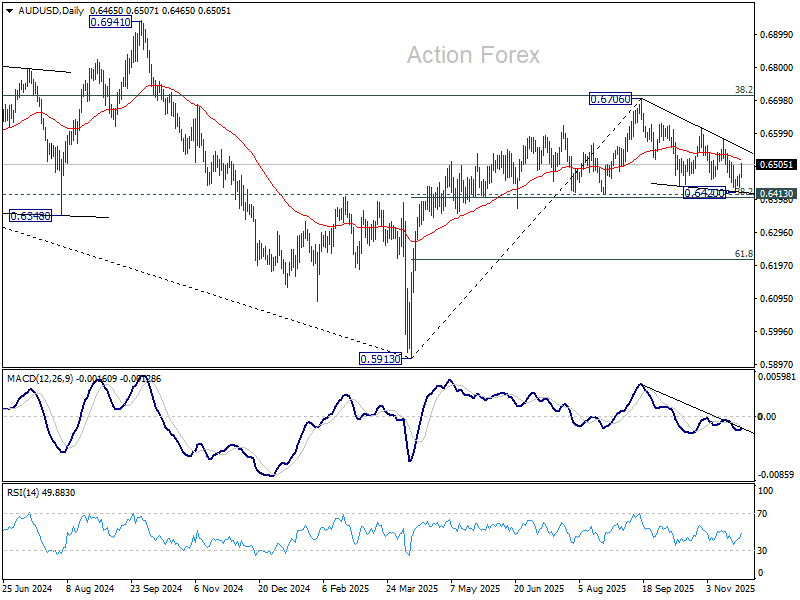

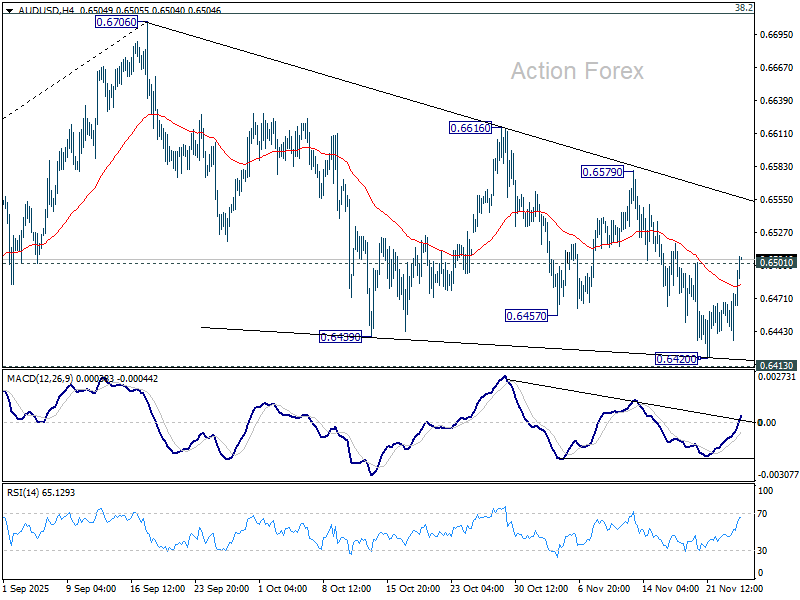

AUD/USD Daily Report

Daily Pivots: (S1) 0.6445; (P) 0.6461; (R1) 0.6485; More...

AUD/USD’s extended rebound and break of 0.6501 resistance suggests short term bottoming at 0.6420. Intraday bias is back on the upside for 06579 resistance. Firm break there should confirm that whole fall from 0.6706 has completed as a three wave correction. Stronger rally should then be seen back to retest 0.6706. On the downside, sustained break of 0.6413 cluster (38.2% retracement of 0.5913 to 0.6706 at 0.6403) should confirm near term bearish reversal.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Break of 0.6413 support will suggest rejection by 0.6713 and solidify this bearish case. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.