Markets Stabilize After Robust JGB Auction, Retroactive US Tariff Relief for Korea – ActionForex

Market sentiment steadied across Asia today, with most assets drifting in tight ranges after Monday’s volatility. The overnight selloff in the US was modest, and fears that Japan-led risk aversion would spill aggressively into global markets did not materialize. While pockets of unease lingered—particularly in the tech space following Bitcoin’s slump—the broader tone has remained controlled.

Bitcoin extended its weak run from November and posted its worst day since March on Monday, weighing on tech-linked sentiment. Even so, the fallout has been mostly contained, with investors showing little sign of broad defensive repositioning. The stabilization in equity futures and credit markets helped underpin the more measured tone in Asian trading.

In Japan, super-long-dated yields eased after briefly touching fresh highs, providing relief after a turbulent start to the week. A successful 10-year JGB auction generated the strongest demand since September, offering reassurance to investors who had grown nervous about the pace of reflation in Japanese rates markets. The result helped reverse part of yesterday’s spike in yields.

The move comes as markets continue to digest rising expectations for a BoJ rate hike at the December meeting. Governor Kazuo Ueda’s comments earlier this week triggered a sharp repricing of rate expectations, but today’s pullback in yields and the solid auction helped calm nerves. Swaps still assign around a 70% probability to a 25bps move this month, keeping policy normalization firmly in focus.

Optimism from South Korea added to the region’s stability. Shares of major auto manufacturers rose after US Commerce Secretary Howard Lutnick confirmed that the newly negotiated 15% US auto tariff rate for South Korea would apply retroactively from November 1. The announcement boosted confidence that bilateral trade conditions are improving for Korean exporters.

In the currency markets, Yen remains the strongest performer of the week, supported by rising BoJ expectations, followed by Euro and Dollar. On the weaker side, Sterling leads the laggards, with Loonie and Swiss Franc also soft. Aussie and Kiwi sit in the middle of the pack as cross-flows dominate.

Most major pairs and crosses have drifted back inside last week’s ranges, reinforcing the view that markets have stabilized after Monday’s volatility. With no major catalysts in the Asian session, traders appear content to consolidate positions ahead of upcoming US data later in the week.

In Asia, Nikkei fell -0.05%. Hong Kong HSI is down -0.04%. China Shanghai SSE is down -0.45%. Japan 10-year JGB yield fell -0.019 to 1.860. Overnight, DOW fell -0.90%. S&P 500 fell -0.53%. NASDAQ fell -0.38%. 10-year yield rose 0.079 to 4.096. Overnight, DOW fell -0.90%. S&P 500 fell -0.53%. NASDAQ fell -0.38%. 10-year yield rose 0.079 to 4.096.

RBNZ’s Breman sets tone for Leadership: Mandate discipline and public trust

New RBNZ Governor Anna Breman used her first appearance before a parliamentary committee to underline a back-to-basics approach for the central bank. She said her leadership will be “laser focused” on the core mandate of keeping inflation low and stable, ensuring financial system resilience, and maintaining a safe and efficient payments framework.

Her comments signal an intention to anchor policy discussions firmly around credibility and discipline after a period of volatility in inflation and rate expectations. By highlighting the fundamentals of price stability and financial stability, Breman appears set to build continuity with the bank’s existing stance while strengthening its emphasis on execution and institutional reliability.

Looking into 2026, Breman said “transparency, accountability, and clear communication” will be central pillars of her leadership. She noted that maintaining public trust is critical for the next phase of policy.

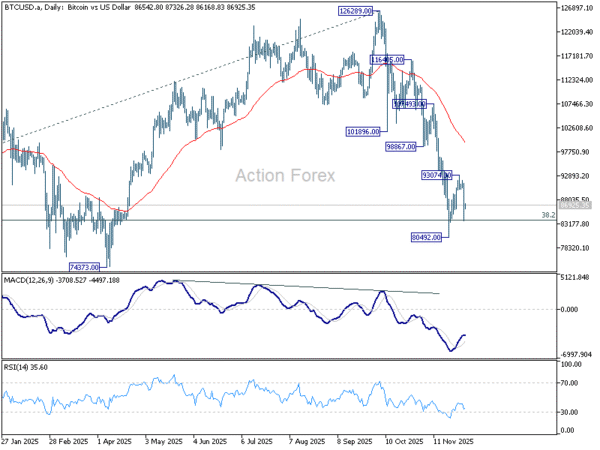

Bitcoin under pressure as rebound fades; correction targets 70k psychological level

Bitcoin’s sharp selloff this week indicates that the latest rebound has possibly already run its course, suggesting that medium-term correction is entering another downward phase. The move follows a difficult November, when Bitcoin posted its largest monthly decline since mid-2021 as a record volume of capital exited the market. Momentum remains soft, and technical structure points to further pressure ahead.

Sentiment deteriorated further on Monday after Strategy — the largest corporate holder of Bitcoin — cut its earnings outlook for 2025, citing Bitcoin’s weak performance. More broadly, Bitcoin appears to be suffering from fading enthusiasm within both the digital-asset community and the wider tech sector, where concerns about market concentration, infrastructure constraints, and slowing global cooperation are resurfacing.

