Markets Turn Cautious Ahead of FOMC as Talk of “Hawkish Cut” Builds – ActionForex

Global markets adopted a more cautious tone today, with Asian equities drifting lower after Wall Street’s soft session. The price action reflects hesitation rather than fear, with most investors choosing not to commit ahead of tomorrow’s critical FOMC outcome.

Talk has intensified that the Fed could deliver what many are calling a “hawkish cut.” A 25bps reduction to 3.50–3.75% is essentially a done deal, but the messaging around it may matter more. After three straight cuts aimed at stabilizing the labor markets, the Committee may use this meeting to telegraph that a long pause is now appropriate.

The Fed’s own estimates put neutral at 2.8–3.5%. Given inflation’s persistence, particularly in services and wages, policymakers may need to retain a modest level of restriction. This would limit the scope for additional cuts unless the disinflation trend strengthens, or labor market deterioration intensifies.

Meanwhile, equity sentiment may see pockets of relief today. Nvidia rallied after President Donald Trump posted on Truth Social that the chipmaker could ship its H200 processors to “approved customers” in China and elsewhere, provided a quarter of the sales revenue is paid to the U.S. government. Still, any bounce is likely to be temporary given the scale of event risk tied to tomorrow’s FOMC projections and press conference.

In the currency markets, Aussie is the day’s strongest performer following the hawkish RBA hold. Governor Michele Bullock reaffirmed that there is no justification for further cuts and that the board is actively discussing the circumstances under which a hike could occur next year. Kiwi follows closely behind, with Swiss Franc also firm.

Yen, however, continues to underperform sharply. Governor Kazuo Ueda’s comment that confidence in the BoJ’s outlook is “increasing gradually” supports expectations of a December hike. But the market remains unconvinced that such a move would materially shift rate differentials, leaving JPY at the bottom of the pack. Dollar is the second-weakest major today, with Loonie also under pressure, while Euro and Sterling sit in the middle of the performance table.

In Asia, Nikkei rose 0.14%. Hong Kong HSI is down -1.24%. China Shanghai SSE is down -0.38%. Singapore Strait Times is up 0.02%. Japan 10-year JGB yield fell -0.007 to 1.966. Overnight, DOW fell -0.45%. S&P 500 fell -0.35%. NASDAQ fell -0.14%. 10-year yield rose 0.033 to 4.172.

RBA holds at 3.60% as Bullock signals no cuts, open to 2026 hike

RBA kept the cash rate unchanged at 3.60% today, as markets had fully priced. But the tone from Governor Michele Bullock was firmer than expected, pushing back against speculation of early-2026 easing. “Given what’s happening with underlying momentum in the economy … it does look like additional cuts are not needed,” she said, adding that she does not see rate cuts “on the horizon for the foreseeable future.”

While Bullock confirmed the board did not discuss a rate hike as an active policy option today, she stressed members spent “quite a lot” of time examining what conditions might force them to lift rates next year. The discussion centered on the persistence of inflation and how much further the economy needs to cool before the board can be confident price pressures are returning to target.

Asked whether a February rate increase is plausible, Bullock did not rule it out. She said the RBA will monitor whether inflation remains sticky: if inflation fails to move back toward target, “then I think that does raise questions about how tight financial conditions are and the board might have to consider whether or not it’s appropriate to keep interest rates where they are or in fact at some point raise them.” Any decision, she added, will be made “meeting by meeting.”

The accompanying statement echoed this mildly hawkish stance, noting that recent data show inflation risks have “tilted to the upside.” Although the board judges part of the recent lift in underlying inflation as driven by temporary factors, policymakers admit uncertainty about the new monthly CPI series and acknowledge signs of a “more broadly based pick-up” in price pressures that may prove persistent.

Labor market indicators continue to suggest conditions remain “a little tight.” While the Wage Price Index has eased from its peak, broader wage measures are still running strong, and unit labor costs remain high.

For now, the RBA is signaling a steady policy stance, but the barrier to easing has grown significantly while the door to a potential hike in 2026 is now visibly open.

