Markets Start With Mild Risk-Off Mood, Central Bank Bonanza Continues – Action Forex

The forex market began the week on a subdued note, with mild risk-off sentiment setting the tone. China’s latest economic data painted a bleak picture, with retail sales significantly underperforming expectations and fixed asset investment experiencing a deeper decline. While industrial production growth met forecasts, it failed to offset concerns about the broader economic slowdown. The lack of impactful measures from the Chinese government continues to weigh on market confidence. Despite repeated pledges for stronger economic support, tangible actions remain elusive, leaving businesses, consumers, and markets uncertain about the path forward.

In Europe, Euro is under pressure following Moody’s downgrade of France’s sovereign credit rating from Aa2 to Aa3, now with a stable outlook. The downgrade highlights concerns over France’s fiscal trajectory, with Moody’s projecting materially weaker public finances over the next three years compared to previous forecasts. This development comes as President Emmanuel Macron appointed centrist François Bayrou as Prime Minister in a bid to stabilize the political climate amid mounting economic challenges. However, Moody’s noted the “very low probability” of substantial fiscal consolidation under the new government, further clouding France’s outlook.

Looking ahead, the focus shifts to three major central bank meetings this week: Fed, BoE and BOJ. Fed’s decision holds the greatest significance as markets seek clarity on the trajectory of rate cuts in 2025 amid persistent inflationary pressures. In addition to central bank meetings, key data releases, including inflation figures, retail sales, and economic sentiment surveys, will be closely watched too.

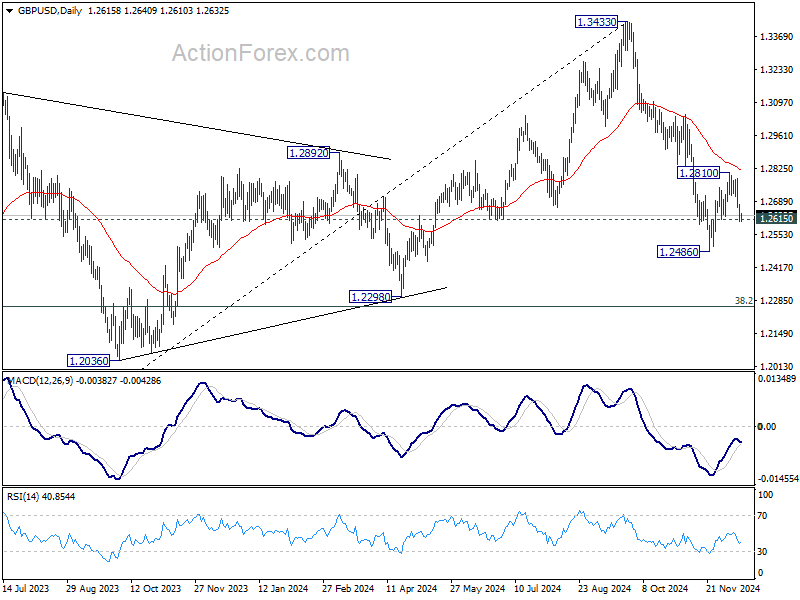

Technically, GBP/USD’s corrective recovery from 1.2486 looks completed at 1.2810 already, after be capped below 55 D EMA. An imminent focus is when GBP/USD would break through 12615 minor support to solidify this bearish case. Then, further fall should be seen through 1.2486 to resume the whole decline from 1.3433 to 1.2298 key structural support next.

Japan’s PMI composite rises to 50.8, stubborn inflation caps growth

Japan’s private sector activity showed a modest improvement in December, driven by a stronger services sector, while manufacturing continued to contract.

PMI Manufacturing index declined from 49.5 to 49.0, marking the fourth consecutive month of contraction. In contrast, PMI Services index rose from 50.5 to 51.4, lifting Composite PMI from 50.1 to 50.8, indicating mild overall growth.

Usamah Bhatti, economist at S&P Global Market Intelligence, pointed out the contrasting trends: “Services firms saw the strongest rise in new business in four months, while goods producers faced a sharper decline in orders.” This divergence highlights persistent weakness in manufacturing amid subdued demand and improving momentum in the services sector.

Inflationary pressures persisted, fueled by the Yen’s weakness, which increased the cost of imported materials. Input prices rose at the fastest pace in four months, while selling price inflation hit its highest level since May, as businesses passed on rising costs to consumers. Bhatti noted, “Stubborn inflation held back a stronger expansion of the Japanese private sector in December.”

