Glimmers of Trade Optimism Lift Asian Markets, But Concrete Progress Still Elusive – Action Forex

There’s a cautious tone of optimism in Asian markets today, though gains are largely concentrated in Japan, South Korea, and Hong Kong. This moderate rally is being supported by a handful of headlines suggesting incremental movement in global trade diplomacy, even if concrete progress remains limited.

One of the more notable developments comes from a Bloomberg report indicating that China is considering suspending its 125% tariffs on certain US imports, including medical equipment, industrial chemicals, and possibly even aircraft leases. While such a move would mark a significant de-escalation, it remains speculative at this stage.

Adding to the mix, U.S. President Donald Trump pushed back on China’s claims that no talks were underway between Washington and Beijing. Trump insisted that “they had a meeting this morning,” although it was unclear who “they” referred to—even he conceded the ambiguity. With no official confirmation from either side, the market reaction has been understandably restrained.

More tangible, however, was news from Washington of a “very successful” trade meeting between the US and South Korea. Treasury Secretary Scott Bessent expressed unexpected optimism following the bilateral “2+2” talks, suggesting that technical-level negotiations could begin as early as next week. South Korea is hoping to strike a deal with the US by July to avert impending tariffs. The news gave a noticeable lift to South Korean shipbuilding stocks, a sector highly sensitive to global trade developments.

In Japan, Prime Minister Shigeru Ishiba unveiled an emergency economic package designed to cushion the impact of higher US tariffs. The stimulus includes corporate financing support, consumer-focused measures to boost domestic spending, and targeted relief such as subsidies for energy bills and fuel price reductions. This has added to the positive tone in Japanese equities, as the government shows readiness to act swiftly in cushioning external shocks and stabilizing demand.

Currency markets are also reflecting shifting sentiment. Kiwi continues to lead the pack this week, followed by Aussie and Dollar. On the weaker end, safe-haven currencies like Swiss Franc, Yen, and Euro remain under some pressure as investors unwind defensive positions.

Sterling and Loonie are holding in the middle of the pack, awaiting further direction from today’s retail sales reports out of the UK and Canada. Market participants will also be watching for any comments from SNB Chair Schlegel regarding the Franc’s recent strength amid global risk aversion.

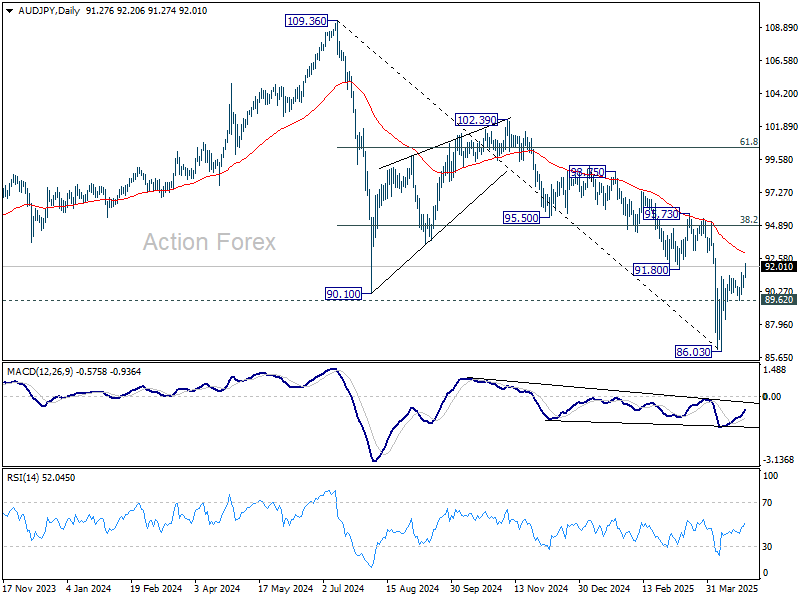

Technically, it’s possible that AUD/JPY’s fall from 102.39 has completed as a five-wave impulse at 86.03, which also marks the completion of the whole three-wave correction from 109.36. For now, further rise is in favor as long as 89.62 support holds. Next target is 55 D EMA (now at 92.97). Sustained trading above there will solidify bullish reversal, and target 38.2% retracement of 109.36 to 86.03 at 94.94 next.

In Asia, at the time of writing, Nikkei is up 1.80%. Hong Kong HSI is up 1.05%. China Shanghai SSE is up 0.05%. Singapore Strait Times is down -0.02%. Japan 10-year JGB yield is up 0.028 at 1.337. Overnight, DOW rose 1.23%. S&P 500 rose 2.03%. NASDAQ rose 2.74%. 10-year yield fell -0.082 to 4.305.

Tokyo CPI core surges to 3.4% in April, strengthening case for BoJ June hike

Inflation in Japan’s capital city surged in April, with Tokyo core CPI (excluding food) accelerating from 2.4% yoy to 3.4% yoy, above the 3.2% yoy forecast. The more domestically focused core-core measure (excluding food and energy) also rose sharply, from 2.2% yoy to 3.1% yoy. Headline CPI jumped from 2.9% yoy to 3.5% yoy.

Despite the upside surprise, BoJ is still expected to hold rates steady at its May 1 policy meeting as it gauges the broader impact of recent US tariffs and awaits progress in ongoing trade negotiations. However, with inflation gathering pace across key categories, market expectations are shifting toward a rate hike as soon as June.

