Risk Appetite Eases; Markets Await Clarity from US-Japan Negotiations – Action Forex

Global markets are trading with a mildly risk-off tone today, with losses spanning from Asia through to Europe, and US futures following suit. Technology stocks are under pressure, led by AI-chip giant Nvidia, which warned of significant charges stemming from new US restrictions on semiconductor exports to China. The announcement marks the latest escalation in trade tensions between Washington and Beijing, particularly in high-tech sectors where geopolitical and economic interests are increasingly colliding.

Despite the drag from tech, the broader equity pullback remains relatively contained. Some support is being drawn from slightly stronger-than-expected US retail sales data, which helped ease fears of a sharp consumer slowdown. Still, sentiment remains cautious ahead of potential headlines from US-Japan negotiations later today. The discussion is expected to touch on key topics including tariffs, defense cost-sharing, energy policy, and exchange rate management. The results of these talks could offer a clearer view of US President Donald Trump’s broader trade strategy and whether current tariff policies are a prelude to further escalation.

Meanwhile, pressure is mounting on BoJ, with reports suggesting it is preparing to downgrade its economic growth outlook at the April 30–May 1 policy meeting. BoJ’s current forecast of 1.1% GDP growth for fiscal 2025 is likely to be revised downward in response to the mounting impact of US tariffs. While inflation in Japan has been trending upward gradually, central bank officials are now questioning whether the external drag from trade tensions could offset domestic momentum.

In the currency markets, the Swiss Franc is leading gains for the day, followed by Euro and Yen, as investors rotate back into safer assets. Dollar, by contrast, is the day’s weakest performer, followed by Kiwi and Pound. Loonie and Aussie are positioning in he middle.

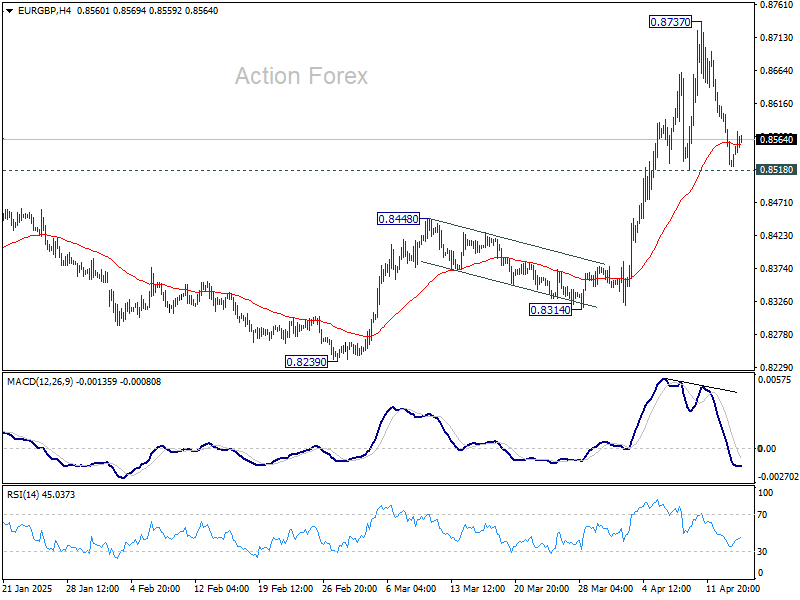

Technically, Sterling has shown some resilience this week, but signs of fatigue are emerging near key resistance levels. EUR/GBP has found support at 0.8518, while GBP/USD is struggling to break above its near-term channel ceiling. Pullback in the Pound from current levels is plausible, though any downside is likely to remain limited unless EUR/GBP breaks back above 0.8737. Conversely, a decisive upside break against both Euro and Dollar could reignite a broader rally in Sterling.

In Europe, at the time of writing, FTSE is down -0.34%. DAX is down -0.54%. CAC is down -0.66%. UK 10-year yield is down -0.0037 at 4.622. Germany 10-year yield is down -0.034 at 2.502. Earlier in Asia, Nikkei fell -1.01%. Hong Kong HSI fell -1.91%. China Shanghai SSE rose 0.26%. Singapore Strait Times rose 1.04%. Japan 10-year JGB yield fell -0.078 to 1.298.

US retail sales rise 1.4% mom in March, above exp 1.3%

US retail sales rose 1.4% mom to USD 734.9B in March, slightly above expectation of 1.3% mom. Ex-auto sales rose 0.5% mom to USD 590.9B, above expectation of 0.4% mom. Ex-gasoline sales rose 1.7% mom to USD 683.4B. Ex-auto & gasoline sales rose 0.8% mom to USD 539.5B.

Total sales for the January through March period were up 4.1% from the same period a year ago.

Eurozone CPI finalized at 2.2% in March, core at 2.4%

Final data confirmed that Eurozone headline inflation edged lower to 2.2% yoy in March, down from 2.3% in February. Core inflation (ex energy, food, alcohol & tobacco) also softened to 2.4% from 2.6%.

Services was the main contributor to price pressures in Eurozone, adding 1.56 percentage points to the annual rate, followed by food, alcohol and tobacco at 0.57 points. Energy contributed negatively, subtracting -0.10 points from the overall figure.

