Dovish ECB Rate Cut Pressures Euro, Gold Breaks to Fresh Record – Action Forex

Euro tumbled broadly after ECB’s decision to cut its deposit rate by 25bps, as widely expected. During the post-meeting press conference, President Christine Lagarde maintained a cautious tone, stressing that ECB is “not pre-committing to a particular rate path.” However, her overall stance leaned dovish, with a clear acknowledgment that “economic activity has been somewhat weaker than expected.”

Lagarde further highlighted that risks to growth remain “tilted to the downside.” Lower confidence could slow the recovery in consumption and investment. Reduced demand for Eurozone exports could potentially adding pressure to economic growth. Additionally, inflation risks could shift to the downside if weak confidence and concerns over geopolitical events continue to curb spending and investment, or if the global economic environment deteriorates unexpectedly.

Overall in the currency markets, Canadian Dollar has emerged as the day’s worst performer, struggling to maintain its brief recovery. Euro follows as the second weakest, with Yen also underperforming. On the other side, Australian Dollar leads the gains, supported by strong employment data, though its upward momentum remains capped. Sterling and Kiwi are also performing well, while Dollar and Swiss Franc occupy middle ground.

Technically, Gold is maintaining steady momentum as it breaches to new record high today. For now, further rally is expected as long as 2638.13 support holds. Next target is 61.8% projection of 2471.76 to 2685.34 from 2604.53 at 2736.62.

In Europe, at the time of writing, FTSE is up 0.47%. DAX is up 0.92%. CAC is up 1.50%. UK 10-year yield is up 0.0228 at 4.091. Germany 10-year yield is up 0.015 at 2.204. Earlier in Asia, Nikkei fell -0.69%. Hong Kong HSI fell -1.02%. China Shanghai SSE fell -1.05%. Singapore Strait Times rose 0.96%. Japan 10-year JGB yield rose 0.0102 to 0.965.

US retail sales rise 0.4% mom in Sep, ex-auto sales jump 0.5% mom

US retail sales rose 0.4% mom to USD 714.4B in September, above expectation of 0.3% mom. Ex-auto sales jumped 0.5% mom to 580.5B, well above expectation of 0.1% mom. Ex-gasoline sales rose 0.6% mom to 633.2B. Ex-auto, gasoline sales rose 0.7% mom to 529.5B.

Total sales for the July through September period were up 2.3% over the sale period a year ago.

US initial jobless claims fall to 241k, match expectations

US initial jobless claims fell -19k to 241k in the week ending October 12, matched expectations. Four-week moving average of initial claims rose 5k to 236k.

Continuing claims rose 9k to 1867k in the week ending October 5. Four-week moving average of continuing claims rose 11.5k to 1843k.

ECB lowers rates by 25bps, cites economic downside surprises impacting inflation outlook

ECB cut its deposit rate by 25 basis points to 3.25% today, as widely anticipated. In its accompanying statement, ECB highlighted that the disinflationary process is “well on track,” with inflation expected to decline to target levels by next year. Recent “downside surprises” in economic activity have also impacted the inflation outlook.

Despite the improvement, domestic inflation remains elevated, driven by persistent wage growth. However, ECB expects labor cost pressures to ease gradually, with profits buffering their inflationary impact.

The central bank reaffirmed its commitment to maintaining rates at restrictive levels for as long as necessary, emphasizing a “data-dependent”, “meeting-by-meeting” approach to future policy decisions, without pre-committing to any specific rate path.

Eurozone CPI finalized at 1.7% in Sep, CPI core at 2.7%

Eurozone CPI in September was finalized at 1.7% yoy, down from August’s 2.2% yoy. Core CPI, which excludes volatile components like energy, food, alcohol, and tobacco, was finalized at 2.7% yoy, slightly lower than August’s 2.8% yoy.

