Moody’s Downgrade Disrupts Calm from Tariff Truce, Dollar Faces New Test – Action Forex

Just as markets were finding their footing following a series of positive trade developments, Moody’s delivered a late-week shock by downgrading the US sovereign credit rating from Aaa to Aa1. The move overshadowed the optimism sparked by the US-China tariff truce and the broader de-escalation of trade tensions.

The trade outlook appears less volatile in the near term, with more agreements possibly in the pipeline. Markets may enjoy a reprieve from tariff headlines until early July for non-China partners, and until mid-August for China.

However, that stability could be abruptly shaken by Moody’s downgrade. The timing of the downgrade coincides with fragile improvements in sentiment, raises the risk of renewed selling in both Treasuries and Dollar.

In the currency markets, performance was mixed last week, a hallmark of broader consolidation. Dollar finished as the strongest currency but notably failed to build on its early-week strength. Aussie followed as the second-best performer, buoyed by strong domestic job data and risk appetite, while Sterling also held firm with support from strong UK GDP. However, gains were limited overall. On the weaker side, Euro posted the poorest performance, followed by Swiss Franc and Kiwi. Yen and Loonie ended the week in the middle.

Wall Street Surges on Trade Truce, Even Though Soaring Inflation Expectations Reinforce Fed Patience

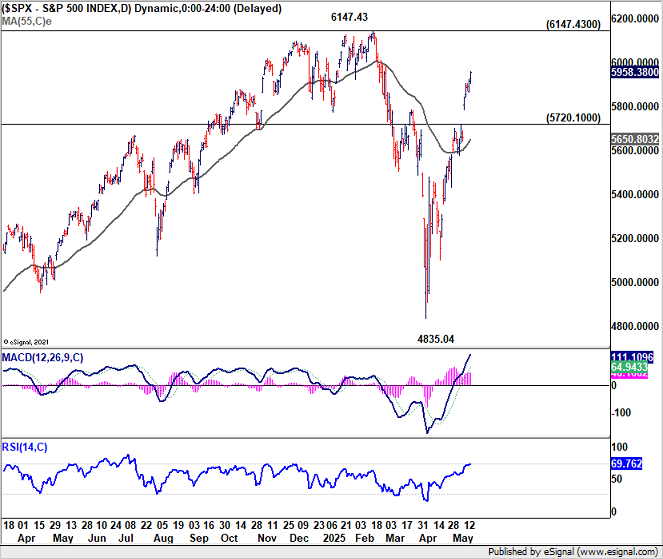

US equity markets wrapped up the week with strong gains, driven by renewed optimism over global trade and investor resilience, despite worrying economic signals. S&P 500 surged 5.3%, DOW added 3.4%, and NASDAQ Composite outperformed with a 7.2% jump. The rally was initially sparked by the surprising outcome of the US-China trade meeting. Both sides agreed to a 90-day truce and rolled back a significant portion of the tariffs, though not fully returning to pre-conflict levels.

Investors looked past several downside risks and pushed stock prices higher, even as economic data pointed to potential trouble ahead. Markets absorbed weak consumer sentiment and sharply rising inflation expectations without flinching. This reflects a broader hope that trade normalization will continue to offset macro headwinds, at least in the short term.

The University of Michigan’s preliminary consumer sentiment report for May, released Friday, highlighted growing public anxiety. The headline index dropped to 50.8, its second-lowest reading on record. Year-ahead inflation expectations surged from 6.5% to 7.3%, the highest since 1981.

Importantly, the survey was conducted between April 22 and May 13. That timeframe includes the period after US President Donald Trump announced that reciprocal tariffs on all trading partners other than China would be scaled back to a 10% baseline. It also includes responses collected a day after the US-China truce was declared.

In that context, the persistent collapse in sentiment and worsening inflation outlook suggest that consumers remain highly skeptical about the economic direction. Even the rollback of some tariffs was not enough to lift the mood or tame concerns about rising prices. Attention will now be on the final May release due May 30, to see if sentiment and expectations shift more positively as the trade truce sinks in.

