Dollar Firm Ahead of NFP, Can Jobs Data Fuel Further Gains? – Action Forex

Dollar continues to dominate the currency markets this week, holding its position as the strongest performer as focus shifts to the upcoming non-farm payroll report from the US. Market reactions to this data will be crucial in shaping financial movements leading up to FOMC rate decision in November. If the employment figures support a standard 25bps rate cut by Fed, risk markets may respond negatively, giving a significant boost to the greenback. Dollar is attempting to reverse its third-quarter losses against major rivals, and supportive NFP data could further enhance this momentum.

Overall in the currency markets, Yen remains the weakest currency this week, influenced by diminishing expectations of a December rate hike by BoJ. Kiwi follows as the second weakest, pressured by firm expectations of a 50 bps rate cut by RBNZ next week. Sterling is the third worst performer after BoE Governor Andrew Bailey raised the possibility of aggressive rate cuts ahead. However, there is prospect for the Pound to rebound significantly if BoE Chief Economist Huw Pill sings a different tune in his speech today.

On the other hand, Canadian Dollar stands as the second strongest currency after the greenback, supported by the rally in oil prices. Developments in the Middle East—specifically whether the US and Israel would strike Iranian oil facilities—are critical factors that could influence the next move in oil prices and, consequently, the Loonie. Aussie is the third strongest, although its upward momentum has slowed as the rally in Hong Kong stock markets pauses. Aussie would await guidance from the reopening of Chinese markets after the holiday next week. Meanwhile, Swiss Franc and the Euro are positioned in the middle of the pack.

Technically, EUR/USD is sitting on an important cluster support level at 1.1001 (38.2% retracement of 1.0665 to 1.1213 at 1.1004). Strong bounce from current level will retain near term bullishness for rallying through 1.1213 and 1.1274 high in the near term. However, decisive break of 1.1001/4 will argue that whole rise from 1.0665 has completed, and risk deeper fall to 61.8% retracement at 1.0874, and possibly below. The market’s reaction today will likely set the tone for EUR/USD’s next major move.

In Asia, at the time of writing, Nikkei is up 0.20%. Hong Kong HSI is up 1.79%. China is still on holiday. Singapore Strait Times is up 0.17%. Japan 10-year JGB yield is up 0.0509 at 0.878. Overnight, DOW fell -0.44%. S&P 500 fell -0.17%. NASDAQ fell -0.04%. 10-year yield rose 0.065 to 3.850.

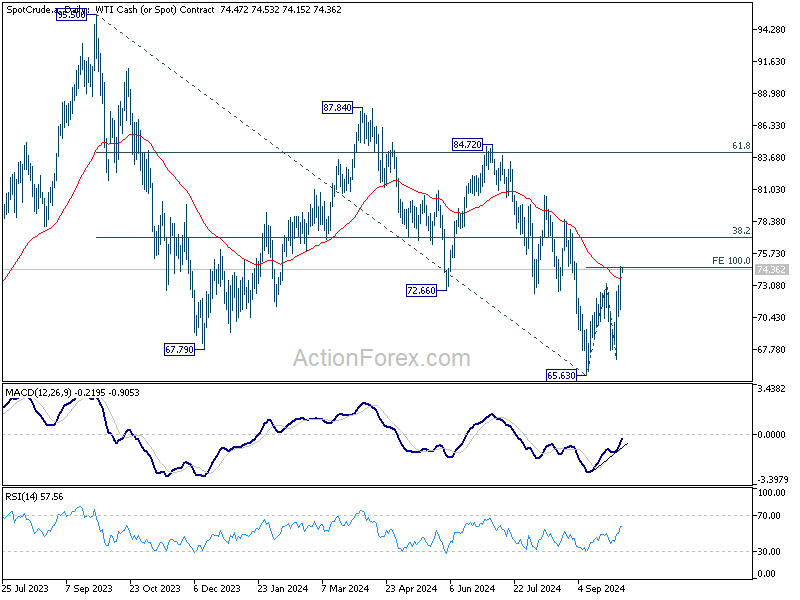

Oil prices rise as US strikes on Iran oil sites, but no runaway rally yet

Oil prices surged as escalating tensions in the Middle East have raised fears of supply disruptions. US President Joe Biden confirmed that he is considering airstrikes on Iran’s oil facilities in retaliation for Tehran’s missile attack on Israel. The growing conflict, already being described as the most severe in the region since the Gulf War, has fueled a sharp rise in oil prices throughout the week. However, the rally has yet to become “runaway”, largely due to OPEC+ holding significant spare capacity, which could be deployed to stabilize the market if needed.

Technically, while WTI’s breach of 55 D EMA is a near term bullish sign, the upside is so far capped by 10% projection of 65.63 to 73.23 from 66.97 at 74.57. Rebound from 65.63 is still seen as a corrective recovery for now. Break of 70.47 minor support will argue that the recovery has completed, and the larger down trend is ready to resume through 65.63 low.

However, decisive break of 74.57 could prompt upside acceleration through key fibonacci level at 38.2% retracement of 95.50 (2023 high) to 65.63 at 77.04. In this case, WTI could be reversing the whole fall from 95.50 and target 61.8% retracement at 84.08.

NFP to back 25bps Fed rate cut in Nov?

The September non-farm payroll report is in sharp focus today, as it plays a critical role in shaping expectations for Fed’s upcoming monetary policy decisions. Currently, markets are pricing in 33% probability of a 50bps rate cut in November, with 67% chance of a 25bps cut. These odds have shifted notably from a week ago, when the probability of a 50bps cut stood at 50%, following comments from Fed Chair Jerome Powell, who indicated two more “normal-sized” cuts are likely by year-end.