Australian PMI composite falls to 49.9, bolsters case for early RBA rate cut

Australia’s December PMI data pointing to a broad-based slowdown. The Manufacturing index fell from 49.4 to 48.2. Services PMI edged down from 50.5 to 50.3. Meanwhile, Composite PMI dropped from 50.2 to 49.9, slipping into mild contraction territory.

Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, noted that the data reflects growing strain across sectors, with manufacturing leading the downturn and services beginning to falter.

Forward indicators presented mixed signals. While business confidence reached its highest level in over two-and-a-half years, new business growth slowed, and unfinished work declined further. Employment gauge showed its first contraction since August 2021.

Muted selling price inflation provides room for RBA to consider rate cuts in early 2024. However, rising cost pressures remain a concern.

NZ BNZ services jumps to 49.5, closer to stability

New Zealand’s BusinessNZ Performance of Services Index rose significantly from 46.2 to 49.5 in November, signaling a move closer to stabilization. However, the index remains under the no-change threshold of 50.0 and well below its long-term average of 53.1.

Key subcomponents offered a mixed picture. Activity/sales improved from 44.4 to 48.6, and new orders/business rose to 49.8, nearing expansion territory. Employment showed only a slight uptick, from 46.4 to 46.8, reflecting continued caution among firms. Stocks/inventories and supplier deliveries moved into expansionary territory at 52.2 and 52.5, respectively, signaling some recovery in supply chain dynamics.

Negative sentiment among respondents eased, with the proportion of unfavorable comments dropping to 53.6% from October’s 59.1%. However, the ongoing concerns over the economic climate and the cost of living remain dominant themes, indicating persistent headwinds for the sector.

Fed’s hawkish cut and signals for 2025, as central bank bonanza continues

Another important week lies ahead for global financial markets, with three major central bank meetings, and economic data converging to shape sentiment. Fed, BoE, and BoJ are set to reveal their latest policy decision. At the same time, a slate of inflation, consumption, and survey data will offer fresh insights into growth and price pressures.

FOMC’s decision tops the agenda. Markets are fully braced for a 25bps rate cut, bringing the federal funds target range down to 4.25–4.50%. With futures assigning over 95% odds of such an outcome, any deviation seems highly unlikely. Yet there are two crucial questions concern Fed’s forward guidance.

First, will policymakers hint at a pause in January, given that the economy remains robust and labor market risks have receded, while inflation remains sticky? Market probability for a pause next month stands at over 80%, so any confirmation or denial in the FOMC statement or Chair Jerome Powell’s press conference will resonate strongly.

Second, the pace of policy easing in 2025 is under the microscope. Fed fund futures suggest around 33% chance of just two more 25bps cuts next year, below the Fed’s September median projection of 3.4%. The updated dot plot and new economic projections will be parsed closely for alignment with market assumptions, as investors seek clarity on how lingering inflation and incoming administration’s fiscal and trade policies might influence Fed’s approach.

Meanwhile, BoE and BoJ are also in the spotlight. BoE is widely expected to keep rates unchanged, with the outlook for four measured rate cuts next year still holding. This meeting may offer little fresh guidance, leaving traders to wait for the February monetary policy summary.

In Japan, BoJ looks increasingly leaning toward maintaining the status quo in the past two weeks, given the lack of urgency to tighten further before its January economic forecasts. While officials consider patience to be a virtue, the BoJ’s track record of unexpected moves means a surprise cannot be fully dismissed.

Beyond central banks, economic data will help define the contours of market sentiment. Investors will scrutinize US PCE inflation, CPI reports from the UK, Canada, and Japan, as well as retail sales data from the UK and Canada.

Additionally, PMIs from major economies will be closely watched. In particular, Eurozone PMIs, Germany’s Ifo and ZEW surveys will test whether Europe’s growth slowdown is stabilizing or deepening. In Asia Pacific, New Zealand’s GDP figures and a batch of Chinese indicators will contribute to the evolving narrative on trade and regional demand.

Here are some highlights for the week:

- Monday: New Zealand BNZ services; Australia PMIs; Japan machine orders, PMIs, tertiary industry index; China industrial production , retail sales, fixed asset investment; Swiss PI; Eurozone PMIs; UK PMIs; Canada housing starts; US Empire state manufacturing, PMIs.

