Dollar Rally Stalls, Market Cools, Trade Optimism Tempered by Reality – Action Forex

Global markets showed signs of fatigue overnight as trade optimism gave way to a more cautious tone. In the US, the S&P 500 eked out another gain, turning positive for the year, while DOW lagged and closed modestly lower. The divergence reflects a market still digesting the implications of recent trade developments. In Asia, stock markets also lacked direction, with investors reluctant to chase risk without clearer signs of progress on the trade front.

Despite the positive headlines, investors are coming to terms with the reality that any new trade deal with China is unlikely to resemble a full rollback to pre-conflict conditions. Even if an agreement is reached, it will likely involve layered provisions and protracted enforcement timelines, making the short-term benefits less impactful. Meanwhile, trade discussions with the EU remain stalled, and Brussels is preparing countermeasures should negotiations not advance in the near future. The fragmented state of trade diplomacy is leaving markets in a holding pattern, particularly as geopolitical and political uncertainties remain elevated.

That said, there is cautious hope that more preliminary deals could emerge soon. Market chatter suggests Switzerland, India, and Japan might be next in line for early-stage agreements. Though, like the recent UK deal, these are likely to be agreements in principle rather than fully ratified pacts, requiring extended negotiations before they take effect.

Adding to the anticipation, US National Economic Council Director Kevin Hassett said President Donald Trump is expected to announce a new trade deal upon returning from his Middle East trip. According to Hassett, around 25 negotiations are currently underway, with at least one nearing final confirmation.

Dollar’s rally also lost much momentum, despite extended rise in 10-year yield. Technically, Dollar’s bounce earlier in the week look more like part of a corrective rise, then a genuine bullish reversal. As for 10-year yield, rise from 3.886 might be ready to resume with corrective pullback from 4.592 completed at 4.124. Further rally is now in favor to retest 4.592 first. Firm break there will confirm this bullish case and target 100% projection of 3.86 to 4.592 from 4.124 at 4.830.

As for currency performance this week, Aussie is now leading the pack, followed by Kiwi, and then Loonie. Yen remains the weakest, trailed by Swiss Franc and Euro. Dollar and British Pound are trading in the middle of the pack.

In Asia, at the time of writing, Nikkei is down -0.33%. Hong Kong HSI is up 1.42%. China Shanghai SSE is up 0.35%. Singapore Strait Times is down -0.22%. Japan 10-year JGB yield is up 0.008 at 1.457.

Overnight, DOW fell -0.64%. S&P 500 rose 0.72%. NASDAQ rose 1.61%. 10-year yield jumped 0.042 to 4.499.

Japan’s PPI rises 4% yoy in April, record high for 8th straight month

Japan’s PPI rose 4.0% year-on-year in April, easing slightly from 4.3% yoy in March and matching market expectations. Despite the modest slowdown, the index climbed to a fresh record high of 126.3, marking the eighth consecutive month of new highs, highlighting persistent cost pressures at the wholesale level.

However, the data also showed little immediate impact from the sweeping US tariffs announced in early April, thanks in part to the 90-day suspension.

Japan’s Yen-based import price index fell sharply by -7.2% yoy in April, following a -2.4% yoy decline in March. The drop suggests that Yen’s appreciation during the market turmoil have helped shield Japanese importers from some of the price shocks, at least for now.

Australian wage growth accelerates to 3.4% yoy in Q1, led by public sector

Australia’s Wage Price Index rose by 0.9% qoq in Q1, slightly above market expectations of 0.8% qoq. Public sector saw a stronger 1.0% qoq gain, outpacing the 0.9% qoq rise in private sector.

On an annual basis, wages grew by 3.4%, up from 3.2% in the previous quarter, marking the first uptick in annual wage growth since mid-2024.

The uptick in annual wage growth was driven primarily by the public sector, which saw a notable increase to 3.6% yoy from 2.9% yoy in Q4. Private sector wage growth was steady at 3.3% yoy.

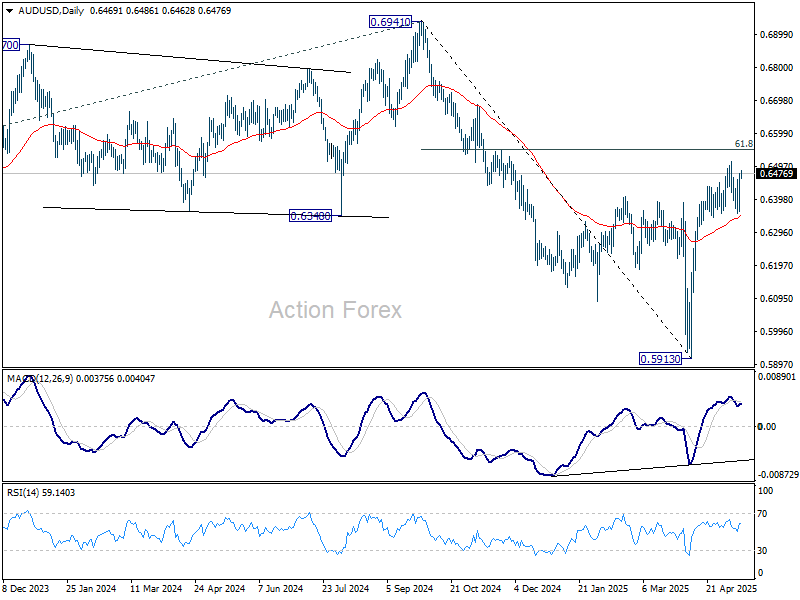

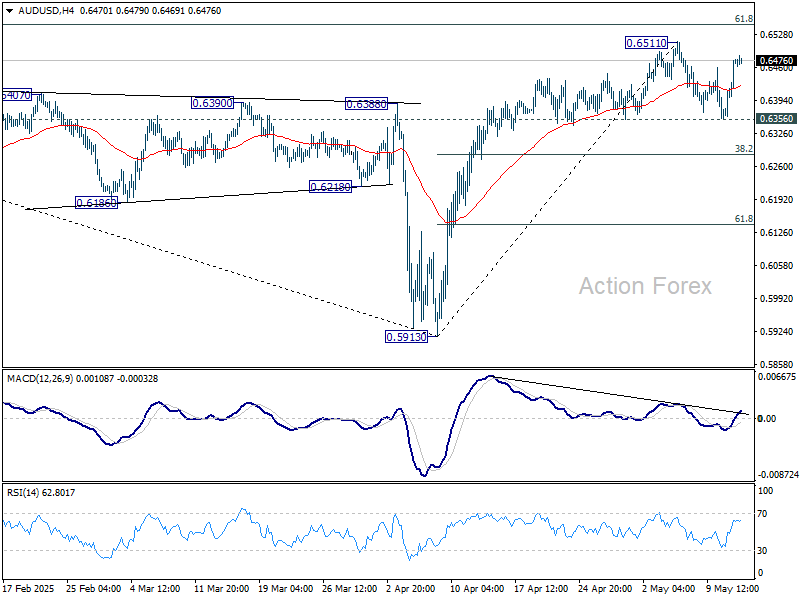

AUD/USD Daily Report

Daily Pivots: (S1) 0.6395; (P) 0.6437; (R1) 0.6513; More...

AUD/USD is staying in range below 0.6511 and intraday bias remains neutral. On the upside, firm break of 0.6511 will resume the rally from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, break of 0.6356 support should confirm short term topping. Intraday bias will be turned back to the downside for 38.2% retracement of 0.5913 to 0.6511 at 0.6283.

In the bigger picture, as long as 55 W EMA (now at 0.6441) holds, down trend from 0.8006 (2021 high) should resume later to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.