The largest contributor to Eurozone CPI was the services sector, adding +1.76 percentage points to the annual rate, followed by food, alcohol, and tobacco (+0.47 pp). Non-energy industrial goods added +0.12 pp, while energy dragged inflation down by -0.60 pp as prices continued to ease.

On a broader level, EU inflation was also finalized lower at 2.1%, down from 2.4% in August. Inflation rates across member states varied significantly, with the lowest annual rates recorded in Ireland (0.0%), Lithuania (0.4%), and Slovenia and Italy (both at 0.7%).

In contrast, Romania (4.8%), Belgium (4.3%), and Poland (4.2%) registered the highest inflation rates. Compared to August, annual inflation fell in twenty Member States, remained stable in two, and rose in five.

Eurozone goods exports fall -2.4% yoy in Aug, imports down -2.3% yoy

Eurozone goods exports fell -2.4% yoy to EUR 216.7B in August. Goods imports fell -2.3% yoy to EUR 212.1B. Trade balance was a EUR 4.6B surplus. Intra- Eurozone trade fell -4.3% yoy to EUR 183.5B.

In seasonally adjusted term, goods exports fell -0.1% mom to EUR 237.9B. Goods imports rose 1.0% mom to EUR 226.8B. Trade balance reported EUR 11.0B surplus. Intra-Eurozone trade fell -0.5% mom to EUR 215.1B.

Australia’s employment grows 64.1k in Sep, unemployment rate unchanged at 4.1%

Australia’s employment figures for September showed stronger-than-expected growth, with 64.1k jobs added, significantly exceeding forecast of 25.2k. Full-time employment led the gains, rising by 51.6k, while part-time jobs increased by 12.5k.

Unemployment rate remained steady at 4.1%, slightly better than the expected 4.2%. Participation also increased by 0.1% to 67.2%, indicating higher workforce engagement. Monthly hours worked saw a modest rise of 0.3% mom.

Over the past year, employment has grown by 3.1%, outpacing the civilian population growth of 2.5%. This pushed the employment-to-population ratio to a historical high of 64.4%, reflecting robust labor market conditions.

Australia’s NAB business confidence drops to -6 in Q3, inflation pressures ease slightly as margins squeezed

Australia’s NAB quarterly Business Confidence declined from -2 to -6 in Q3. Business conditions also dropped from 5 to 2, with trade conditions falling from 9 to 5, profitability slipping from 2 to 0, and employment conditions down from 5 to 3, signaling softer economic momentum.

Leading indicators weakened, with expected business conditions for the next 3 months falling from 11 to 10, and for the next 12 months from 15 to 12. Forward orders remained negative at -4, and capacity utilization eased from 83.6% to 83.0%. Capital expenditure plans also declined from 24 to 19, indicating reduced investment expectations.

Cost pressures remained persistent. Labor costs grew 1.2%, up from 1.1%, and purchase costs increased to 1.0%, up from 0.9%. Final product price growth, however, slowed from 0.6% to 0.4%, and retail price growth remained steady at 0.7%, suggesting inflationary pressures are easing but at the expense of business margins.

NAB Head of Australian Economics Gareth Spence noted, “Labor cost growth remains elevated, and wage costs are the top issue affecting business confidence. While purchase cost growth persists, the marked drop in final product price growth suggests progress on inflation, though margins are under pressure.”

Japan’s exports fall -1.7% yoy in Sep, first decline in 10 months

Japan’s exports in September dropped by -1.7% yoy to JPY 9.038T, marking the first annual decline in 10 months. This slump was driven by weaker demand from key trading partners. Exports to China, Japan’s largest market, fell by -7.3% yoy, while those to the US dropped by -2.4% yoy.

On the other hand, imports rose modestly by 2.1% yoy to JPY 9.333T, leading to a trade deficit of JPY -294B, the third consecutive monthly shortfall.

In seasonally adjusted terms, there was a small improvement. Exports grew by 2.0% mom to JPY 8.956T, while imports fell by -1.2% mom to JPY 9.144T. This led to a seasonally adjusted trade deficit of JPY -187B.