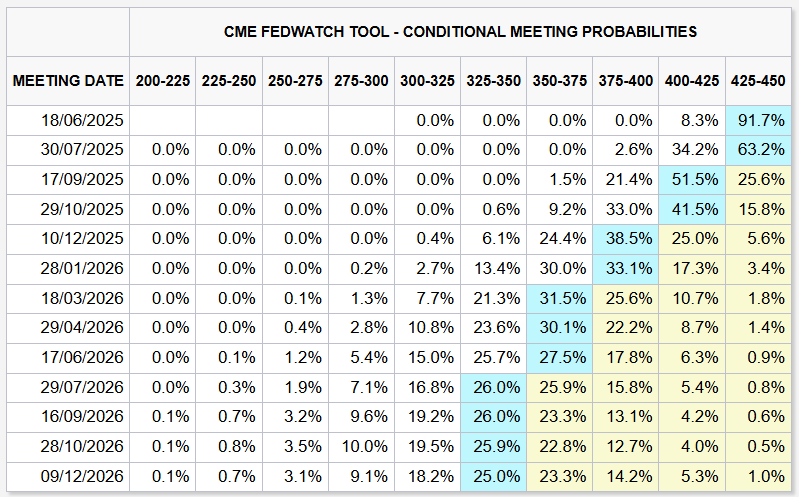

For Fed, the data likely reinforce a cautious stance, for holding back from another rate cut for longer. Fed funds futures now reflect just a 36% chance of a 25bps rate cut in July. Expectations rise to 75% for a September cut, followed by around 70% odds of another in December. That suggests markets believe only two rate cuts are likely this year, if any.

Technically, S&P 500 gapped higher at the start of the week and extended its rally from 4835.04 low. The current rise is still viewed as the second leg in the medium-term corrective pattern from the 6147.43 high. Momentum should start to fade above 6000 psychological level. A break below 5720.10 gap support would indicate short-term topping. Sustained trading below 55 Day EMA (now at 5650.80) would suggest that the third leg of the correction has already begun.

Moody’s Downgrade Casts Shadow Over Dollar and Treasuries

Despite a strong weekly finish for Wall Street and Dollar, sentiment faces a fresh challenge after Moody’s downgraded the US sovereign credit rating on Friday. The move, announced after markets closed, cut the rating by one notch to Aa1 from Aaa—marking a rare loss of top-tier status. While the immediate market reaction was muted due to timing, the downgrade could cast a shadow over financial markets in the coming week, with pressure potentially building on both Dollar and US Treasuries.

Notably, Dollar ended as the top-performing major currency last week, but it did so without conviction. After Monday’s initial surge, momentum faded quickly. By midweek, the greenback began to stall, showing little follow-through despite stronger inflation expectations. That suggests underlying demand may be fragile.

Moody’s cited deteriorating fiscal outlook as the key reason for the downgrade, pointing to “successive US administrations and Congress” that have failed to reverse the trend of widening deficits and rising debt servicing costs. The agency also expressed skepticism that meaningful fiscal reforms are on the horizon, making clear that the downgrade reflects more than just short-term political risks. The downgrade reflects not only mounting fiscal stress, but also the political impasse that continues to hinder structural reforms.

This backdrop is especially important given how markets reacted in early April, when sweeping reciprocal tariffs imposed by the US triggered a rally in Treasury yields and broad weakening of Dollar. That episode suggested investors may be reassessing traditional assumptions about the US’s role as the ultimate safe asset provider. A similar dynamic could resurface if the Moody’s downgrade gains traction with bondholders or sparks broader credit rating scrutiny.

Technically, 10-year yield’s strong rise last week suggests that near term correction from 1.4592 has already completed at 4.124. Rise from 3.886 might be ready to resume. Further rally is now in favor as long as 55 D EMA (now at 4.3437) holds. Firm break of 4.592 would target 100% projection of 3.886 to 4.592 from 4.124 at 4.830 next.

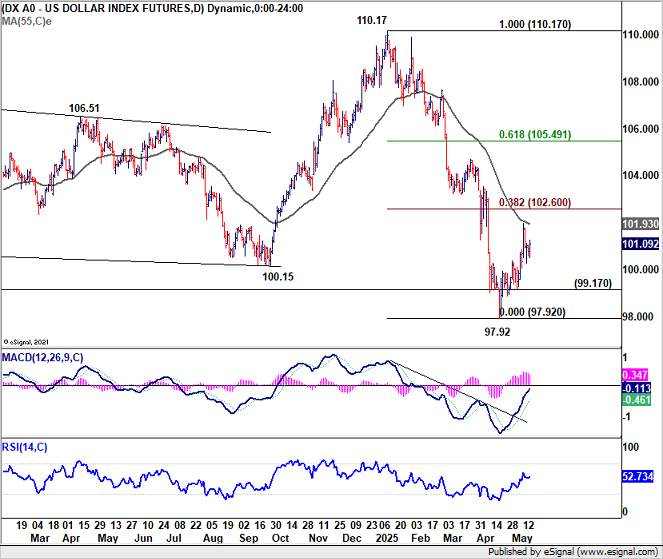

Dollar Index’s corrective recovery from 97.92 continued last week, but started to struggle ahead of 55 D EMA (now at 101.93). While another rise cannot be ruled out, upside should be limited by 38.2% retracement of 110.17 to 97.92 at 102.60. On the downside, break of 99.17 support will argue that larger down trend is ready to resume through 97.92 low.

