Yen Slides as BoJ Slashes Growth Outlook; Investor Resilience Faces ISM Test – Action Forex

Yen weakened broadly today following the BoJ’s decision to leave interest rates unchanged, while significantly downgrading its growth projections for the current fiscal year. Inflation outlook was also softened, with risks of undershooting the 2% target increased, albeit slightly.

This backdrop suggests that while BoJ remains on a slow tightening path, policymakers may take a more cautious approach in the near term. The prospect of a rate hike in June now appears less likely unless global trade negotiations between the US and its partners make meaningful progress.

Elsewhere, Wall Street showed surprising resilience overnight. After initially tumbling on the back of an unexpected Q1 contraction in US GDP, DOW and S&P 500 managed to close in positive territory, while NASDAQ was little changed. Fed rate expectations were also little changed, with markets still pricing in a 97% chance of a hold in May and a 66% chance of a rate cut in June.

Investor sentiment, while shaken, has not broken—at least not yet. Attention now shifts to the upcoming ISM manufacturing survey today and tomorrow’s US non-farm payroll report.

In the currency markets, Yen is the day’s weakest performer so far, weighed down by BoJ’s dovish lean. Sterling and Euro are also under pressure. On the other side, Kiwi leads gains, followed by Loonie and Aussie. Dollar and Swiss Franc are trading in the middle.

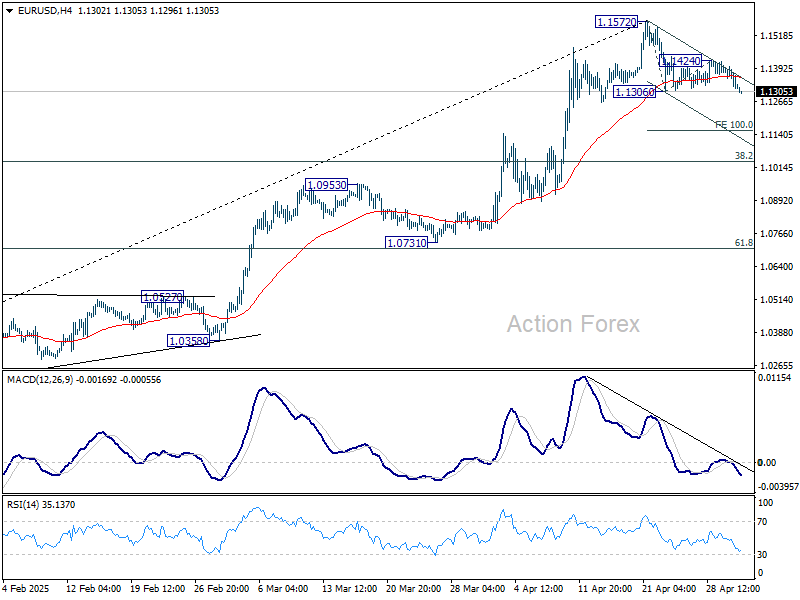

Technically, EUR/USD’s correction from 1.1572 short term top is resuming through 1.1306 support. Deeper fall is now in favor to 100% projection of 1.1572 to 1.1306 from 1.1424 at 1.1158. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039 to complete the pullback.

In Asia, at the time of writing, Nikkei is up 0.93%. Japan 10-year JGB yield is down -0.038 at 1.277. Hong Kong, China and Singapore are on holiday. Overnight, DOW rose 0.35%. S&P 500 rose 0.15%. NASDAQ fell -0.09%. 10-year yield rose 0.004 to 4.177.

Looking ahead, Swiss retail sales and UK PMI maufacturing final will be released in European sesison. Later in the day, US will publish ISM manufacturing and jobless claims.

BoJ holds rates, slashes growth outlook on trade headwinds

BoJ kept its benchmark interest rate unchanged at 0.50% today, by unanimous vote, in line with expectations. However, it struck a cautious tone on the economic outlook by sharply cutting its growth forecasts.

The central bank now projects Japan’s real GDP to grow just 0.5% in fiscal 2025, down from the 1.1% forecast in January, and 0.7% in fiscal 2026 (downgraded from 1.0%). Growth is expected to recover to 1.0% in fiscal 2027, assuming stabilization in global conditions.

In its statement, BoJ acknowledged that “Japan’s economic growth is likely to moderate” as global trade and policy uncertainty weigh on external demand and corporate profitability. Still, the bank expects activity to reaccelerate once overseas economies resume “a moderate growth path.”

On inflation, BoJ maintained that price pressures are broadly on course toward the 2% target, but revised its CPI core forecast down from 2.4% to 2.2% for fiscal 2025, and from 2.0% to 1.7% for fiscal 2026.

BoJ raised its projection for the core-core CPI from 2.1% to 2.3% for fiscal 2025, reflecting persistent domestic inflation pressures. However, this is followed by a downgrade from 2.1% to 1.8% in 2026 before stabilizing at 2.0% in 2027.

Japan’s PMI manufacturing finalized at 48.7, slump persists amid trade uncertainty

Japan’s manufacturing sector remained in contractionary territory in April, with the final PMI reading at 48.7, up slightly from March’s 48.4. While the deterioration in business conditions marked the tenth consecutive month of decline, it remained modest.

