Markets Stay Subdued Ahead of Big Data and Earnings; Trade Talks Remain in Focus – Action Forex

Trading remains notably subdued across global financial markets today as investors adopt a cautious stance. On deck are quarterly earnings from four of the “Magnificent Seven”—Amazon, Apple, Meta Platforms, and Microsoft. On top of that, key releases including US and Eurozone GDP, US non-farm payrolls, and Eurozone CPI flash inflation data will provide critical insights into the impacts of recent trade tensions on the economy.

Sentiment is caught between two powerful forces. On the pessimistic side, growing risks of a global recession stemming from escalating trade disruptions are weighing heavily. According to a Reuters poll, three-quarters of economists have downgraded their 2025 global growth forecasts, cutting the median forecast to 2.7% from 3.0% just a few months ago. Alarmingly, 60% of surveyed economists rated the risk of a global recession this year as either “high” or “very high.” Investors will be keenly watching this week’s economic releases for validation—or rejection—of these rising recession fears.

However, there is also a glimmer of optimism. Any tangible breakthrough in ongoing trade negotiations could quickly improve sentiment. US Treasury Secretary Scott Bessent emphasized that “it’s up to China to de-escalate,” highlighting that China’s trade surplus with the US makes their current tariff burden “unsustainable.” Bessent also hinted that India could soon become one of the first countries to finalize a new trade agreement with the US, keeping markets alert for needed boost to sentiment.

In the currency markets, Kiwi is the weakest performer of the day so far, followed by Swiss Franc and Loonie. On the stronger side, Ten is leading gains, followed by Sterling, and then Aussie. Dollar and Euro are sitting in the middle of the pack.

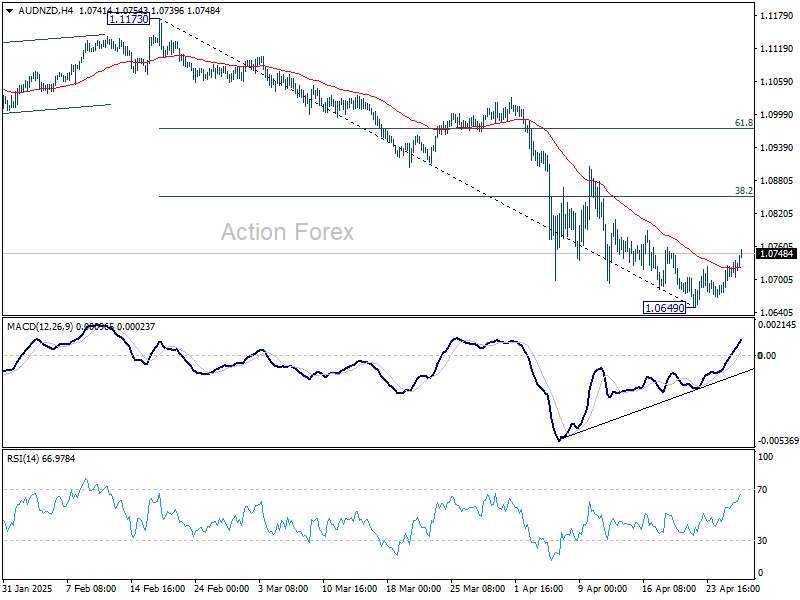

Technically, AUD/NZD’s extended recovery suggests that a short term bottom was formed at 1.0649, on bullish convergence condition in 4H MACD. Stronger rally is in favor for the near term. But outlook will stay bearish as long as 38.2% retracement of 1.1173 to 1.0649 at 1.0849 holds. Another decline through 1.0649 is expected at a later stage once the current consolidation completes—especially if RBA moves toward faster rate cuts in response to weakening economic conditions.

In Europe, at the time of writing, FTSE is up 0.16%. DAX is up 0.55%. CAC is up 0.87%. UK 10-year yield is up 0.039 at 4.521. Germany 10-year yield is up 0.052 at 2.515. Earlier in Asia, Nikkei rose 0.38%. Hong Kong HSI fell -0.04%. China Shanghai SSE fell -0.20%. Singapore Strait Times fell -0.31%. Japan 10-year JGB yield fell -0.025 to 1.315.

IMF warns US tariffs to outweigh Germany’s stimulus, recommends just one more ECB cut

Higher infrastructure spending in Germany will offer some support to Europe’s growth outlook, but it won’t be enough to offset the damage caused by US tariffs, according to Alfred Kammer, director of the European department at the IMF.

