Dollar Weakens on Core Inflation Relief, But Bullish Bias Holds – Action Forex

Dollar extended its near-term pullback in early trading after core inflation data for December came in slightly below expectations, offering a degree of relief to traders and investors. Treasury yields also retreated, with the 10-year yield falling back below the 4.7% mark.

Core CPI rose by 3.2% yoy, down from 3.3%, a result that eased fears of renewed inflationary pressures forcing Fed’s hand back into tightening. While core inflation remains clearly elevated, the data at least suggests that pressures are not intensifying enough to alter Fed’s loosening bias, with pauses in between moves.

Fed fund futures now show 97.3% chance of a hold at the January FOMC meeting, a decision that appears still firmly priced in. Meanwhile, the odds of a rate cut in May have rebounded to 49%, up from 36% the previous day. June remains the most likely timing for a rate cut, with markets assigning nearly 70% probability. This aligns with expectations that Fed might deliver only one rate reduction in 2025.

In forex markets, Dollar is the worst performer of the day so far. Canadian Dollar and Swiss Franc also rank among the weaker currencies. On the other hand, Japanese Yen is leading gains, bolstered by comments from BoJ officials that have reintroduced the possibility of a rate hike at the January meeting. Australian Dollar and New Zealand Dollar also posted solid gains, supported by improved risk sentiment. Euro and Sterling are trading with mixed momentum in middle positions.

From a technical perspective, while the Dollar’s pullback has extended, it remains above key support levels against major counterparts. EUR/USD is capped below 1.0435 resistance, GBP/USD below 1.2486, AUD/USD below 0.6301, and USD/CHF above 0.9007 support. As long as these levels hold, the Dollar’s broader bullish trend remains intact, and the current movement is viewed as a consolidation phase rather than a reversal.

US CPI jumps to 2.9% in Dec, core ticks down to 3.2%

US CPI rose by 0.4% mom in December, surpassing expectations of 0.3% mom and marking an acceleration from the prior month’s 0.3% mom increase. Meanwhile, core CPI, which excludes the more volatile food and energy components, rose by a more subdued 0.2% mom, in line with market expectations but down from the 0.3% mom recorded in November.

Energy prices were the primary driver, rising 2.6% mom on the month and accounting for over 40% of the headline increase. Food prices also contributed to inflationary pressure, advancing by 0.3% mom.

On an annual basis, headline inflation climbed to 2.9% yoy, meeting consensus forecasts and up from November’s 2.7% yoy. Core inflation, however, slowed to 3.2% yoy, slightly below expectations of 3.3% yoy, indicating some easing in underlying price pressures. Notably, energy prices declined by -0.5% yoy, while food prices remained elevated at 2.5% yoy.

Eurozone industrial production rises 0.2% mom in Nov, EU up 0.1% mom

Eurozone industrial production edged up by 0.2% mom in November, falling short of 0.3% mom consensus forecast. While the overall increase suggests resilience in the industrial sector, the performance was uneven across categories. Production rose by 1.5% for durable consumer goods and 1.1% for energy, highlighting strong demand in these areas. Intermediate and capital goods also posted gains of 0.5% each, while non-durable consumer goods saw a marginal uptick of 0.1%.

Across the broader EU, industrial production grew by just 0.1% on the month. The highest monthly increases were recorded in Belgium (+8.7%), Malta (+7.1%) and Lithuania (+4.3%). The largest decreases were observed in Ireland (-5.8%), Luxembourg (-3.9%) and Portugal (-3.4%).

ECB’s Guindos and Villeroy affirm progress on disinflation

ECB Vice President Luis de Guindos highlighted today that disinflation in the Eurozone is “well on track,” reinforcing optimism about the region’s progress toward price stability. While December’s inflation rose to 2.4%, Guindos noted that this increase was anticipated and aligned with ECB’s projections. Domestic inflation remains elevated, but recent easing signals have provided some relief.

Guindos cautioned, however, that risks remain high. “The high level of uncertainty calls for prudence,” he said, referencing global trade frictions that could fragment the global economy further. He also warned about the fiscal policy challenges to weigh on borrowing costs and renewed geopolitical tensions to destabilize energy markets.

Despite weak near-term economic outlook, Guindos expressed cautious optimism, stating, “The conditions are in place for growth to strengthen over the projection horizon, although less than was forecast in previous rounds.”

Meanwhile, French ECB Governing Council member François Villeroy de Galhau echoed a positive sentiment, emphasizing progress against inflation.

“We have practically won the battle against inflation,” he said, projecting that it “makes sense for interest rates to reach 2% by the summer.” However, Villeroy also highlighted risks to France’s 2025 growth forecast of 0.9%, acknowledging that while downside risks persist, a recession remains unlikely.

