Global Risk Sentiment Brightens, But Caution Lingers Around US Assets – Action Forex

Global risk sentiment showed further improvement last week, with stock markets around the world posting impressive gains. Although headlines continued to focus on the confusing state of U.S.-China trade tensions, there was quiet but notable progress on multiple trade fronts, including US talks with Japan, South Korea and India.

US equities rebounded alongside the global rally even though they still lack the decisive momentum needed to confirm that a durable bottom has been established. European markets, on the other hand, painted a far more encouraging picture.

The strength of the rebound in European equities suggests that the worst of the April selloff may already be behind us. Moreover, there is a growing sense that the sharpest phase of the tariff crisis has passed, and that incremental improvements could take root from here.

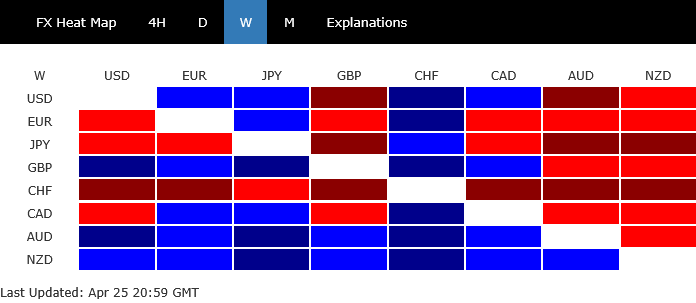

The shift in sentiment was clearly reflected in the currency markets too. Kiwi ended the week as the strongest performer, followed by Aussie and Sterling. All three currencies benefited from the rebound in risk appetite, with investors rotating out of safe-haven assets and into higher-yielding or growth-linked currencies. On the other end, the safe-haven trio—Swiss Franc, Yen, and Euro—underperformed, as investors rotated away from defensive assets amid easing fears. Dollar and Loonie finished in the middle of the pack.

While the equity rally suggests a return of broader risk appetite, investor interest in US assets has yet to fully recover. This is likely due to ongoing concerns over U.S. policy consistency and the uncertain path for trade negotiations. Until clearer signals emerge from Washington and stronger technical confirmations develop in US stock markets, Dollar may continue to lag behind the recovery seen elsewhere.

Markets Rally on Trade Progress, But Major Hurdles with China and EU Remain

Global stock markets extended their strong rally last week. There seems to be growing optimism that the worst phase of the tariff crisis may be behind us, at least for now. Trade negotiations appear to be picking up momentum across several fronts, offering hope for partial resolutions. Recent economic data, particularly PMI surveys from the Eurozone and the US, suggest that businesses have been bracing well for uncertainty, cushioning the blow from trade tensions.

In an interview with Time magazine on Friday, US President Donald Trump said he expects “many” trade deals to fall into place over the next three to four weeks. Positive signals are emerging from several bilateral channels too. Japan’s Economy Minister Ryosei Akazawa is set to visit Washington this week for a second round of talks. US Treasury Secretary Scott Bessent has hinted that a US-South Korea trade deal could be finalized as early as next week. US and India are reported to have agreed on the terms for a bilateral deal covering trade in goods, services, and critical sectors like e-commerce and minerals. Switzerland also announced it was among a group of 15 countries given “somewhat preferential treatment” in tariff talks, with Swiss President Karin Keller-Sutter indicating that the 90-day truce could be extended for active negotiating partners.

However, not all fronts are moving smoothly. Despite initial discussions, talks between the US and the EU have yet to yield tangible compromises. Progress remains slow, even in setting a basic framework for formal negotiations. The slow movement with Europe highlights that achieving broad global de-escalation is far from guaranteed.

Meanwhile, the situation with China remains the murkiest. Rumors continue to swirl about informal discussions, but no clear confirmation has been provided by either side. Trump insists that some communication with Beijing is ongoing, while Chinese officials deny that any talks are happening. Although there were earlier hopes for de-escalation, Trump has reiterated that tariffs on China will remain in place unless “they give us something substantial.”

