Markets Pause After Relief Rally, Bessent Tempers De-escalation Optimism – Action Forex

Markets are treading water in the Asian session today, with most asset classes trading mixed and within familiar ranges. While US equities closed higher overnight, much of the early gains were pared back, signaling the fragility of the current risk-on mood. The price action reflects what is often seen during a relief rally—short-lived optimism that fades quickly if underlying uncertainty persists. Hopes of a breakthrough in US-China tariff talks briefly lifted sentiment, but optimism quickly met a dose of reality from Washington.

US Treasury Secretary Scott Bessent pushed back against speculation that President Donald Trump had offered any unilateral gesture to ease tariffs on China. “No unilateral offer—none at all,” Bessent clarified. He acknowledged that current tariff levels are likely unsustainable but stressed that any reduction would have to be mutual. His remarks serve as a reminder that structural obstacles in the trade negotiations remain and that headline-driven rallies may lack staying power.

In the currency markets, price actions are subdued, with all major pairs and crosses trading within yesterday’s ranges. Kiwi is leading gains for the week so far, followed by Dollar and Loonie. On the other side, the safe-haven trio in on the back foot, with Swiss Franc, Yen, and Euro the weakest performers, in line with stabilizing risk sentiment and a broader unwinding of prior defensive flows. Sterling and Aussie are middling.

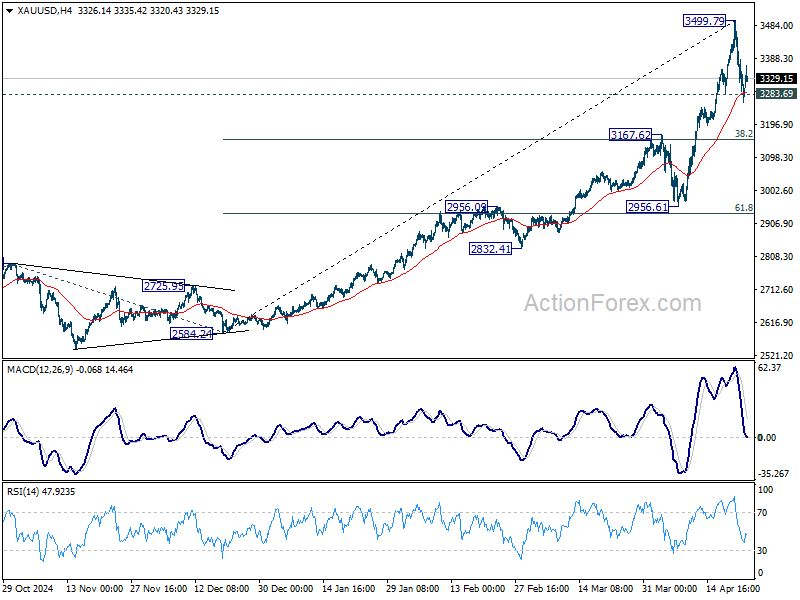

Technically, Gold’s breach of 3283.69 minor support indicates short term topping at 3499.79, just ahead of 3500 psychological level. Some consolidations should be seen in the near term, with risk of deeper pullback. But downside should be contained by 3167.62 cluster support (38.2% retracement of 2584.24 to 3499.79 at 3150.04 to bring rebound. Gold’s long term up trend is expected to continue after the consolidation completes.

In Asia, at the time of writing, Nikkei is up 0.40%. Hong Kong HSI is down -1.08%. China Shanghai SSE is up 0.06%. Singapore Strait Times is up 0.26%. Japan 10-year JGB yield is up 0.001 at 1.325. Overnight, DOW rose 1.07%. S&P 500 rose 1.67%. NASDAQ rose 2.50%. 10-year yield fell -0.02 to 4.387.

Looking ahead, German Ifo business climate is the main feature in European session. Later in the day, US will release jobless claims, durable goods orders, and existing home sales.

IMF: BoJ may delay rate hike on tariff risk, cacks Yen’s haven role

Nada Choueiri, deputy director of IMF’s Asia Pacific Department, told Reuters that BoJ is likely to delay further interest rate hikes as heightened uncertainty from US tariff policy weighs on business sentiment and economic outlook.