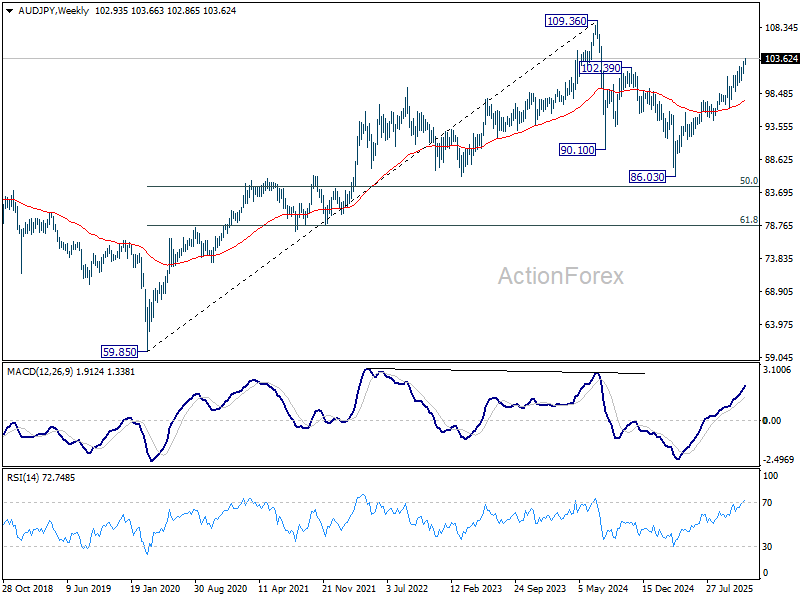

AUD/JPY extends up trend as hawkish RBA fuel upside acceleration

AUD/JPY extended its advance today, with mild acceleration following the RBA’s hawkish hold. Governor Michele Bullock’s explicit dismissal of further rate cuts—and her acknowledgement that rate hikes could be on the table next year—provided the catalyst for renewed Aussie buying. Against this, persistent Yen softness remains a dominant background theme, with markets still doubting that a BoJ hike later this month will materially strengthen the currency.

Technically, the sustained break above the near-term rising channel ceiling signals that an upside acceleration phase is underway. The rise from 86.03 (2025 low) is now tracking toward 161.8% projection of 94.38 to 100.93 from 96.24 at 106.83. Outlook will stay firmly bullish with 100.93 resistance turned support intact, on any pullback.

In the bigger structure, the decisive break of 102.39 structure resistance confirms that corrective decline from 109.36 (2024 high) has ended with a three-wave drop to 86.03. It is still too early to determine whether the current rally is simply the second leg within a larger corrective pattern from 109.36, or the resumption of the long-term uptrend that began at 59.85 in 2020.

Either way, upside is favored while the 55 W EMA (now at 97.50) remains intact, for retesting 109.36. Yet, whether 109.36 gives way will be determined by the RBA’s timeline for tightening.

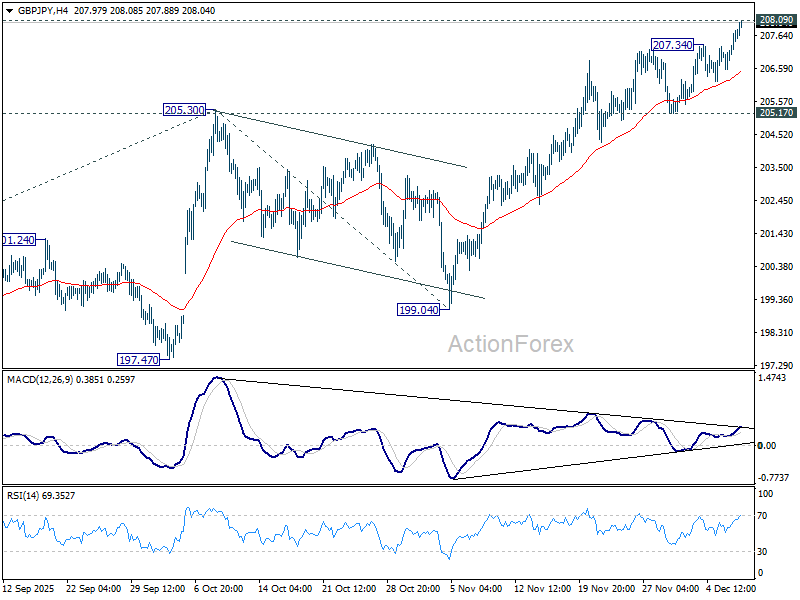

GBP/JPY Daily Outlook

Daily Pivots: (S1) 206.94; (P) 207.37; (R1) 208.16; More…

GBP/JPY’s rally resumed after brief consolidations and it’s now pressing 208.09 high. Intraday bias is back on the upside, and decisive break of 208.09 will confirm larger up trend resumption. Next near term target will be 61.8% projection of 184.35 to 205.30 from 199.04 at 211.98. Outlook will stay bullish as long as 205.17 support holds, in case of retreat.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 199.04 support will dampen this view and extend the corrective pattern with another fall.