ECB’s Lane expects service inflation to ease

ECB Chief Economist Philip Lane noted during an event today that services inflation will “come down quite a bit” in the coming months. He attributed much of the anticipated moderation to a slowdown in wage growth. Additionally, firms are reportedly experiencing reduced cost pressures, which should also contribute to easing price increases.

Lane highlighted the challenges of providing a definitive future path for interest rates, citing significant uncertainties in the global economic environment, including escalating trade tensions.

“From our point of view, saying here’s where we think the future rate path is going to be conveys a sense of certainty that we don’t feel,” Lane said, reinforcing the ECB’s cautious stance.

On the topic of exchange rates and their influence on prices, Lane pointed out that while movements in the euro-dollar exchange rate can impact European prices over time, the short-term relationship is less predictable. He noted that in the early stages of a significant currency shift, much of the impact is “absorbed by firms.

“The exchange rate, I think, over time plays a role,” Lane said. “But in terms of the month-by-month, quarter-by-quarter correlation between the exchange rate and import prices is not that stable.”

UK CPI slows to 2.5% in Dec, services inflation down to 4.4%

UK CPI slowed from 2.6% yoy to 2.5% yoy in December, below expectation of 2.7% yoy. Core CPI slowed from 3.5% yoy to 3.2% yoy, below expectation of 3.4% yoy.

CPI goods annual rate rose from 0.4% yoy to 0.7% yoy, while CPI services annual rate fell from 5.0% yoy to 4.4% yoy.

On a monthly basis, CPI rose by 0.3% mom, below expectation of 0.4% mom.

BoJ’s Ueda signals rate hike on the table next week

BoJ Governor Kazuo Ueda today provided further hints that the central bank may be considering a rate hike at its upcoming policy meeting.

Ueda noted, “We are currently analyzing data thoroughly and will compile the findings in our quarterly outlook report. Based on that, we will discuss whether to raise interest rates at next week’s policy meeting and would like to reach a decision.”

Ueda emphasized the significance of Japan’s wage outlook, which has recently been a key focus for policymakers. He pointed to encouraging signals from wage negotiations, which could bolster consumer spending and support BoJ’s inflation target.

Additionally, Ueda remarked that the economic policies of the incoming US administration, coupled with domestic wage trends, would play a pivotal role in determining the timing of any rate adjustment.

The governor’s remarks align closely with those of BoJ Deputy Governor Ryozo Himino, who earlier this week suggested that a rate hike was on the table.

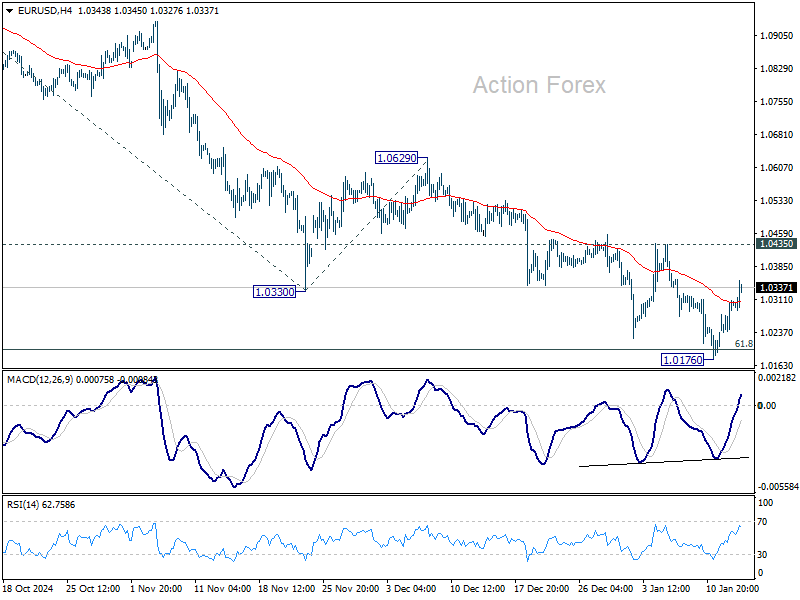

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0261; (P) 1.0286; (R1) 1.0333; More…

EUR/USD’s recovery from 1.0176 extends higher today but stays below 1.0435 resistance. Intraday bias remains neutral while further decline is still expected. On the downside, break of 1.0176 will resume the fall from 1.1213 and target 61.8% projection of 1.1213 to 1.0330 from 1.0629 at 1.0083. However, considering bullish convergence condition in 4H MACD, firm break of 1.0435 will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.1274 (2023 high) should either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. In both cases, sustained break of 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will pave the way back to 0.9534. For now, outlook will stay bearish as long as 1.0629 resistance holds, even in case of strong rebound.