Dollar Stays Soft Into Thanksgiving Lull – Action Forex

Trading turned subdued as markets moved into the U.S. session, with activity expected to slow further as Thanksgiving approaches. Liquidity conditions were already thinning in early trade, and the muted tone across majors reflects a market unwilling to take fresh positions before the long weekend. Despite the quieter backdrop, broader directional themes remain unchanged.

Dollar attempted a modest recovery earlier in the day but lacked momentum, with the prospect of a December Fed rate cut still acting as a cap on any sustained rally. Much of the intraday movement appears to be position-squaring rather than a shift in sentiment, with traders closing shorts and reducing exposure ahead of the holiday. The underlying bias remains tilted against the greenback.

Yen also tried to firm but struggled to gain traction. Falling U.S. yields provides some support, yet these gains are partially offset by expectations that BoJ could hold in December. By contrast, Kiwi and Aussie remain among the stronger performers, supported by both constructive risk sentiment and supportive domestic developments.

For the week so far, Kiwi remains the best performer, with Sterling now overtaking Aussie for second place. Dollar is anchored at the bottom of the pack, followed by Yen and Swiss Franc. Euro and Loonie sit in the middle.

In Europe, at the time of writing, FTSE is down -0.10%. DAX is up 0.26%. CAC is up 0.11%. UK 10-year yield is up 0.036 at 4.464. Germany 10-year yield is up 0.009 at 2.683. Earlier in Asia, Nikkei rose 1.23%. Hong Kong HSI rose 0.07%. China Shanghai SSE rose 0.29%. Singapore Strait Times rose 0.17%. Japan 10-year JGB yield fell -0.017 to 1.802.

ECB accounts show unified hold, but debates on future cut threshold

ECB meeting accounts from October showed unanimous agreement to keep all three key interest rates unchanged, with policymakers noting that both the inflation outlook and incoming activity data had broadly aligned with September’s baseline. The economy was still expanding despite global headwinds, giving the Governing Council confidence that the current stance remained appropriate.

Members highlighted that December will bring critical new information, including a fresh set of staff projections extending to 2028 for the first time. These forecasts will offer a “clearer picture of the outlook at that horizon”.

However, the accounts revealed differing views on whether the rate-cutting cycle has fully run its course. Some members argued that the favorable outlook meant that “should not be fine-tuned” in response to “moderate and temporary fluctuations” of inflation.

Others cautioned that the Governing Council must remain “entirely open-minded,” noting that another rate cut could be justified if downside risks intensified or if projected inflation undershoots persisted. That viewpoint stressed that the bar for action should be “no higher than normal”.

Eurozone economic sentiment marks mild gains, but stay below long-term average

EU and Eurozone posted only marginal improvements in sentiment in November, with the Economic Sentiment Indicator rising 0.2 points in both regions to 96.8 and 97.0. While the Employment Expectations Indicator saw a more meaningful lift—up to 98.8 in the EU and 97.8 in the Eurozone. Both gauges remain below their historical averages of 100.

Sector trends again showed uneven dynamics. Services, retail and construction recorded higher confidence. But industry confidence weakened further, nearly cancelling out those gains and keeping the overall ESI flat. Consumer sentiment was little changed,.

Across major EU economies, sentiment gains were led by Spain (2.0), Italy (1.1), France (0.) and Poland (0.5), while Germany and the Netherlands were steady at -0.3.

Noguchi says BoJ can restart hikes gradually as Yen weakness turns problematic

BoJ board member Asahi Noguchi said today that the central bank could resume interest rate hikes once U.S. tariff risks recede, but emphasized that any tightening must “measured, step-by-step”.

He warned that maintaining very low real interest rates for too long risks undermining the economy by pushing Yen lower and stoking undesirable inflation. A weaker currency, he said, lifts prices through import costs and boosts exports in a way that can overheat the economy .

Noguchi highlighted that Yen depreciation was once a tailwind during Japan’s deflation era, supporting exporters and helping revive demand. However, “as supply constraints intensify, the positive effects eventually disappear and are replaced by negative effects that merely push inflation higher than needed,” he added.

NZ ANZ business confidence jumps to 11 year high, green shoots well established

New Zealand’s ANZ Business Confidence index jumped from 58.1 to 67.1 in November, the strongest reading in 11 years. The survey’s own-activity outlook also surged from 44.6 to 53.1, marking the highest level since 2014 and signaling a material improvement in real economic momentum rather than sentiment alone. ANZ noted that “green shoots are looking well established”, with recent gains increasingly rooted in actual activity.