It’s important to recall that Fed’s larger-than-usual 50bps rate cut in September was primarily a “catch-up) to their inaction in July. Many Fed officials believed that July would have been a more opportune time to initiate the easing cycle, had they had access to subsequent economic data. Therefore, barring any significant negative surprises in today’s NFP report, Fed is likely to adhere to its current plan outlined in the dot plot, implementing two additional 25 bps cuts in November and December respectively.

NFP is expected to show an increase of approximately 140k in September, with the unemployment rate remaining steady at 4.2%. Average hourly earnings are projected to slow to a month-over-month growth of 0.3%.

Recent related data offers mixed signals: ISM Manufacturing Employment Index declined sharply from 46.0 to 43.9, and ISM Services Employment Index also fell from 50.2 to 48.0. ADP employment report showed private sector job gain of 143k. Four-week moving average of initial jobless claims decreased slightly from 230,000 to 224,000.

Overall, these indicators suggest that while job growth remains robust, the likelihood of a significant upside surprise in today’s NFP release is low.

Risk sentiment and the market’s reaction to the NFP will be pivotal in shaping financial markets for the remainder of October, including currency movements.

Technically, NASDAQ is clearly losing momentum, as seen in 55 D MACD, after hitting 18327.33. Decisive break of 55 D EMA (now at 17587.55) will argue that rebound from 15708.53 has completed. In the bearish case, the corrective pattern from 18671.06 high could have already started the third leg, back towards 15708.53 and possibly below.

Looking ahead

Swiss unemployment rate, France industrial production, Italy retail sales, and UK PMI construction will be released in European session. Later in the day, US NFP will take center stage. Canada will release Ivey PMI.

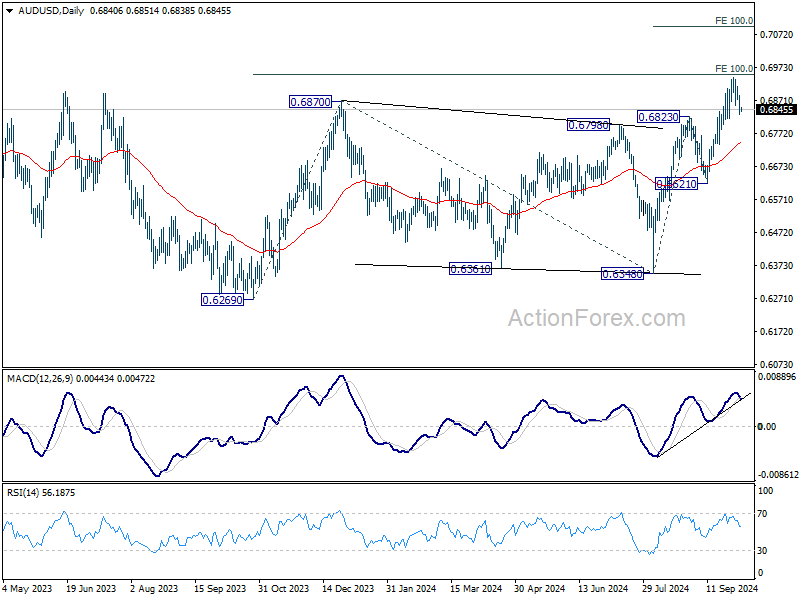

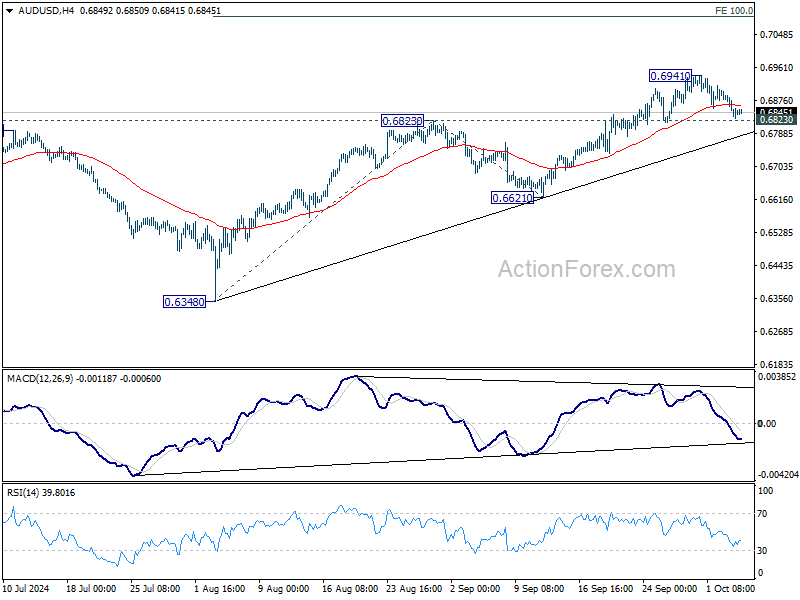

AUD/USD Daily Report

Daily Pivots: (S1) 0.6818; (P) 0.6853; (R1) 0.6877; More...

Intraday bias in AUD/USD remains neutral for the moment. Further rally is still in favor as long as 0.6823 resistance turned support holds. Above 0.6941 will resume the rise from 0.6348 to 100% projection of 0.6348 to 0.6823 from 0.6621 at 0.7096. However, firm break of 0.6823 will indicate rejection by 0.6941 medium term fibonacci level. Intraday bias will be turned back to the downside for 55 D EMA (now at 0.6742) and possibly below.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 0.6870 resistance will target 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941, and then 138.2% projection at 0.7179. This will now remain the favored case as long as 0.6621 support holds.