Kiwi Eases as NZ CPI Backs RBNZ 50bps Cut, Dollar Unmoved by Trump’s Continuous Tariff Talks – Action Forex

New Zealand Dollar softened mildly today as Q4 inflation data reinforced the case for continued monetary easing by RBNZ. The central bank has ample room to swiftly bring interest rate from the current 4.25% to neutral, with inflation staying at around mid-point of 1-3% target range for the second straight quarter.

Another 50bps rate cut on February 19 should be solidified. However, beyond this, the scale further rate reductions by RBNZ will depend heavily on domestic disinflationary progress, especially in non-tradeable prices, as the effects of falling tradeable prices fade.

Elsewhere, Dollar’s pull back this week have slowed, but it has yet to stage a convincing recovery. President Donald Trump’s ongoing rhetoric on tariffs continued to draw attention but had little immediate impact on markets. Trump reiterated yesterday his intention to impose a 10% tariff on China, accusing it of enabling fentanyl shipments through Canada and Mexico to the US. He also repeated his threat to target EU with tariffs, calling it the “only way” to achieve trade “fairness”. Markets, however, appeared unfazed, awaiting concrete actions to back Trump’s statements.

Key dates for tariff announcements include February 1, when decisions on 25% tariffs for Canada and Mexico and 10% tariffs on China are expected. For other countries, tariff measures may be delayed until federal trade reviews conclude on April 1. With no immediate actions, Trump’s remarks seem more rhetorical than actionable.

In terms of weekly performance so far, Dollar remains the weakest major currency, followed by Yen and Swiss Franc, reflecting a risk-on sentiment across US and European markets. Kiwi continues to lead gains despite today’s pullback, with Euro and Sterling following suit. Aussie and Loonie are mixed in middle positions.

Technically, a short term bottom is formed at 0.5540 in NZD/USD, just ahead of 0.5511 (2022 low). More consolidations would be seen with risk of stronger recovery. But as long as 55 D EMA (now at 0.5751) holds, larger down trend is expected to resume through 0.5511/40 sooner rather than later. Nevertheless, strong break of 55 D EMA will bring further rebound to 38.2% retracement of 0.6378 to 0.5540 at 0.5860, as the corrective pattern lengthens.

ECB’s Knot supports near-term rate cuts, not convinced of of stimulus mode

Dutch ECB Governing Council member Klaas Knot expressed agreement with market expectations for rate cuts at the January and March meetings, saying he is “pretty comfortable” with them. However, he added it is “too early to comment” on further cuts beyond March.

“As long as the incoming data is in line with our projected return of inflation to target later this year then I think there is little obstacle to making another rate cut,” Knot said. “To change my mind for next week, it’s rather unlikely.”

Knot reiterated ECB’s trajectory toward a neutral policy stance. But he emphasized, “I’m not convinced yet that we need to go into stimulative mode as well.”

He expressed optimism that recent inflation data is “encouraging”. “It confirms the broad picture that we will return to target in the remainder of the year, and hopefully the economy will also finally recover a bit,” he added.

However, Knot flagged risks posed by US trade policies, describing punitive tariffs as a “clear downside risk on the horizon.”

New Zealand CPI unchanged at 2.2% yoy, non-tradeable pressures persist

New Zealand’s CPI rose 0.5% qoq in Q4 2024, in line with expectations, as tradeable inflation increased 0.3% qoq and non-tradeable inflation rose 0.7% qoq. Annually, CPI was unchanged at 2.2% yoy, slightly exceeding the anticipated 2.1% yoy. This marks the second consecutive quarter that inflation has stayed within RBNZ’s target range of 1% to 3%.

The data highlights diverging trends within inflation components. Non-tradeable inflation, which reflects domestic demand and supply conditions and excludes foreign competition, stood at 4.5% yoy, highlighting persistent internal price pressures. Tradeable inflation, influenced by global factors, recorded a -1.1% yoy decline.

Rent prices were the largest contributor to the annual CPI increase, rising 4.2% and accounting for nearly 20% of the overall 2.2% gain. Lower petrol prices, down -9.2% yoy, offset some of the upward momentum, with CPI excluding petrol increasing 2.7% yoy.

Australia’s Westpac Leading Index falls to 0.25%, signals gradual growth pickup

Westpac Leading Index for Australia dipped slightly in December, moving from 0.33% to 0.25%. Westpac noted that while the growth signal remains modest, it reflects a marked improvement from the consistently negative and below-trend readings observed over the past two years. This uptick hints at a gradual lift in economic momentum through the first half of 2025.