Without a clear breakthrough or even a defined negotiation channel, US-China trade tensions remain a major overhang for global markets, tempering some of the broader optimism.

European Strength Offers Hope, Caution Persists for US Indexes

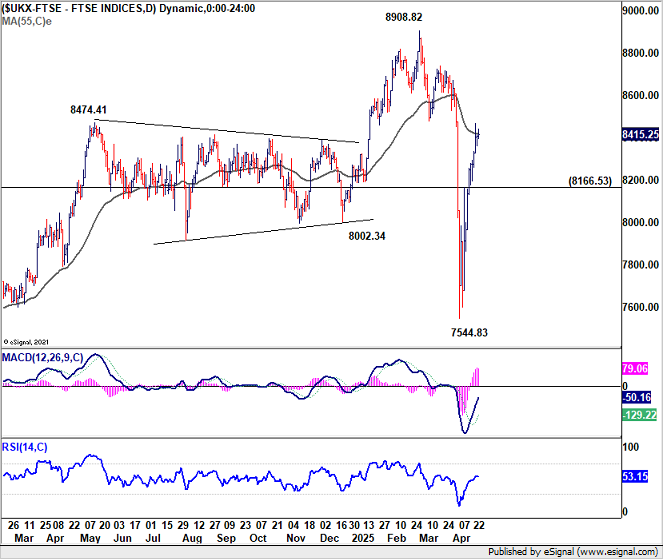

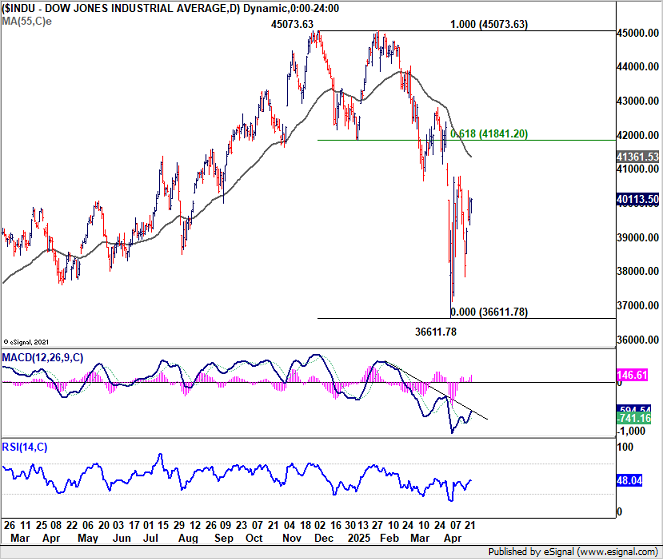

While US stocks have staged a strong rebound recently, the technical backdrop remains somewhat unconvincing. The recovery lacks decisive confirmation, particularly in DOW. In contrast, the outperformance seen in European markets is offering hope that the worst of the market correction could already be behind us. Particularly in the UK and Germany, technical signals suggest that early April’s steep selloff may have been a medium-term shakeout rather than the start of a long-term bearish trend.

In the UK, FTSE ‘s breach of 55 D EMA (now at 8420.51) and break of 55 W EMA (now at 8260.66) suggest that corrective fall from 8900.82 has already completed at 7554.83. Price actions from 8908.82 is likely just a medium term consolidations pattern, rather than a long term bearish trend reversal. The range of the consolidations should be set between 38.2% retracement of 4898.79 to 8902.82 at 7376.99 and 8908.82.

Nevertheless, for the near term, while further rise could be seen as long as 8166.53 support holds, FTSE should start to lose momentum above 55 D EMA.

Germany’s DAX tells a similar story. The index’s corrective fall from the 23476.01 has likely completed at 18489.91. What we are seeing now is a medium-term consolidation rather than a full trend reversal. The range is set between 38.2% retracement of 8255.65 to 23476.01 at 17661.83 and 23476.01.

For the near term, further rise is in favor as long as 21044.61 support hold. But DAX should lose momentum as it approaches 23476.01 high.

