BoJ’s Repeated Hawkish Signals Fuel Yen Rebound, Sterling Falters on Stagnant Growth Data – Action Forex

Yen’s near term rebound gained momentum again today, supported by BOJ Governor Kazuo Ueda’s persistent messaging about a potential rate hike at next week’s policy meeting. Ueda’s repeated remarks are interpreted as laying the groundwork for markets to brace for a monetary policy shift. While recent polls as of last week indicated only a minority expectation of a January hike, the market are clearly undergoing recalibration. However, the current move in Yen against Dollar remains largely corrective, and a sustained reversal in the broader down trend trend would require further confirmation.

Meanwhile, Sterling continues to face mounting pressure after UK GDP data highlighted stagnation in economic activity. Monthly GDP rose just 0.1% in November, falling short of expectations. More importantly, growth over the three months to November was flat. The data has heightened fears of a contraction in Q4. Adding to Sterling’s challenges, new MPC member Alan Taylor struck a dovish tone in his first public speech, noting that while inflation is nearing its endgame, the weakening economy justifies a return to more “normal” interest rates.

For the week so far, Sterling remains the weakest performer among major currencies, with no signs of a sustainable rebound. Dollar is the second worst, as it continues to consolidate recent gains. . Yesterday’s softer-than-expected core CPI reading alleviated fears of a Fed policy reversal toward tightening, while a resurgence in risk appetite has kept the Dollar’s recovery momentum in check. Canadian Dollar rounds out the bottom three.

On the other hand, Australian Dollar, buoyed by risk-on sentiment. However, the Aussie’s inability to extend its rally following robust employment data raises questions about its underlying strength. Yen is the second-best performer, with the potential to advance further as expectations for a BoJ policy shift solidify. New Zealand Dollar rounds out the top three, while Euro and Swiss Franc are mixed in the middle.

Technically, the US stock markets are back into focus with yesterday’s strong rebound. It might be too early to call for resumption of record run in S&P 500. But price actions from 6099.97 are still clearly corrective looking. Downside is also supported above 5669.67 resistance turned support. So, break of 6099.97 remains in favor at a later stage, probably after Trump’s inauguration that clear out some uncertainties over his trade policies, as tariff could be raised just gradually to minimize the shocks to the economy.

UK GDP grows only 0.1% mom in Nov, with mixed sector performance

UK’s economy posted modest growth in November, with GDP increasing by 0.1% mom, but slightly missing market expectations of 0.2%. Nevertheless, this marked a positive turnaround from the -0.1% mom contraction in October.

Sectoral performance was mixed, with services, the largest contributor to the economy, inching up by 0.1% mom, while production fell by -0.4% mom. Construction activity, however, provided a brighter spot, rising 0.4% mom during the month.

Despite November’s modest gains, the broader economic picture remains subdued. Over the three months to November 2024, real GDP showed no growth compared to the three months to August. Services, which account for a significant portion of the UK’s output, stagnated over this period. Production output contracted by -0.7%, offsetting the 0.2% growth seen in construction.

BoJ’s Ueda reiterates rate hike debate for next week’s policy meeting

BoJ Governor Kazuo Ueda indicated today, for the second time this week, that the central bank will “debate whether to raise interest rates” at its upcoming January 23-24 policy meeting. This marks the second time in this week that Ueda has emphasized

Ueda’s comments come as BoJ prepares its new quarterly economic report, which will serve as the basis for its policy decision. While the Governor has not committed to a specific outcome, the repeated message signals that a rate hike is a plausible scenario, barring any significant market shocks tied to the January 20 inauguration of U.S. President-elect Donald Trump.

Market sentiment, nevertheless, remains divided on the timing of the anticipated hike. A recent poll conducted between January 8-15 shows that 59 out of 61 economists expect BoJ to raise rates to 0.50% by the end of March. Yet, only 20 foresee the move occurring at this month’s meeting.

Japan’s PPI holds steady at 3.8% as import prices turn positive

Japan’s PPI held steady at 3.8% yoy in December, meeting market expectations and maintaining the previous month’s pace. Key drivers included a sharp 31.8% yoy rise in agricultural goods prices, fueled by soaring rice costs.

Energy costs also contributed significantly, with electric power, gas, and water prices climbing 12.9% year-on-year. This uptick comes as the government phases out subsidies designed to mitigate rising utility and gasoline prices.

Yen-based import prices turned positive, rising 1.0% yoy after three months of declines. While modest, this reversal underscores the lingering effects of Yen depreciation, which was recorded at -0.1% mom.