Westpac forecasts GDP growth to improve steadily over the course of 2025, projecting a year-end expansion of 2.2%—a notable recovery from the weak 0.8% growth recorded in the year to September 2024. However, the bank noted that while this represents progress, it remains below the economy’s long-term potential.

Westpac highlighted that recent improvements in the Leading Index coincide with mixed signals on broader economy. A key concern for RBA is the labor market, where the “rebalancing” stalled in H2 2024.

“A further slowdown in underlying measures of inflation could still see the Bank ease in February or April but we suspect the RBA will need to be more comfortable about some of these risks before it is prepared to begin easing,” Westpac noted.

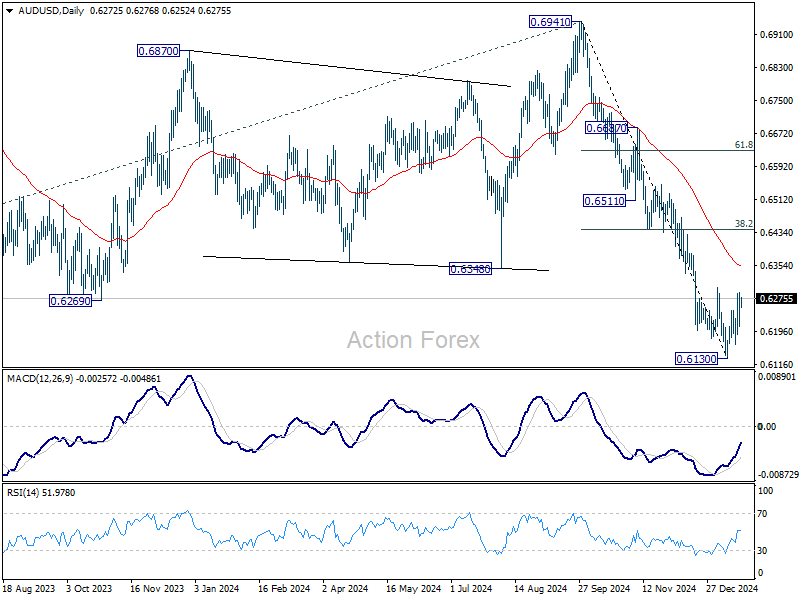

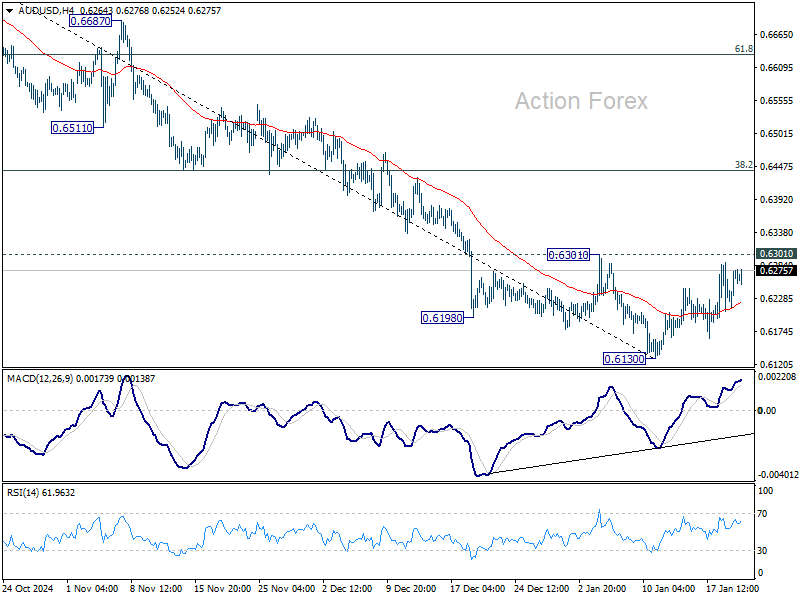

AUD/USD Daily Report

Daily Pivots: (S1) 0.6224; (P) 0.6257; (R1) 0.6305; More...

Intraday bias in AUD/USD stays neutral for the moment. With 0.6301 resistance intact, consolidations from 0.6130 should be relatively brief, and further decline is expected. Break of 0.6130 will resume the fall from 0.6941. However, firm break of 0.6310 will turn bias back to the upside for stronger rebound to 55 D EMA (now at 0.6352), and possibly above.

In the bigger picture, down trend from 0.8006 (2021 high) is resuming with break of 0.6169 (2022 low). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806, In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6545) holds.