She noted that many Japanese firms are now hesitant to move forward with investment plans, opting instead to wait for greater clarity on global trade developments. “This is postponing investment decisions as well,” Choueiri said, adding that the downside risks to both growth and inflation have increased.

“We do see that if our reference scenario materializes, the BOJ interest rate increases will be pushed backwards in time,” she said.

Choueiri also commented on the recent appreciation of Yen, reaffirming its role as a “safe-haven currency”, supported by the country’s economic stability and predictability.

Fed’s Beige Book: Stagnant growth, tariff-driven inflation

The latest Fed Beige Book painted a picture of a stagnating US economy, with activity described as “little changed” across most of the country. Of the 12 Districts, only five reported slight growth, while three saw flat conditions and the remaining four noted modest declines.

However, the most striking theme running through the report was the “pervasive” uncertainty around international trade policy, which was highlighted in nearly all Districts as a key concern weighing on sentiment and business planning.

Inflation pressures remain persistent, with half of the Districts describing price growth as moderate and the other half calling it modest. However, many businesses signaled “elevated input cost growth” tied to tariffs, with some already receiving notices from suppliers warning of upcoming price hikes.

In response, firms have started add “tariff surcharge” or shortening their pricing terms. Still, the ability to fully pass on higher costs is proving difficult in some sectors, particularly for consumer-facing sectors where demand remains sluggish.

ECB’s Lane sees Dollar outflows as rebalancing, not the end of dominance

Speaking at an IIF conference overnight, ECB Chief Economist Philip Lane downplayed concerns over recent portfolio shifts away from US Dollar assets, suggesting the move may reflect a normalization rather than a structural retreat.

Lane noted that allocations are likely moving from an overweight position in Dollar-denominated assets toward a more balanced distribution among global currencies.

He pointed out that US assets had been “priced to perfection” following US President Donald Trump’s election last year, making some degree of reallocation expected as valuations adjust.

Lane also addressed recent outflows from U.S. Treasuries, framing them as part of this rebalancing process. “It can either settle down or invite a deeper rethink,” he said, leaving the door open to further shifts depending on global investor sentiment.

However, he admitted that despite the near-term adjustments, Dollar is still expected to far outweigh Euro in most global portfolios.

ECB’s Knot and Muller downplay tariff impacts on inflation and growth

Dutch ECB Governing Council member Klaas Knot noted that the combination of US tariffs, a stronger Euro, and falling energy prices could push eurozone inflation lower than expected in the short term.

“The strong euro, together with falling energy prices, suggests that the near-term impact might not be so inflationary after all,” Knot said. However, he cautioned that medium-term risks remain, especially if global supply chain disruptions intensify. He supported keeping the ECB’s key policy rate within a neutral range of 1.75% to 2.25%, where it currently stands.

Echoing a cautious but measured tone, Estonia’s ECB Governing Council member Madis Muller acknowledged that the US’s evolving trade policy creates “quite a bit more challenging” outlook for the Eurozone. Nevertheless, he maintained that moderate growth remains achievable, albeit at a slower pace than previously anticipated.

Muller added that he is not forecasting a recession, noting that the impact of trade tensions, while significant, is unlikely to derail the region’s economic recovery entirely. Though, he emphasized the need for optionality, suggesting that more accommodation could be warranted if conditions deteriorate

BoE’s Bailey: We must take tariff-related growth risks very seriously

BoE Governor Andrew Bailey emphasized the growing downside risks to UK growth stemming from US President Donald Trump’s tariff policies. Speaking at an IIF conference, Bailey said, “We do have to take very seriously the risk to growth,” highlighting the UK’s vulnerability as a highly open economy.

He noted that the impact of U.S. trade measures extends far beyond bilateral ties, influencing the UK through broader disruptions in global trade dynamics.

When asked how much the BoE is factoring in the effects of US trade policy, Bailey confirmed that the issue is front and center. “We’re currently working through that because we’ve got an interest rate decision coming in two weeks’ time,” he said.