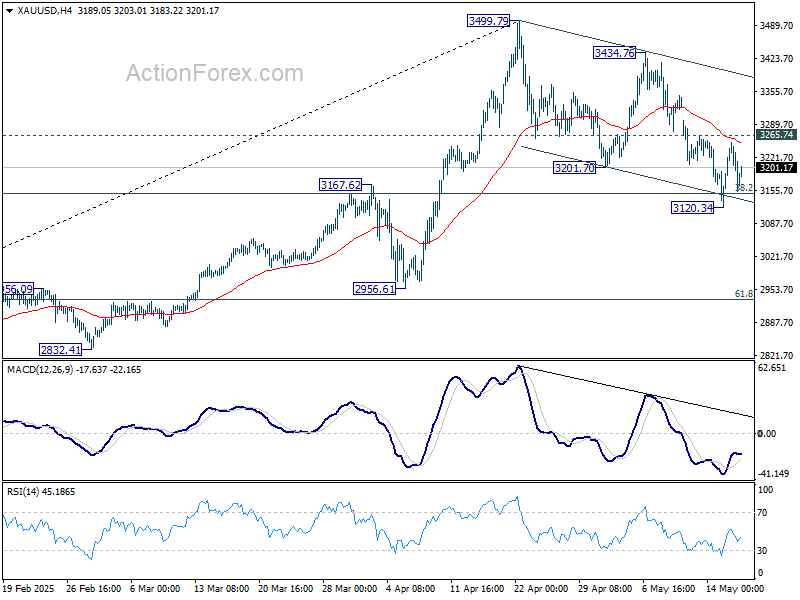

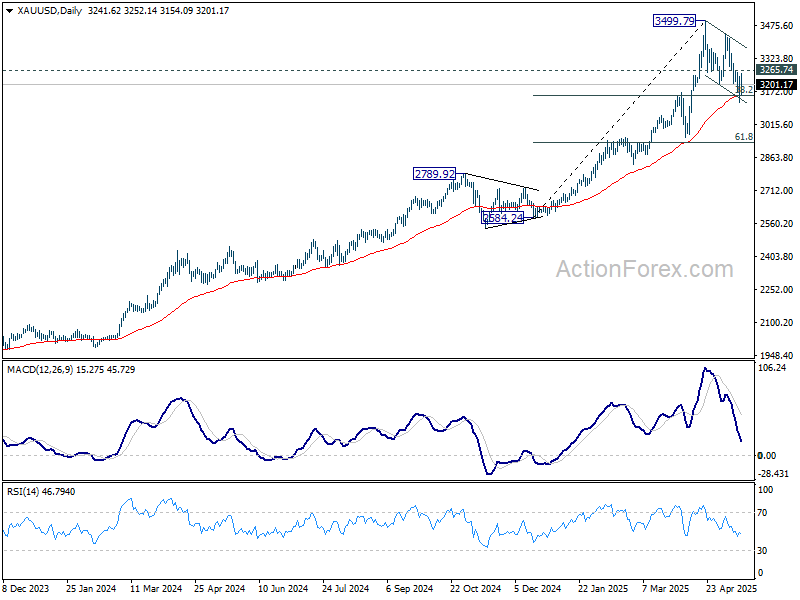

One asset that could benefit from renewed stress on the Dollar and Treasuries is Gold. Technically, Gold is now at an ideal level to complete the corrective pullback from 3499.79 high. Current levels include 55 D EMA (now at 3152.88) and 38.2% retracement of 2584.24 to 3499.79 at 3150.04. On the upside, firm break of 3262.74 resistance should bring stronger rally back to 3434.76/3499.79 resistance zone.