Turning to the US, developments in Europe suggest that DOW may eventually find solid support from 38.2% retracement of 18213.65 to 45073.63 at 34813.12 to contain downside even in case of another fall, should another selloff occur. Still, firm break of 55 D EMA (now at 41361.53) is needed to indicate that fall from 45703.63 has completed. Or risk will remain on the downside for the near term.

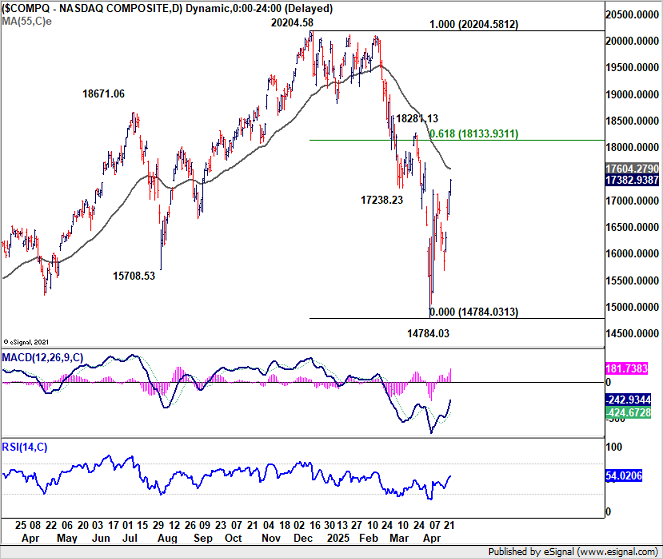

NASDAQ’s picture is a little bit more promising than DOW. Firm break of 55 D EMA (now at 17604.27) will indicate that fall from 2024.58 has completed at 14783.03, after defending 38.2% retracement of 6631.42 to 20204.58 at 15019.63. That should set the range for medium term consolidations for NASDAQ.

Dollar Struggles Despite Risk Stabilization, Policy Uncertainty Remains a Drag

While risk sentiment has shown signs of stabilizing in global markets, and even hints at a return of risk appetite, this does not necessarily imply a renewed interest in US assets. In particular, both the Dollar and US. Treasuries continue to face headwinds until investors see more policy consistency from the Trump administration. Markets remain wary of abrupt shifts in trade policy, tariff threats, and broader economic strategies, which cloud the overall investment climate for Dollar-based assets.

Another important factor is the evolving US trade balance. Should the Trump administration succeed in narrowing the US trade deficit, there could be a meaningful structural impact on the demand for Dollar-denominated assets. A narrower deficit would mean fewer surplus Dollars circulating abroad to be recycled into US Treasuries and other assets, potentially pushing yields higher and softening the Dollar’s appeal at the same time, particularly if fiscal deficits remain large.

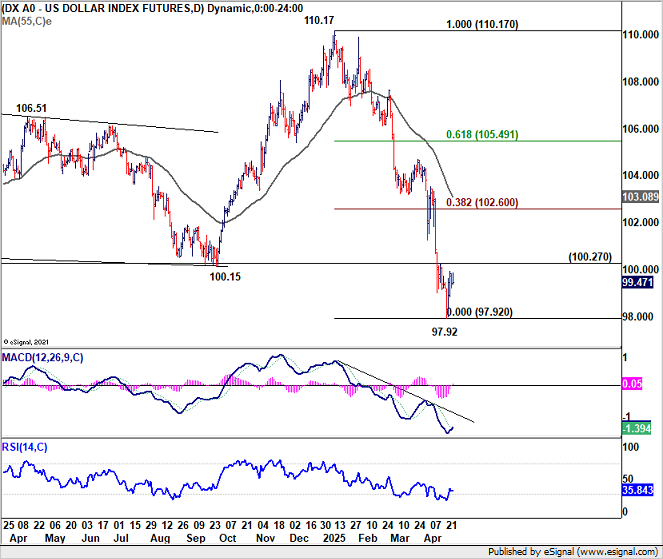

Technically, Dollar Index’s recovery from 97.92 short term bottom is lacking decisive momentum. As long as 100.27 resistance holds, near term risk will remain on the downside for another fall through 97.92 sooner rather than later. Break of 97.92 will pave the way to 100% projection of 114.77 to 99.57 from 110.17 at 94.97 next.