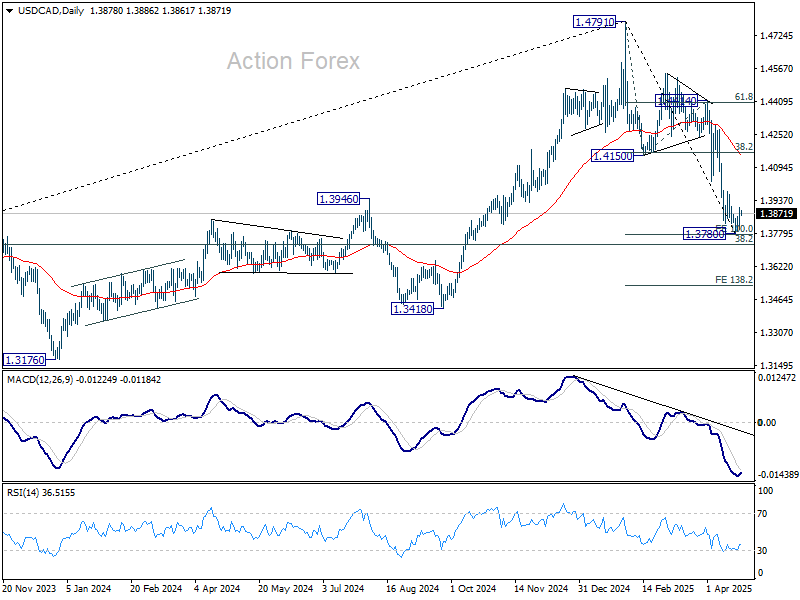

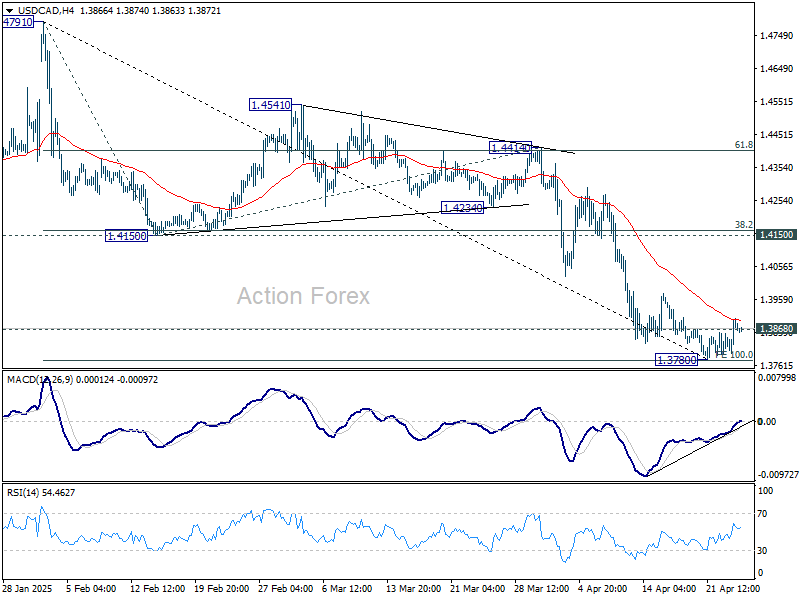

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3818; (P) 1.3861; (R1) 1.3925; More…

A short term bottom should be in place at 1.3780, just ahead of 100% projection of 1.4791 to 1.4150 from 1.4414 at 1.3773, and on bullish convergence condition in 4H MACD. Intraday bias in USD/CAD is mildly on the upside for recovery. But upside should be limited by 1.4150 support turned resistance (38.2% retracement of 1.4791 to 1.3780 at 1.4166. On the downside, firm break of 1.3780 will resume the whole fall from 1.4791.

In the bigger picture, the break of 1.3976 resistance turned support (2022 high) and 55 W EMA (now at 1.3982) indicates that a medium term top is already in place at 1.4791. Fall from there would either be a correction to rise from 1.2005, or trend reversal. In either case, firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.