Speaking to CNBC, Kammer stressed that “it’s the tariffs and the trade tensions which weigh on the outlook rather than the positive effects on the fiscal side.”

He noted that the IMF has delivered a “meaningful downgrade” to growth forecasts for Europe’s advanced economies and an even steeper downgrade for the emerging Eurozone countries over the next two years. The IMF cut its Eurozone growth forecasts by -0.2% for each of the next two years, now projecting growth of just 0.8% in 2025 and 1.2% in 2026.

Kammer also outlined a clear policy recommendation for ECB. Acknowledging the success of the disinflation efforts, he suggested that ECB has room for “one more 25-basis-point cut in the summer,” after which it should hold rates steady at around 2%, barring major shocks.

ECB’s Villeroy reaffirms gradual rate cut, sees no recession risk

French ECB Governing Council member Francois Villeroy de Galhau expressed confidence today that there is no imminent recession risk for either France or Europe, while inflation continues to decline.

Speaking to RTL Radio, Villeroy also reaffirmed that the ECB retains “a gradual margin for rate cuts”, despite global uncertainties.

Villeroy also issued a strong warning about the risks stemming from US trade policies. He criticized the administration’s protectionist stance, saying it was “playing against the US economy and unfortunately also against the world economy.”

He stressed that protectionism ultimately leads to “less growth and more inflation.”

China reaffirms growth target, holds back on major stimulus

China pledged its full confidence in achieving this year’s growth target of around 5%, vowing to implement timely and multiple support measures as the country is now in full-fledged trade war with the US. However, no major stimulus was announced immediately, giving the impression that Beijing is not in a rush to roll out large-scale interventions. Authorities appear inclined to first monitor the trade shock’s timing and magnitude before deciding on more aggressive measures.

Zhao Chenxin, deputy head of the National Development and Reform Commission, stressed at a press conference today that China retains “ample policy reserves and plenty of policy space,” and highlighted plans to stabilize employment and strengthen public employment services.

At a Politburo meeting chaired by President Xi Jinping last week, officials called for a “timely reduction” in interest rates and reserve requirement ratios to support the economy. Additional measures to aid struggling businesses, boost consumption among middle- and lower-income groups, and promote further development in technology and artificial intelligence were also emphasized.

As a touch of optimism, official data released over the weekend showed China’s industrial profits returning to growth in the first quarter. Cumulative profits rose 0.8% yoy to CNY 1.5T, reversing a -0.3% decline seen in the first two months.

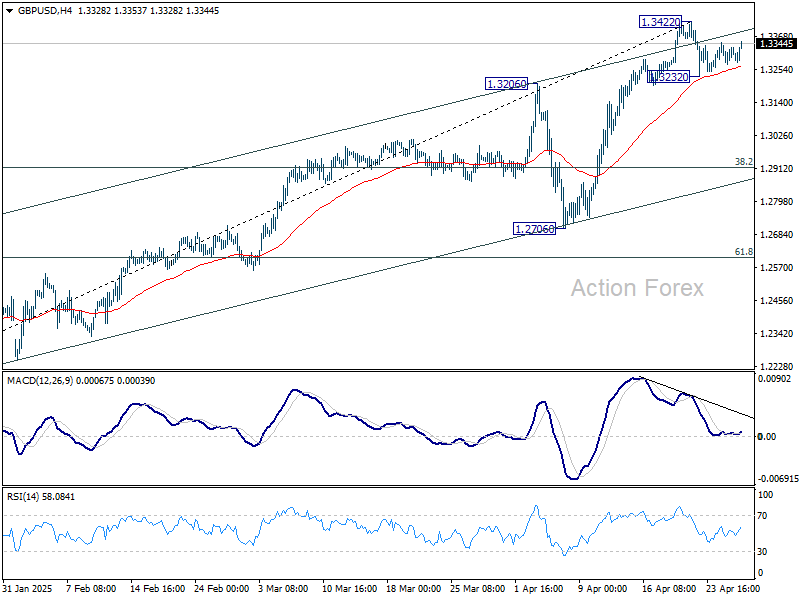

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3268; (P) 1.3318; (R1) 1.3361; More…

Intraday bias in GBP/USD is turned neutral first with today’s recovery. Correction from 1.3422 short term top could still extend, and break of 1.3232 will turn intraday bias back the downside. But in this case, downside should be contained by 38.2% retracement of 1.2099 to 1.3422 at 1.2917. On the upside, firm break of 1.3422/33 resistance zone will resume larger up trend.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could either be resuming the up trend, or the second leg of a consolidation pattern. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.