BoJ’s Ueda says G20 peers aAlign on tariff risks to trade and sentiment

BoJ Governor Kazuo Ueda acknowledged growing global concern over the economic impact of tariffs, following discussions with international counterparts at a G20 finance ministers’ meeting.

Speaking at a press conference, Ueda said many global policymakers “roughly had the same view” that tariffs weigh on trade activity, weaken business sentiment, and increase market volatility. He noted that these factors will be integrated into BoJ’s evolving assessment of Japan’s economic outlook and monetary policy.

Ueda reaffirmed BoJ’s intention to raise interest rates gradually, provided underlying inflation continues to converge toward the 2% target. But he emphasized a cautious, data-dependent approach.

“We would like to scrutinize various data that comes in, without pre-conception,” he said.

Fed’s Kashkari: Trade shift could raise US borrowing costs

Minneapolis Fed President Neel Kashkari highlighted the economic risks tied to shifts in the US trade balance and lingering uncertainty from ongoing trade disputes.

Speaking at an event overnight, Kashkari noted that the US’s persistent trade deficit has long been supported by foreign capital inflows, which have helped keep interest rates low. However, if the U.S. were to move toward a trade surplus and lose its status as the “singular premier destination for capital”, borrowing costs could rise, along with the neutral interest rate.

Kashkari emphasized that resolving current trade disputes with major partners could provide much-needed clarity for businesses and households, reducing the “extraordinary uncertainty” they currently face.

He warned that a collective loss of confidence could quickly ripple through the economy, “really bring down the economy, really slow it down” and potentially triggering job losses. While such a downturn hasn’t materialized yet, Kashkari said it’s a risk he is “keeping a close eye on.”

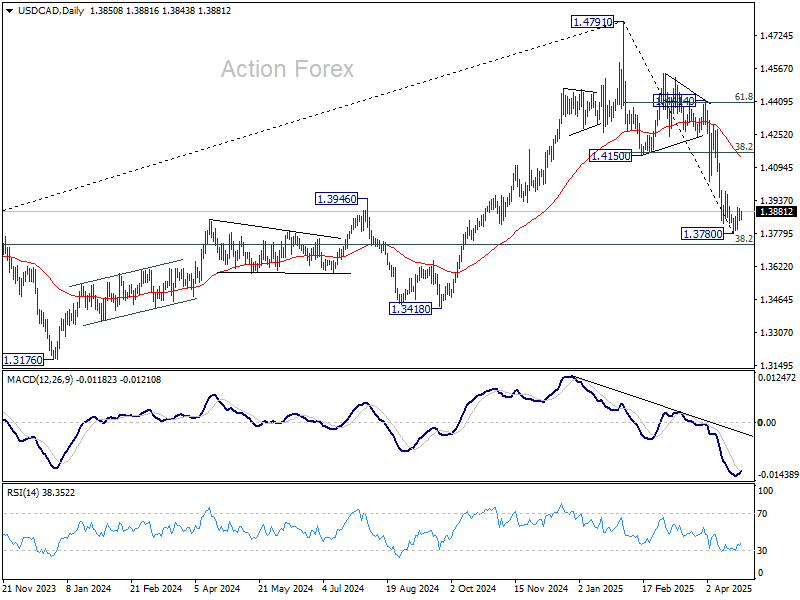

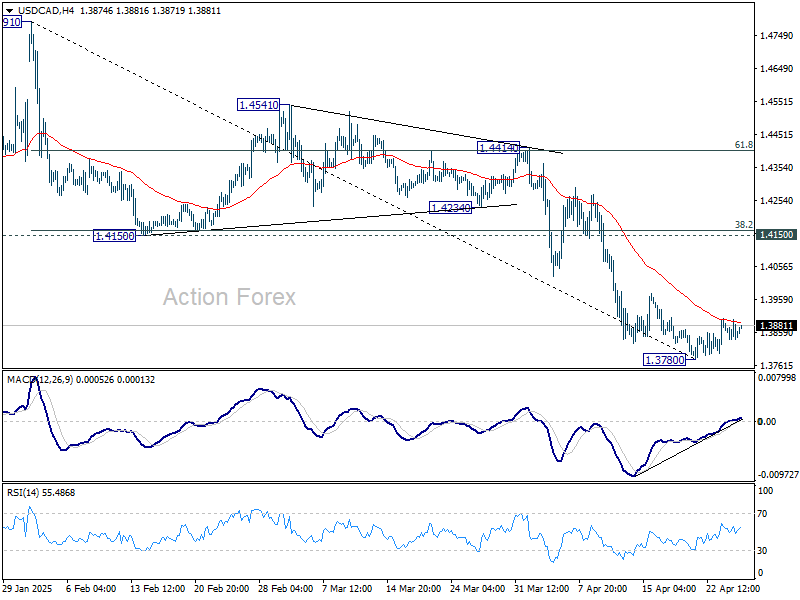

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3830; (P) 1.3864; (R1) 1.3889; More…

Intraday bias in USD/CAD stays mildly on the upside at this point. Recovery from 1.3780 short term bottom could extend higher. However, upside should be limited by 1.4150 support turned resistance (38.2% retracement of 1.4791 to 1.3780 at 1.4166. On the downside, firm break of 1.3780 will resume the whole fall from 1.4791.

In the bigger picture, the break of 1.3976 resistance turned support (2022 high) and 55 W EMA (now at 1.3982) indicates that a medium term top is already in place at 1.4791. Fall from there would either be a correction to rise from 1.2005, or trend reversal. In either case, firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.