Technically, the near-term rebound from 80,492 looks to have topped at 93,074. Retest of 80,492 is now the immediate focus, and firm break would resume the entire decline from 126,289. In any case, outlook will stays firmly bearish as long as 55 D EMA (now at 99,564) holds.

In the bigger picture, Bitcoin is clearly correcting the full five-wave uptrend from the 15,452 (2022 low). While further decline is expected, the 70,000 psychological region is expected to provide strong initial support for an interim base. That aligns with several structural levels: 74,373 support, 73,812 former resistance-turned-support, and 50% retracement of 15,452 to 126,289 at 70,870. This cluster reinforces the area’s importance in defining the medium-term floor.

Meanwhile sustained break back above the 55 W EMA (now at 97,447), would indicate that the medium-term correction from 126,289 has already shifted into a second leg, opening the door for a more sustained rebound. Until then, price risks remain skewed to the downside as the market digests weakening sentiment and tightening technical conditions.

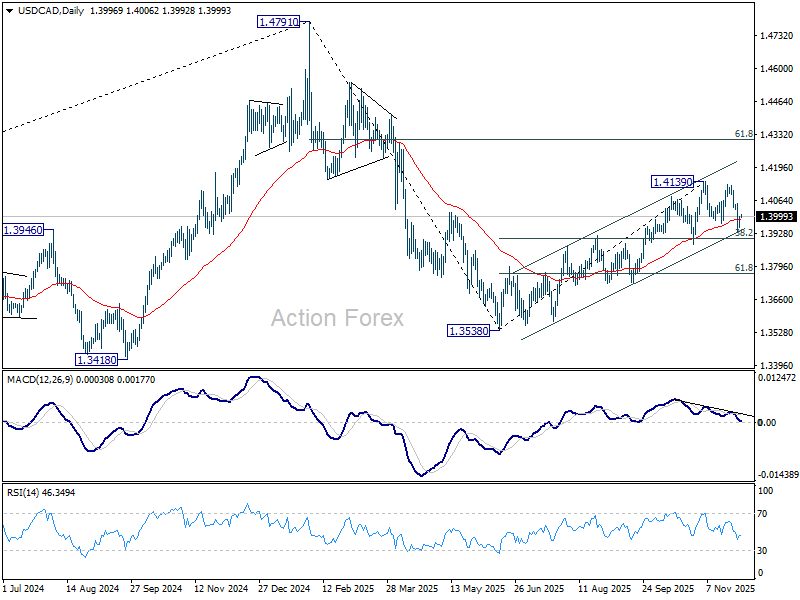

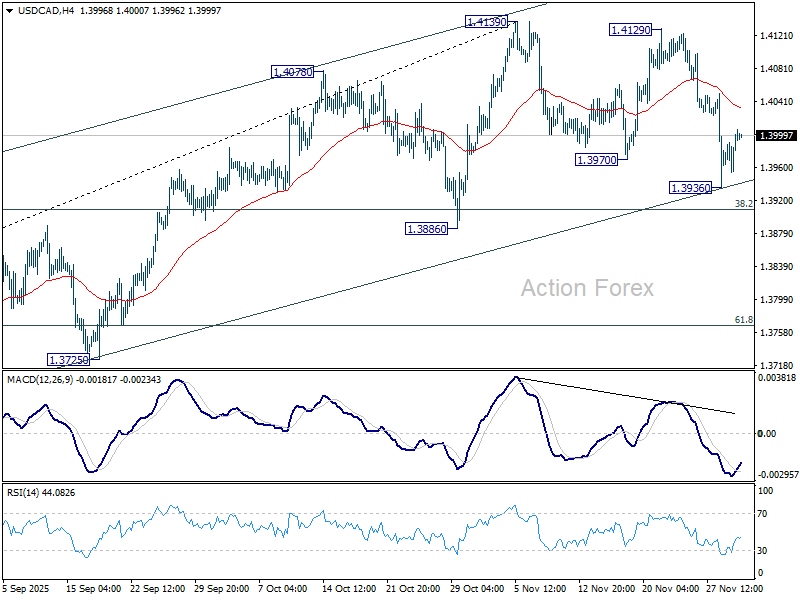

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3968; (P) 1.3985; (R1) 1.4015; More…

USD/CAD recovered ahead of near term channel support and intraday bias is turned neutral first. Some consolidations could be seen above 1.3936 temporary low. But risk will stay mildly on the downside as long as 55 4H EMA(now at 1.4033) holds. Below 1.3936 will target 38.2% retracement of 1.3538 to 1.4139 at 1.3909. Sustained break there will indicate that whole rise from 1.3538 has completed. Deeper fall should then be seen to 61.8% retracement at 1.3768 next. However, fir break of 55 4H EMA will retain near term bullishness, and bring retest of 1.4139 high.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low), with rise from 1.3538 as the second leg. A third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3886 support holds. However, firm break of 1.3886 will revive the case that fall from 1.4791 is indeed a larger scale correction.