At the EU level, inflation was finalized at 2.5% yoy, an improvement from February’s 2.7% yoy. France registered the lowest annual rate at just 0.9%, while Denmark and Luxembourg followed at 1.5% and 1.5% respectively. In contrast, inflation remains more persistent in Eastern Europe, with Romania (5.1%), Hungary (4.8%), and Poland (4.4%)recording the highest annual rates.

UK CPI falls to 2.6%, both goods and services inflation ease

UK consumer inflation continued to ease in March, with headline CPI slowing to 2.6% yoy, slightly below the expected 2.7% and down from 2.8% yoy in February. On a monthly basis, prices rose 0.3%, also under consensus 0.4% mom forecast.

The decline was broad-based, with annual goods inflation falling to 0.6% yoy from 0.8% yoy and services inflation easing to 4.7% yoy from 5.0% yoy.

Core CPI (excluding energy, food, alcohol and tobacco) edged down to 3.4% as expected, from 3.5% previously.

BoJ’s Ueda: US tariffs nearing bad scenario, policy response may be needed

BoJ Governor Kazuo Ueda warned that US President Donald Trump’s escalating tariff policies have “moved closer towards the bad scenario” anticipated by the central bank.

“We will scrutinise without pre-conception the extent to which US tariffs could hurt the economy,” he said in an interview with Sankei newspaper.

“A policy response may become necessary. We will make an appropriate decision in accordance with changes in developments,” he added.

Nevertheless, Ueda reiterated that BoJ will continue to raise interest rates “at an appropriate pace” as long as economic and price conditions align with its projections.

On inflation, Ueda said domestic food price pressures are expected to ease. He sees real wages turning positive and continuing to rise into the second half of the year, supporting consumption and price stability.

Still, he warned of dual risks: persistent inflation driven by global supply shocks, or a consumption drag caused by the rising cost of living.

Australia Westpac leading index falls as tariff shock starting to weigh

Australia’s Westpac Leading Index slipped from 0.9% to 0.6% in March. Westpac noted that the index has only just begun to reflect the escalating disruptions caused by US President Donald Trump’s reciprocal tariff announcement on April 2.

While the immediate impact on Australia is seen as limited and manageable for now, “some further softening in the growth pulse looks likely in the months ahead”.

Westpac has revised down its growth forecast for Australia in 2025 to 1.9% from 2.2%, citing the accumulating downside risks.

Looking ahead to RBA’s May 19–20 meeting, Westpac expects the deteriorating global backdrop and clearer signs of inflation cooling will prompt a 25bps rate cut.

Moreover, the tone of the meeting is likely to pivot more decisively “away from lingering questions about inflation to downside risks to growth.” Such a shift would lay the groundwork for additional policy easing in the second half of the year.

China Q1 GDP tops forecasts with 5.4% growth

China’s economy started the year on a stronger footing, with GDP expanding by 5.4% yoy in Q1, surpassing market expectations of 5.1%. On a quarterly basis, growth slowed to 1.2% from 1.6% in Q4.

March’s activity indicators were broadly upbeat. Industrial production surged by 7.7% yoy, well above the 5.6% yoy forecast. Retail sales climbed 5.9%, also ahead of expectations of 5.1% yoy.

Fixed asset investment increased 4.2% year-to-date, modestly exceeding projections. However, persistent weakness in the property sector continues to weigh on the recovery narrative. Property investment fell -9.9% in Q1, slightly worse than the -9.8% decline recorded over the first two months of the year. Private sector investment—a key gauge of business confidence—rose only 0.4%.

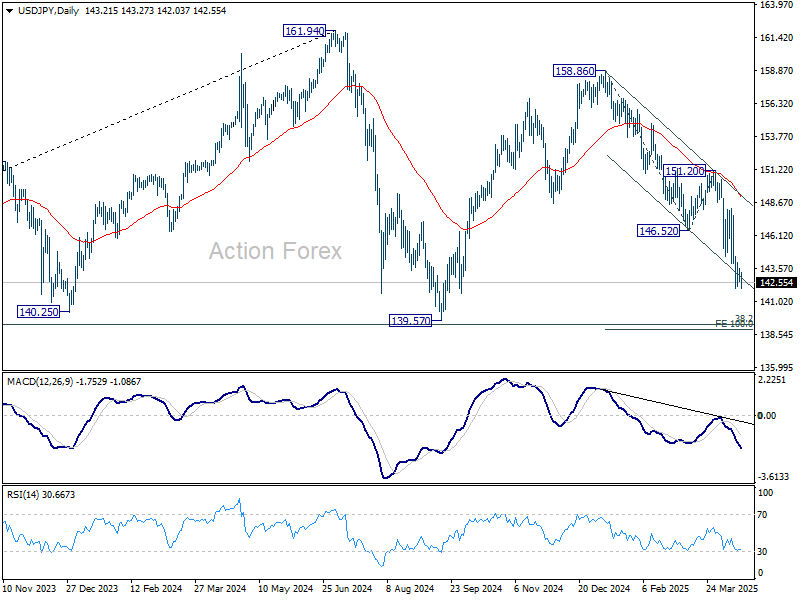

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.71; (P) 143.15; (R1) 143.70; More…

USD/JPY is still bounded in consolidations from 142.05 temporary low and intraday bias remains neutral. Another recovery cannot be ruled out, but outlook will stay bearish as long as 151.20 resistance holds. Below 142.05 will resume the fall from 158.86 to 139.57 support.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.