Australia’s employment grows 56.3k in Dec, showing continuous resilience

Australia’s labor market displayed resilience in December as employment surged by 56.3k, significantly exceeding expectations of a 15.0k increase. Number of unemployed people also rose by 10.3k, contributing to a slight uptick in the unemployment rate from 3.9% to 4.0%, in line with forecasts.

Participation rate climbed to a record high of 67.1%, up from 67.0%, reflecting an expanding labor force. Additionally, employment-to-population ratio rose by 0.1 percentage point to a new peak of 64.5%, showcasing the labor market’s capacity to absorb more workers. Monthly hours worked increased by 0.5% mom, equivalent to 10 million additional hours.

This data supports the view that the labor market’s earlier signs of easing have stabilized in the second half of 2024. Robust employment growth, consistent levels of average hours worked, and unchanged or lower levels of labor underutilization compared to a year ago affirm the ongoing strength of the job market.

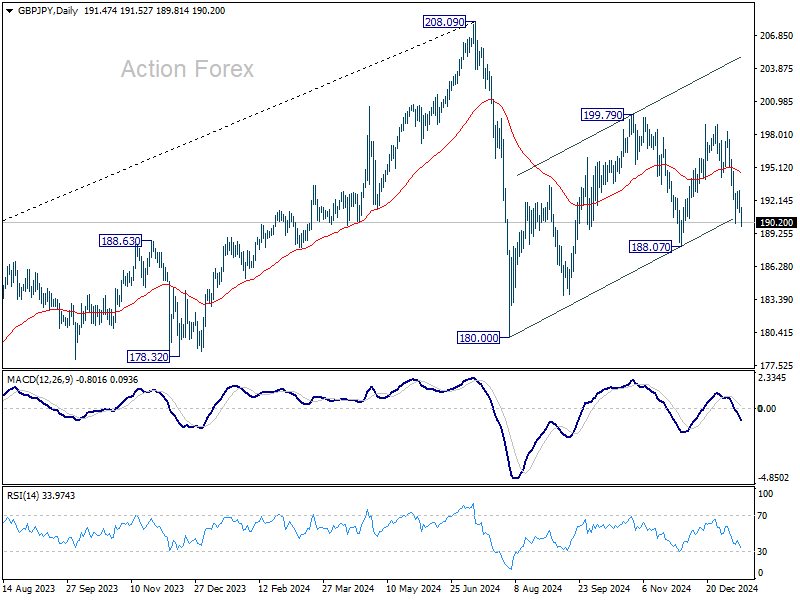

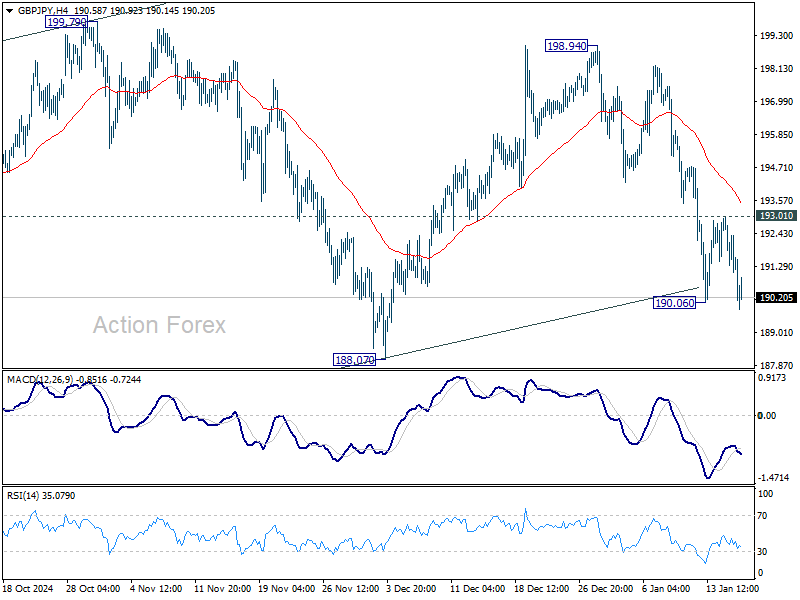

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.78; (P) 191.91; (R1) 192.72; More…

GBP/JPY’s breach of 190.06 temporary low suggests that fall from 198.94 is resuming. Intraday bias is back on the downside for 188.07 support. Firm break there will argue that corrective pattern from 180.00 has finished too, and larger decline from 208.09 might be ready to resume. On the upside, above 193.01 resistance will delay the bearish case and turn intraday bias neutral again.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.