Markets Tread Water as Traders Shrug Off US PPI and UK GDP Surprises – Action Forex

Global financial markets are trading in tight ranges today, with little conviction seen across major asset classes. U.S. futures are pointing to a mildly weaker open. Despite a surprise decline in US producer prices in April, suggesting a possible easing of inflation pressures, there was little follow-through in market reaction. Earlier today, stronger-than-expected UK Q1 GDP data also offered limited support to the Pound. Overall sentiment remains contained as traders await further clarity on the trade front.

Much of the current hesitation in markets can be attributed to persisting trade uncertainty. The EU Foreign Affairs Council is holding a key meeting today in Brussels to discuss trade relations with the US and broader economic security. Ahead of the meeting, European trade ministers expressed dissatisfaction with the limited UK-US trade agreement announced last week, which retains a 10% tariff on British exports. EU officials signaled that such a deal would not suffice to deter retaliatory measures.

European Trade Commissioner Maros Sefcovic confirmed a recent conversation with U.S. Commerce Secretary Howard Lutnick and noted that both sides have agreed to step up engagement. Additional meetings are anticipated in Brussels or during upcoming OECD sessions. However, the complexity of negotiations and diverging expectations between the EU and US continue to cast doubt on a swift resolution.

Elsewhere, trade talks between the US and India also show signs of friction. US President Donald Trump claimed that India had offered a trade deal with “no tariffs” on American goods. However, India’s foreign minister Subrahmanyam Jaishankar quickly pushed back, saying that talks remain ongoing and nothing has been finalized. It’s believed that India would demand strict reciprocity on tariffs, while it’s unlikely to concede easily in politically sensitive sectors such as agriculture, where protectionist pressures remain high.

In the currency markets, Aussie is leading gains for the week, followed by Dollar and then Sterling. On the weaker side, the Swiss Franc is the laggard, with Kiwi and Euro also underperforming. Yen and Canadian Dollar are holding middle positions.

In Europe, at the time of writing, FTSE is up 0.34%. DAX is up 0.10%. CAC is down -0.19%. UK 10-year yield is down -0.042 at 4.674. Germany 10-year yield is down -0.061 at 2.64. Earlier in Asia, Nikkei fell -0.98%. Hong Kong HSI fell -0.79%. China Shanghai SSE fell -0.68%. Singapore Strait Times rose 0.54%. Japan 10-year JGB yield rose 0.022 to 1.479.

US retail sales rises 0.1% mom in Apr, ex-auto sales up 0.1% mom

US retail sales rose 0.1% mom to USD 724.1B in April, matched expectations. Ex-auto sales rose 0.1% mom to USD 582.5B, below expectation of 0.3% mom. Ex-gasoline sales rose 0.1% mom to USD 673.1B. Ex-auto & gasoline sales rose 02% mom to USD 531.5B.

Total sales for the February through April period were up 4.8% from the same period a year ago.

US PPI at -0.5% mom, 2.4% yoy in April, below expectations

US PPI fell -0.5% mom in April, below expectation of 0.2% mom. PPI services fell -0.7% mom while PPI goods was unchanged. PPI less foods, energy and trade services ticked down by -0.1% mom, the first decline since April 2020.

For the 12 months, PPI slowed from 2.7% yoy to 2.4% yoy, below expectation of 2.5% yoy. PPI less foods, energy and trade services rose 2.9% yoy.

US initial jobless claims unchanged at 229k

US initial jobless claims was unchanged at 229k in the week ending May 10, slightly below expectation of 230k. Four-week moving average of initial claims rose 3k to 230.5k.

Continuing claims rose 9k to 1881k in the week ending May 3. Four-week moving average of continuing claims rose 1k to 1874k.

Eurozone industrial output surges 2.6% mom in March, led by capital goods

Eurozone industrial production jumped 2.6% mom in March, significantly outperforming expectations of 1.7% mom. The surge was driven by strong gains across key categories, including capital goods (+3.2%), durable consumer goods (+3.1%), and non-durable consumer goods (+2.3%). Intermediate goods also posted a modest 0.6% rise, while energy output dipped by -0.5%.

Across the broader EU, industrial production rose by 1.9% mom. Ireland led the gains with a remarkable 14.6% surge, followed by Malta (+4.4%) and Finland (+3.5%). However, there were notable declines in Luxembourg (-6.3%), Denmark, Greece (both -4.6%), and Portugal (-4.0%).

UK economy beats expectations with 0.7% qoq growth in Q1, 0.2% mom in March

The UK economy expanded by 0.7% qoq in Q1, slightly ahead of expectations at 0.6% qoq. Growth was led by a 0.7% qoq rise in the services sector and a robust 1.1% qoq increase in production output, while construction activity was flat. Importantly, real GDP per head also rose by 0.5% qoq, ending two consecutive quarters of contraction.