- Tuesday: Australia Westpac consumer sentiment UK employment; Swiss SECO economic forecasts; Germany Ifo business climate, ZEW economic sentiment; Eurozone trade balance; Canada CPI; US retail sales, industrial production, business inventories, NAHB housing market index.

- Wednesday: Japan trade balance; UK CPI, PPI; Eurozone CPI core; US building permits and housing starts, current account, FOMC rate decision.

- Thursday: New Zealand GDP, ANZ business confidence; BoJ rate decision; BoE rate decision; US GDP final, jobless claims, Philly Fed survey, existing home sales.

- Friday: New Zealand trade balance; Germany PPI; UK retail sales; Canada retail sales; US personal income and spending, PCE inflation.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4210; (P) 1.4228; (R1) 1.4252; More…

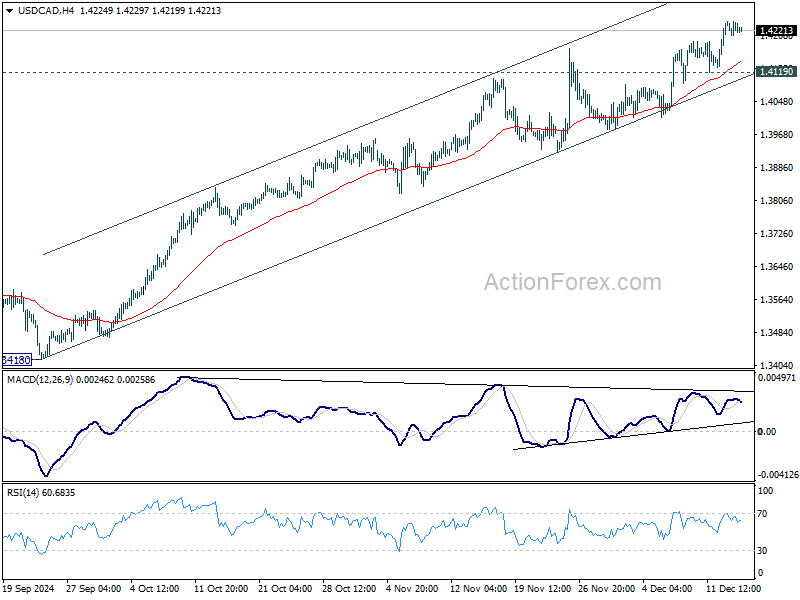

Intraday bias in USD/CAD stays on the upside for the moment. Current rally is part of the larger up trend and should target 1.4391 projection level next. Considering bearish divergence condition in 4H MACD, break of 1.4119 support will indicate short term topping and bring deeper correction.

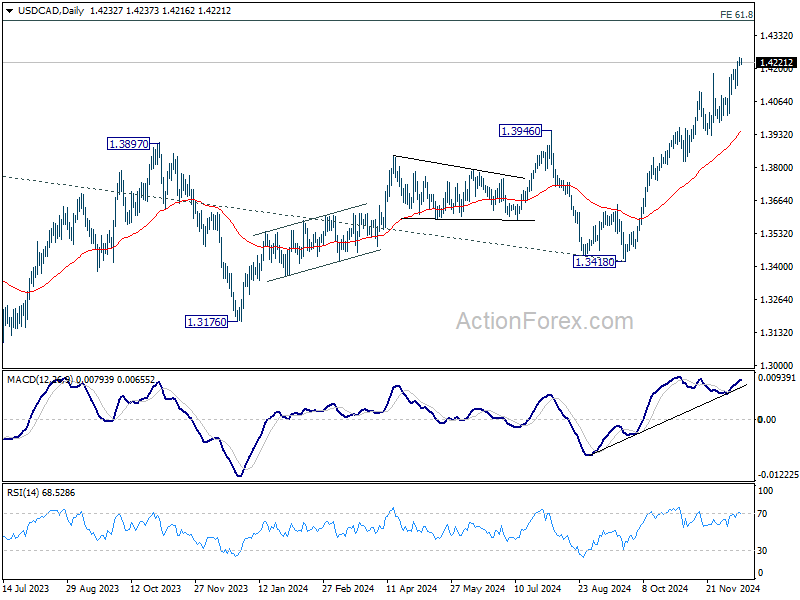

In the bigger picture, up trend from 1.2005 (2021) is in progress. Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Medium term outlook will remain bullish as long as 55 W EMA (now at 1.3706) holds, even in case of deep pullback.