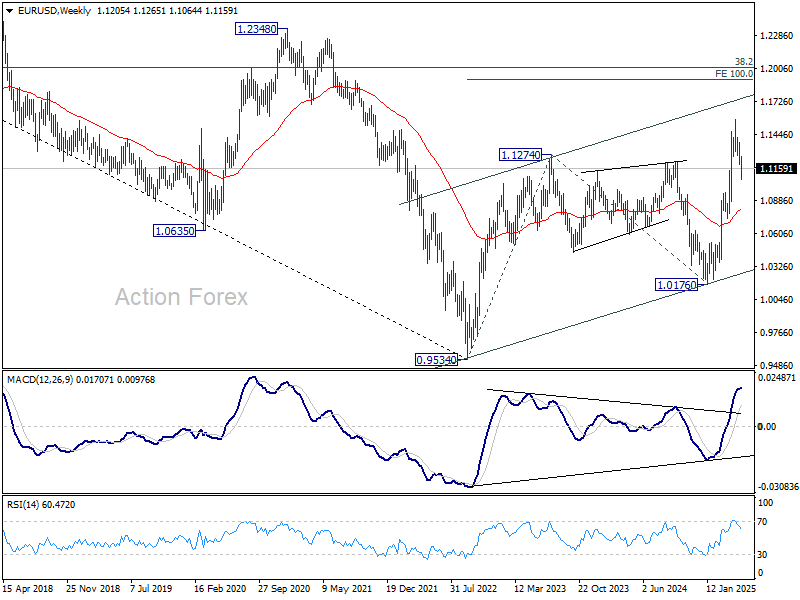

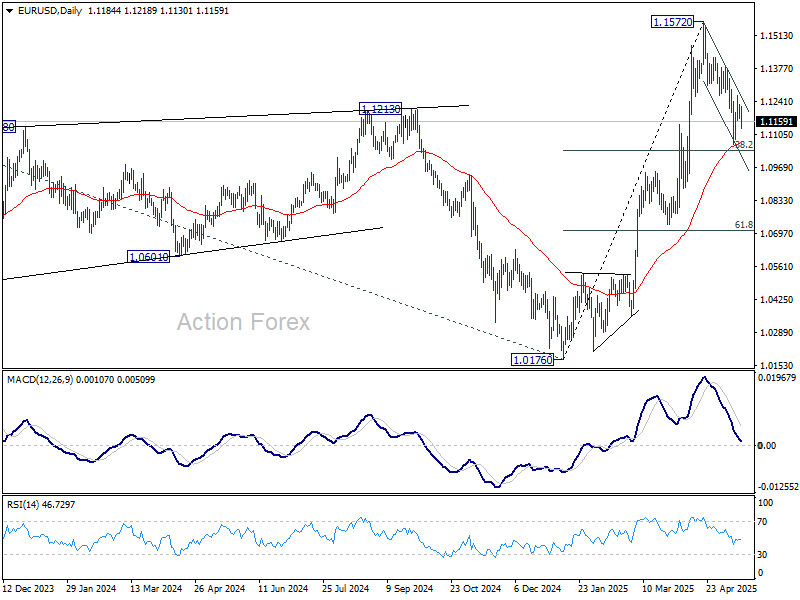

EUR/USD Weekly Outlook

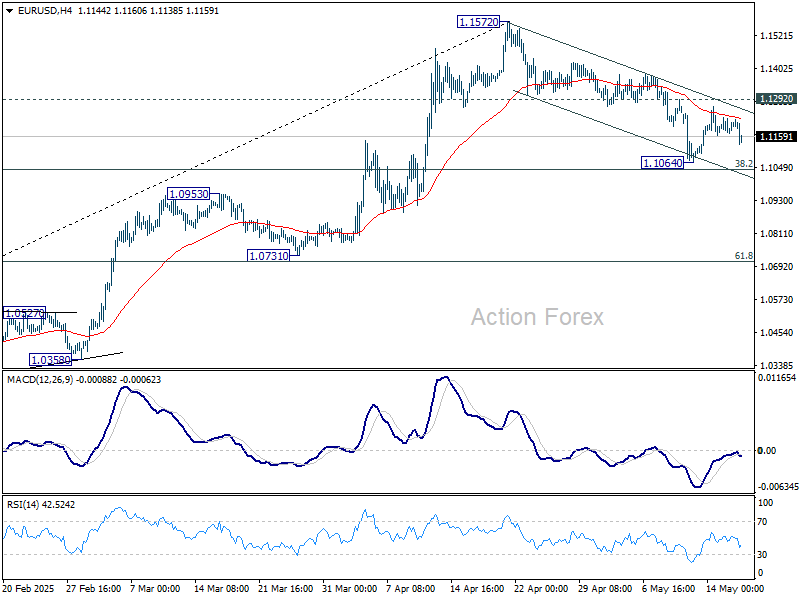

EUR/USD dived further to 1.1064 last week but recovered ahead of 38.2% retracement of 1.0176 to 1.1572 at 1.1039. Initial bias remains neutral this week first. Strong support is still expected from 1.1039 to complete the correction from 1.1572. On the upside, above 1.1292 will bring stronger rise back to retest 1.1572. However, sustained break of 1.1039 will dampen this view and target 61.8% retracement at 1.0709 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0818) holds.

In the long term picture, the case of long term bullish reversal is building up. Sustained break of falling channel resistance (now at around 1.1300) will argue that the down trend from 1.6039 (2008 high) has completed at 0.9534. A medium term up trend should then follow even as a corrective move. Next target is 38.2% retracement of 1.6039 to 0.9534 at 1.2019.