Nevertheless, firm break of 100.27 would set the stage for stronger rebound to 38.2% retracement of 110.17 to 97.92 at 102.60, even still as a corrective move.

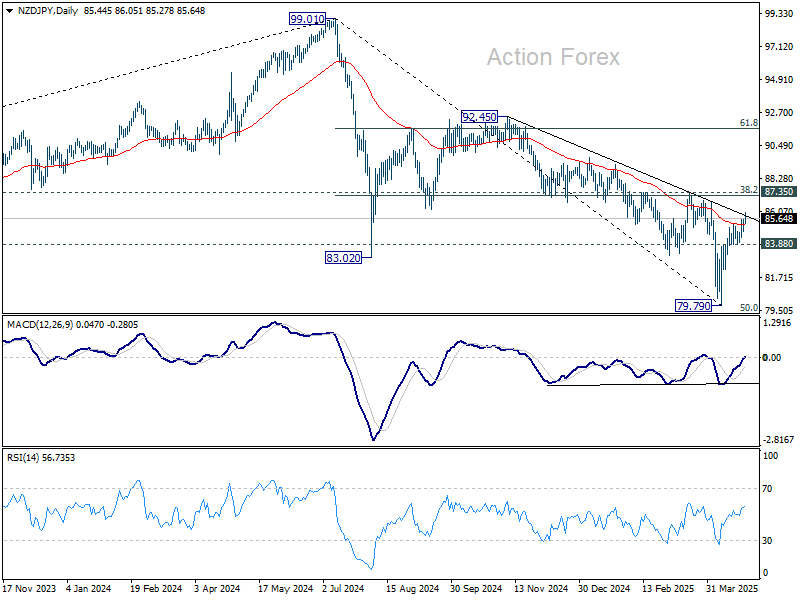

NZD/JPY Extends Rebound, Bullish Reversal Hinges on 87.35 Break

NZD/JPY extended the rebound from 79.79 last week as risk sentiment continued to improve. The breach of falling trend line resistance is a tentative sign that fall from 92.45 has completed at 79.79. Further rise is now in favor as long as 83.88 support holds.

On the upside, decisive break of 87.35 cluster resistance (38.2% retracement of 99.01 to 79.79 at 87.13) will argue that corrective decline from 99.01 has already completed too. Further rally should then be seen to 61.8% retracement at 91.66.

However, rejection by 87.13/35 will keep near term outlook bearish. Break of 83.88 support will bring retest of 79.79, and possibly resumption of the down trend from 99.01 too.