However, underlying components revealed more concerning trends, with sharper drops in new orders and exports, highlighting persistent demand-side weakness.

According to S&P Global, firms responded by scaling back purchasing and adjusting inventories, while overall sentiment worsened.

Business confidence around future output fell to its lowest since mid-2020, as companies expressed caution amid ongoing global trade tensions and muted demand. Without a significant turnaround in both domestic and external demand, “firms are likely to struggle to see a recovery in conditions”.

BoC minutes: Dual uncertainties cloud policy path

BoC’s summary of deliberations from its April meeting revealed a divided Governing Council, as members weighed the case for another rate cut against the need for more clarity.

While some policymakers pushed for an immediate cut, citing a weakening domestic economy and subdued near-term inflation, others argued in favor of holding steady at 2.75% to better assess the evolving trade environment, especially with US tariffs in flux.

All members acknowledged the unusually high level of uncertainty. They agreed to be “less forward-looking than usual,” signaling a preference for data-dependence over proactive policy signaling.

The Council framed the current risks in two layers: the unpredictable path of U.S. trade policy, and the unknown economic impact of tariffs—including potential fiscal responses to soften the blow.

With no clear resolution on either front, the BoC leaned toward caution, holding policy steady at 2.75% while signaling a readiness to adjust as needed.

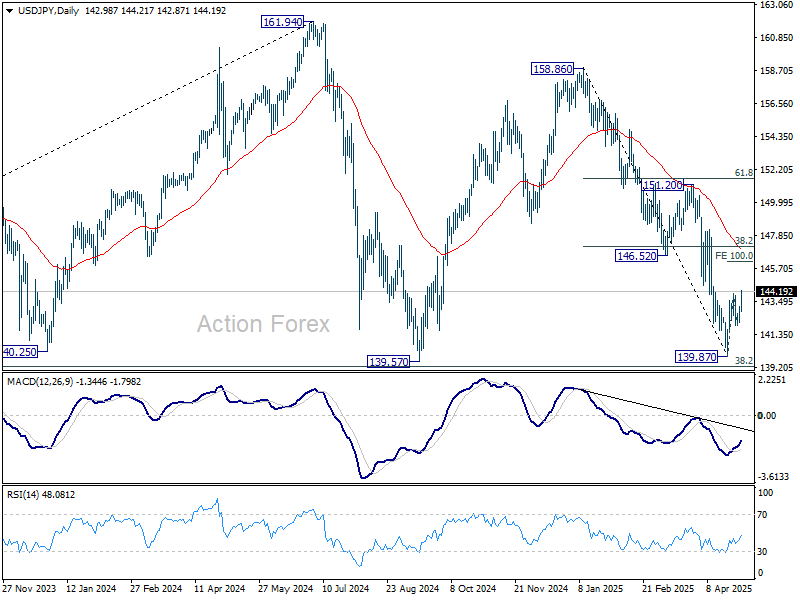

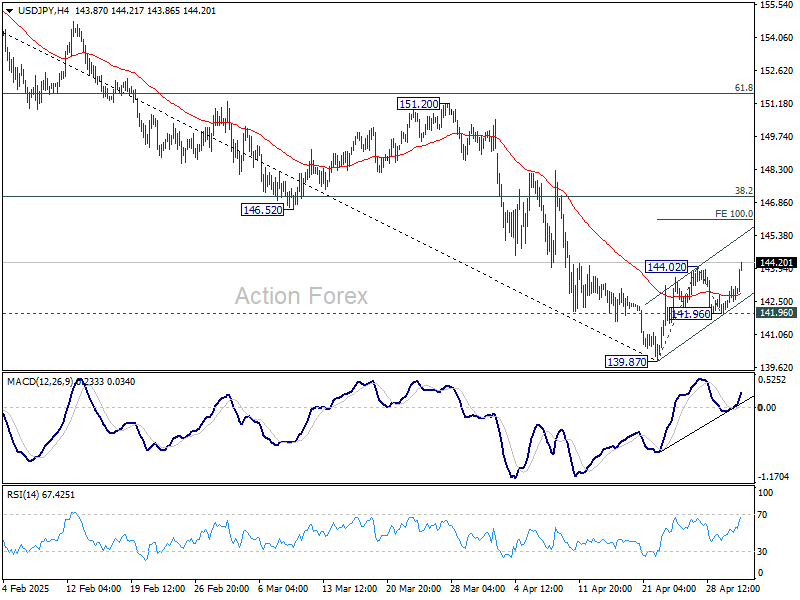

USD/JPY Daily Outlook

Daily Pivots: (S1) 142.42; (P) 142.81; (R1) 143.45; More…

USD/JPY’s rebound from 139.87 short term bottom resumed by breaking through 144.02 today. Intraday bias is back on the upside for 100% projection of 139.87 to 144.02 from 141.96 at 146.11. But still, near term outlook will stay bearish as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds. On the downside, firm break of 141.96 will argue that the rebound has completed as a corrective move. Retest of 139.87 should then be seen next in this case.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.