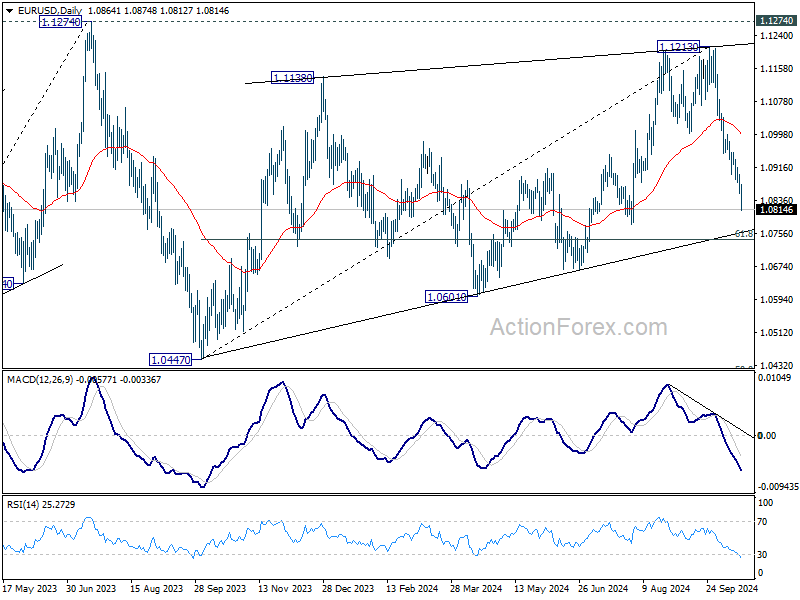

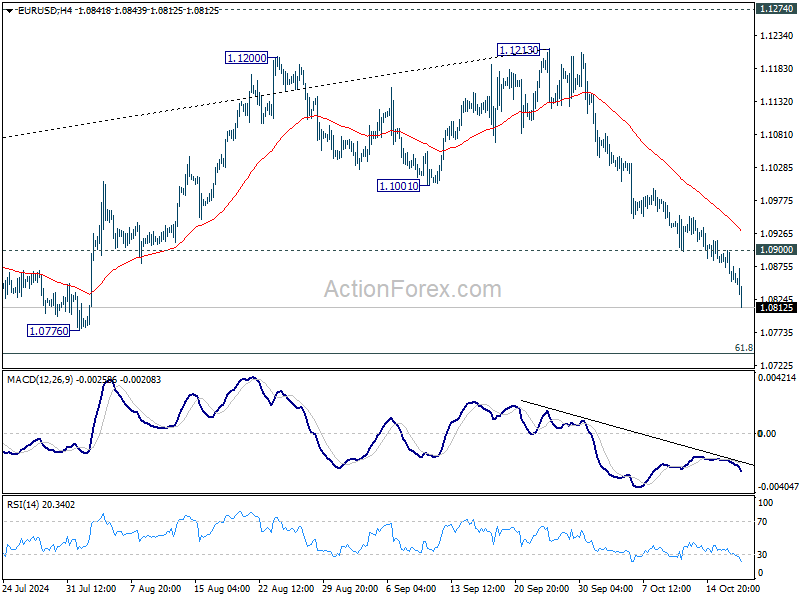

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0843; (P) 1.0872; (R1) 1.0891; More….

EUR/USD’s fall from 1.1213 extends lower today and intraday bias remains on the downside. This decline is seen as the third leg of the corrective pattern from 1.1274. Deeper fall would be seen to 61.8% retracement of 1.0447 to 1.1213 at 1.0740 next. Firm break there will target 1.0601 support next. On the upside, above 1.0900 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, rejection by 1.1274 resistance suggests that corrective pattern from 1.1274 (2023 high) is not completed yet. Instead, decline from 1.1213 might be another falling leg. Sustained break of 55 W EMA (now at 1.0877) will validate this case, and bring deeper fall towards 1.0447 support again. But downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404.