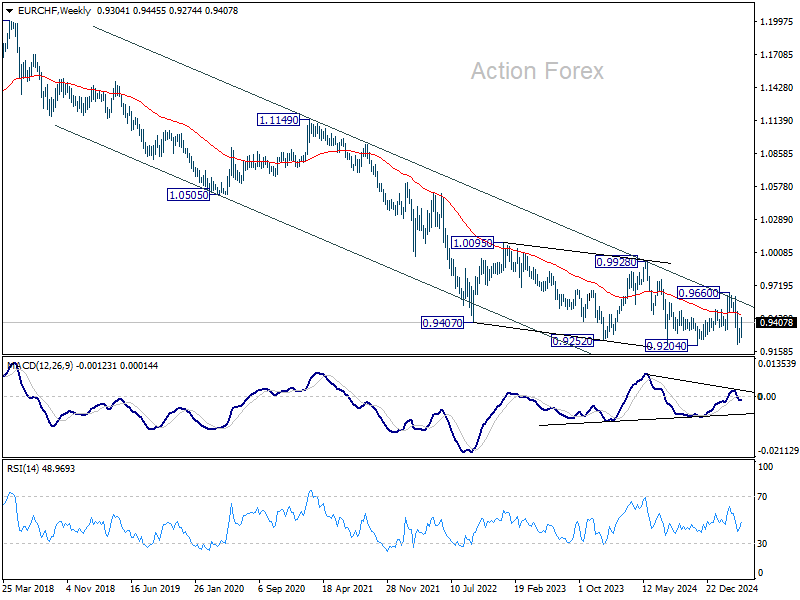

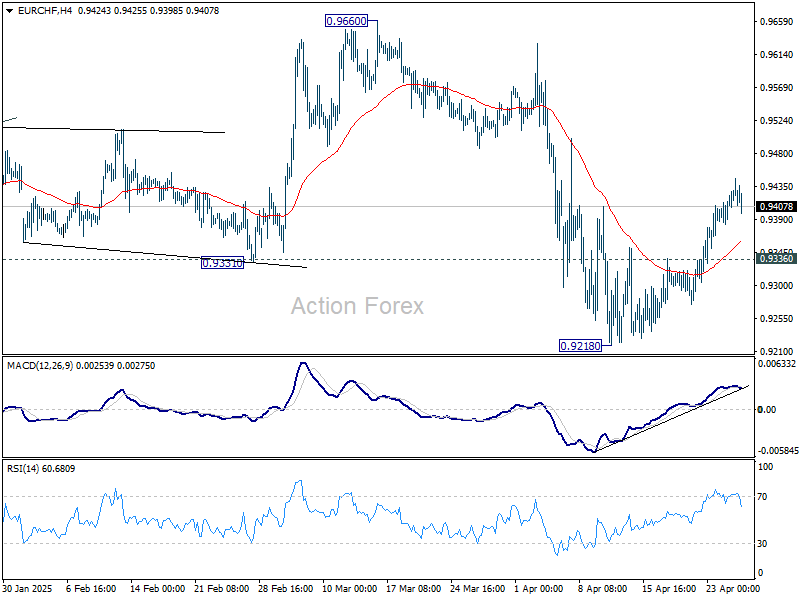

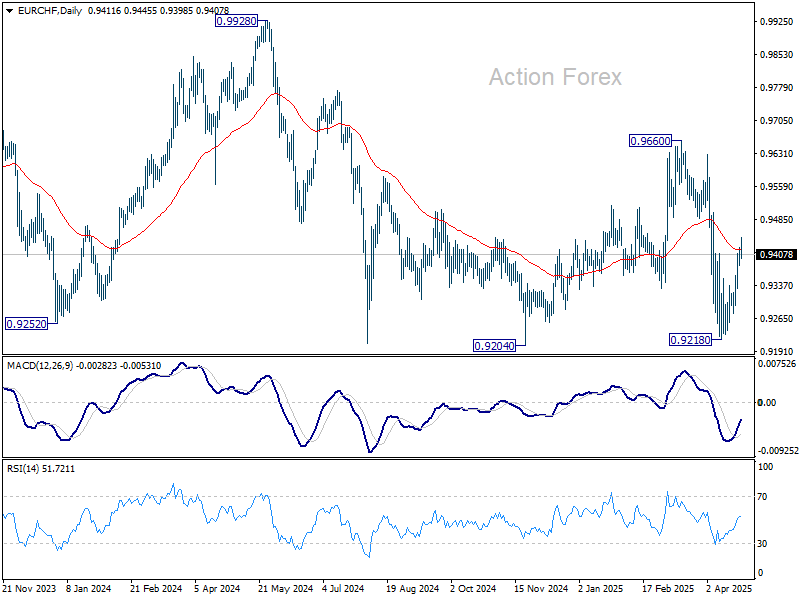

EUR/CHF Weekly Outlook

EUR/CHF’s stronger than expected rebound last week suggests that fall from 0.9660 has already completed at 0.9218, ahead of 0.9204 low. Rebound from 0.9218 is either a corrective move, or the third leg of the pattern from 0.9204. In either case, further rally is expected this week as long as 0.9336 support holds, towards 0.9660. However, break of 0.9336 will bring retest of 0.9204/18 support zone.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9555) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

In the long term picture, overall long term down trend is still in force in EUR/CHF. Outlook will continue to stay bearish as long as 55 M EMA (now at 0.9962) holds.