Inflation signals were more mixed. The share of firms planning to raise prices over the next three months climbed from 44% to 51%, the highest since March. However, expected cost increases eased slightly from 76% to 74%, and one-year-ahead inflation expectations were steady at 2.7%. The combination points to stabilizing inflation pressures, but not yet disinflation strong enough to encourage fresh easing from the RBNZ.

ANZ said the underlying improvement in conditions offers reassurance that the pickup is likely to be sustained. With the recovery underway and CPI sitting at the top of the target band, the bank sees little reason for further OCR cuts “barring unexpected developments.”

NZ retail sales surge 1.9% qoq in Q3, strongest since 2021

New Zealand retail sales delivered a strong upside surprise in Q3, rising 1.9% qoq versus expectations of 0.6%. Ex-auto sales also beat forecasts, up 1.2% qoq compared with 0.8% consensus.

Statistics New Zealand said this was the largest quarterly increase in retail activity since late 2021, with broad-based gains across the sector. Most industries recorded growth during the September.

The details showed particularly strong demand in motor vehicles and electrical and electronic goods retailing, which posted the biggest increases. Eight of the 15 retail industries reported higher volumes compared with Q2.

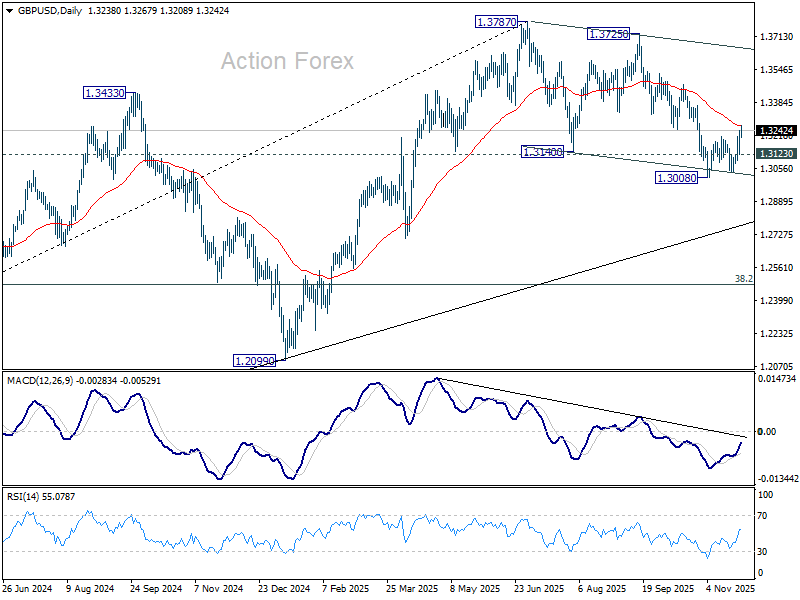

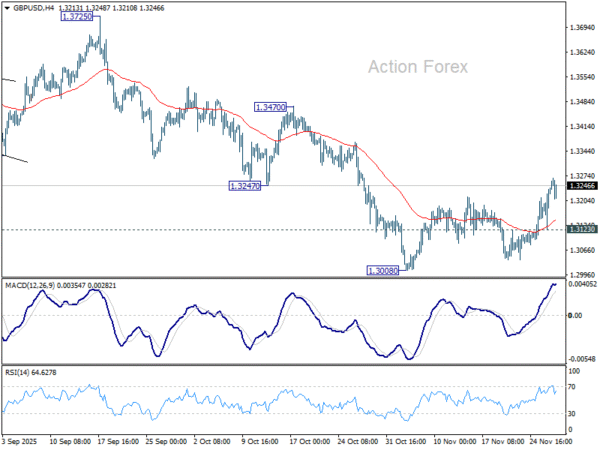

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3162; (P) 1.3204; (R1) 1.3282; More…

Intraday bias in GBP/USD stays mildly on the upside at this point. Corrective fall from 1.3787 could have completed with three waves down to 1.3008. Sustained trading above 55 D EMA (now at 1.3268) should confirm and target a retest on 1.3725/3787 resistance zone. Nevertheless, break of 1.3123 minor support will revive near term bearishness, and bring retest of 1.3008.

In the bigger picture, the break of 55 W EMA (now at 1.3184) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2760) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.