On the expenditure side, growth was underpinned by a 2.9% qoq rise in gross fixed capital formation, signaling strong business investment. Household consumption also edged up by 0.2% qoq, while net trade contributed positively as exports rose by 3.5% qoq and imports by 2.1% qoq.

Monthly data for March further supported the upbeat quarterly reading, with GDP rising by 0.2% mom, exceeding expectations of flat growth. Services output was the standout, rising 0.4% mom and contributing the most to overall GDP expansion. Meanwhile, construction rose by 0.5% mom, offsetting a -0.7% mom decline in production output.

Australia jobs surge 89k in April, unemployment rate unchanged at 4.1%

Australia’s labor market delivered a strong upside surprise in April, with employment rising by 89k, sharply above expectations of 20.9k. Full-time jobs accounted for 59.5k of the gain, while part-time employment rose by 29.5k.

Unemployment rate held steady at 4.1%, in line with forecasts, as the surge in employment was matched by a jump in labor force participation from 66.8% to 67.1%.

Despite the headline strength, hours worked were largely unchanged on the month. Nonetheless, the employment-to-population ratio rose by 0.3 percentage points to 64.4%, just shy of the record high reached in January.

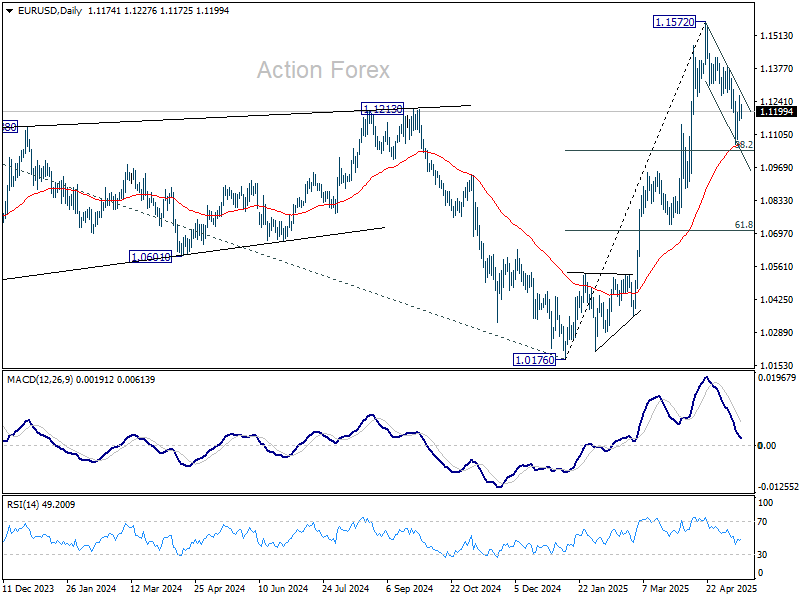

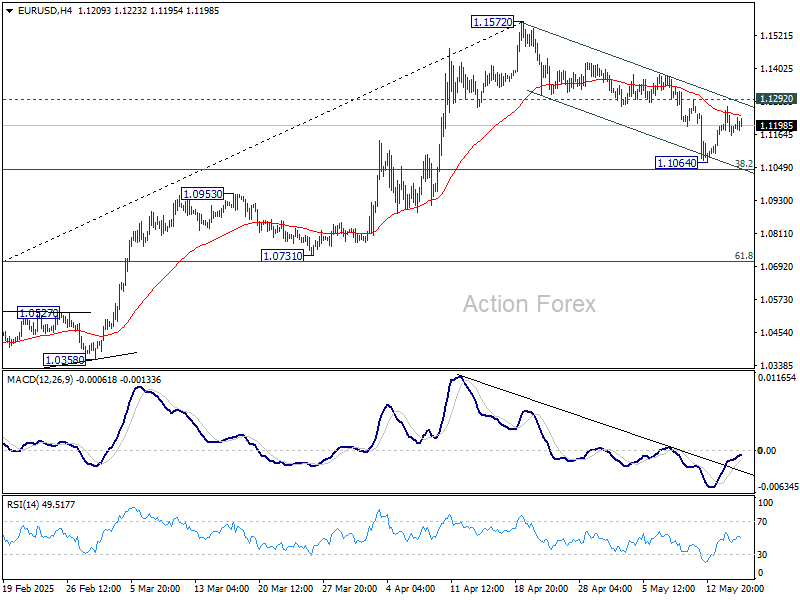

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1136; (P) 1.1201; (R1) 1.1238; More…

Range trading continues in EUR/USD and intraday bias stays neutral. On the upside, break of 1.1292 resistance will argue that correction from 1.1572 has completed after defending 38.2% retracement of 1.0176 to 1.1572 at 1.1039. Intraday bias will be back on the upside for retesting 1.1572. However, sustained break of 1.1039 will dampen this view and target 61.8% retracement at 1.0709 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0789) holds.