Japan Data Beats But Yen Lacks Traction; Dollar Heads for Worst Week Since Mid-Year – Action Forex

Japan’s data releases were surprisingly strong today, with both industrial output and retail sales showing impressive gains. Combined, they paint a picture of an economy that is slowly regaining momentum on both production and consumption fronts. Yet the Yen remains notably weak, failing to capitalize on the firmer-than-expected numbers.

One of the key constraints remains the inflation mix. Tokyo’s CPI held firm, but the strength is still concentrated in food prices, with rice, coffee, and chocolate continuing to show outsized gains. Services inflation, however, stayed relatively tame. That provides ammunition for the government’s argument that underlying inflation momentum is still insufficient to declare inflation “well anchored”—a key condition for more decisive BoJ tightening.

There is, however, a counter-argument. The reduction in U.S. auto tariffs is already showing up in production figures, and many expect the positive spillover to widen in the months ahead. That narrative supports the BoJ’s October assessment that downside growth risks are easing. With this major external drag fading, BoJ has more room to proceed with gradual tightening without threatening the recovery. However, how soon the BoJ acts is still an open question. The base case remains a January hike, but confidence in that call is low.

Dollar, meanwhile, remains under pressure and is heading toward its worst weekly performance since mid-year. Markets continue to price roughly 85% probability of a 25bps cut in December. That expectation has kept USD recoveries short-lived and contributed to sustained downside across the major pairs. Still, rate expectations beyond December are far from settled. Markets currently assign around 50% probability that the Fed will remain on hold through Q1, viewing the December cut largely as a risk-management move.

With the recent government shutdown delaying key data releases, the 2026 outlook remains highly uncertain. That fog should begin to lift after November non-farm payrolls on December 16 and CPI on December 18, which will provide the missing clarity on labor-market and inflation trends. Until then, any bets on extended easing—or on a prolonged pause—are premature.

In weekly performance terms, Kiwi continues to lead, followed by Aussie and Sterling. Dollar sits at the bottom, ahead of Yen and Swiss Franc, while Euro and Loonie hold mid-table positions.

In Asia, at the time of writing, Nikkei is down -0.04%. Hong Kong HSI is down -0.24%. China Shanghai SSE is up 0.21%. Singapore Strait Times is up 0.46%. Japan 10-year JGB yield is up 0.022 at 1.825.

Tokyo core CPI holds at 2.8% in November, inflation pressures still firm

In Japan, Tokyo’s inflation profile showed little moderation in November, with both core CPI and core-core CPI staying at 2.8% yoy. The readings came in slightly firmer than expected, while headline CPI eased just one-tenth to 2.7%. The stability of these measures indicates that underlying inflation momentum remains intact.

Much of the price momentum came from food, where sharp gains continued. The cost of rice surged 38.5% yoy, coffee beans rose 63.4%, and chocolate jumped 32.5%, reflecting broad price pressures across essential and discretionary categories.

Meanwhile, goods inflation climbed 4.0% yoy. Services inflation eased only marginally to 1.5% from 1.6%.

Japan industrial production surges 1.4% mom in October on auto rebound, but fluctuation to continue

Japan’s industrial production rose 1.4% mom in October, sharply beating expectations of a -0.6% decline. The rebound was driven primarily by a 6.6% jump in motor vehicle output, a sector benefiting from the U.S. tariff rate on Japanese cars being reduced to 15% from 27.5% in mid-September. The improvement highlights how quickly Japanese automakers responded once tariff uncertainty eased.

However, the forward outlook remains soft. Based on its manufacturer survey, METI expects output to fall -1.2% in November and contract a further -2.0% in December. Despite October’s upside surprise, the ministry kept its overall assessment unchanged, saying industrial production “fluctuates indecisively” amid continued uncertainty at home and abroad.

Retail sales also surprised to the upside, rising 1.7% yoy versus expectations of 0.8%. The strength suggests domestic demand remains more resilient than many feared, even as the industrial sector continues to face uneven momentum.

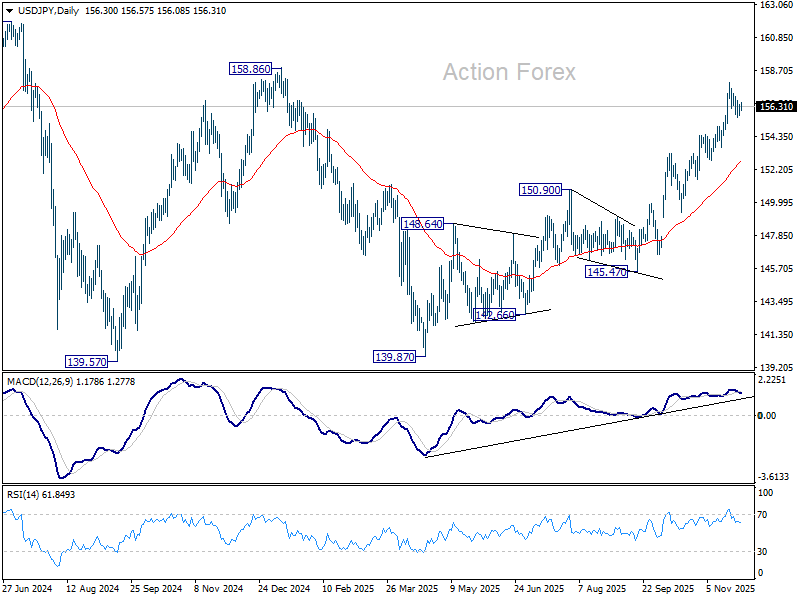

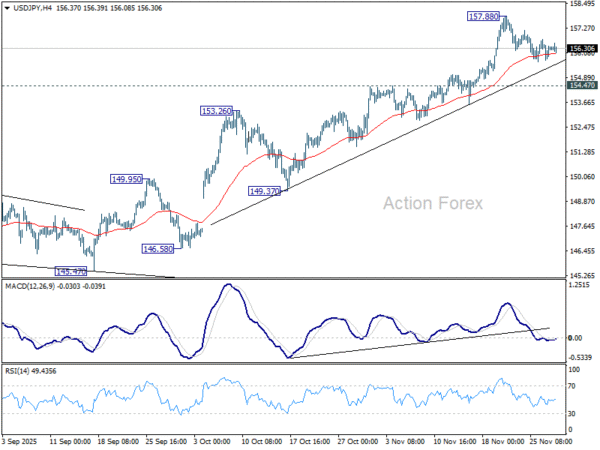

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.85; (P) 156.17; (R1) 156.63; More…

USD/JPY is still bounded in consolidations below 157.88 and intraday bias remains neutral. Downside should be contained by 154.47 resistance turned support. On the upside, break of 157.88 will resume the whole rally from 139.87. Next target is 158.86 structural resistance, and then 161.94 high. However, firm break of 154.47 will bring deeper correction to 55 D EMA (now at 152.63).

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.