Dollar Drops on CPI Miss; Trade Optimism Offers Limited Support – Action Forex

Dollar fell broadly following weaker-than-expected US inflation report for May, reinforcing the narrative that consumer prices have not yet felt the full brunt of tariff pressures. The data offered some relief that the feared pass-through from tariffs to end consumers hasn’t materialized, at least not yet.

However, it wasn’t enough to shift expectations for the June and July Fed meetings, where markets still overwhelmingly anticipate the central bank to hold steady. What did shift slightly was the probability of a September rate cut. According to fed funds futures, the odds of a cut in Q3 have now climbed above 55%. Nonetheless, the Fed is unlikely to act preemptively without more confirmation.

On trade, President Trump declared this week’s talks with China a success, albeit with no rollback of existing tariffs. While the 55% tariff rate remains in place, Trump noted that China has committed to supplying key items such as magnets and rare earths “up front,” with the US reciprocating on non-economic terms like student access.

In the broader FX market, Dollar is now the weakest performer for the week, followed by Sterling and Yen. The Pound remains weighed down by soft UK labor market data. On the other hand, Euro is gaining the upper hand, while commodity Aussie and Kiwi are benefiting from improved risk sentiment. Swiss Franc and Loonie sit in the middle.

In Europe, at the time of writing, FTSE is up 0.22%. DAX is up 0.41%. CAC is up 0.10%. UK 10-year yield is up 0.008 at 4.552. Germany 10-year yield is down -0.006 at 2.521. Earlier in Asia, Nikkei rose 0.55%. Hong Kong HSI rose 0.84%. China Shanghai SSE rose 0.52%. Singapore Strait Times fell -0.37%. Japan 10-year JGB yield fell -0.019 to 1.461.

US CPI ticks up to 2.4%, core unchanged at 2.8%, undershoot expectations

US consumer inflation data for May came in softer than expected, offering some relief to markets concerned about price pressures from tariffs and broader cost pass-throughs.

Headline CPI rose just 0.1% mom, below consensus of 0.2% mom. Core CPI, which excludes food and energy, also surprised to the downside with a 0.1% mom rise against an expected 0.3% mom. The gains in overall prices were primarily driven by shelter (0.3% mom) and food (0.3% mom), while energy posted a -1.0% monthly drop.

On an annual basis, headline CPI rose slightly from 2.3% yoy to 2.4% yoy, still undershooting the forecasted 2.5% yoy. Core CPI held steady at 2.8% yoy, also missing expectations of 2.9% yoy.

ECB’s Lane: Last week’s rate cut aimed at anchoring expectations, avoiding prolonged undershoot

ECB Chief Economist Philip Lane emphasized that last week’s rate cut was a strategic step to ensure inflation remains on track toward the 2% target over the medium term. He argued that, without this move, the “projected negative inflation deviation” over the next 18 months could have risked becoming entrenched.

In a speech today, Lane also stressed the importance of clarity in ECB’s reaction function. By cutting the deposit facility rate to 2.00%, the central bank signaled that “we are determined to make sure that inflation returns to target in the medium term”. This helps “underpin inflation expectations and avoid an unwarranted tightening in financial conditions.”

On the other hand, holding the rate at 2.25% could have sent the wrong signal, Lane warned, potentially triggering a market repricing that would reinforce a “more pronounced and longer-lasting undershoot of the inflation target.”

ECB’s Kazaks: Further fine-tuning cuts likely

Latvian ECB Governing Council member Martins Kazaks signaled openness to further interest rate cuts, suggesting that while ECB has already delivered significant easing, “fine-tuning” adjustments could be needed depending on how the economy evolves.

He noted that current market pricing for one more cut is “not out of the realm of the baseline,” but stressed that any additional moves must be carefully calibrated to keep inflation anchored near the 2% target.

Kazaks warned against complacency, highlighting risks of a persistent inflation undershoot. While not yet leaning toward accommodative territory, he emphasized the importance of vigilance, particularly amid the uncertain impact of global trade tensions. So far, deflationary effects seem to dominate, but the final outcome remains highly uncertain and must be watched closely.

Japan’s CGPI cools to 3.2% in May, but food inflation continue to rise

Japan’s corporate goods price index slowed more than expected in May, easing from 4.1% to 3.2% yoy, versus the anticipated 3.5% yoy. The decline reflects the broader disinflationary trend in upstream prices, aided by the recent rebound in Yen. Yen-based import price index plunged -10.3% yoy, a sharper drop than April’s -7.3% yoy.

Falling raw material costs were evident across sectors, with steel prices down -4.8% yoy, chemicals -3.1% yoy, and non-ferrous metals -2.1% yoy

However, consumer-related categories showed more persistence in inflation. Prices of food and beverages accelerated to 4.2% yoy from April’s 4.0% yoy, suggesting that inflationary stickiness in essential goods remains a challenge despite broader producer-side cooling.

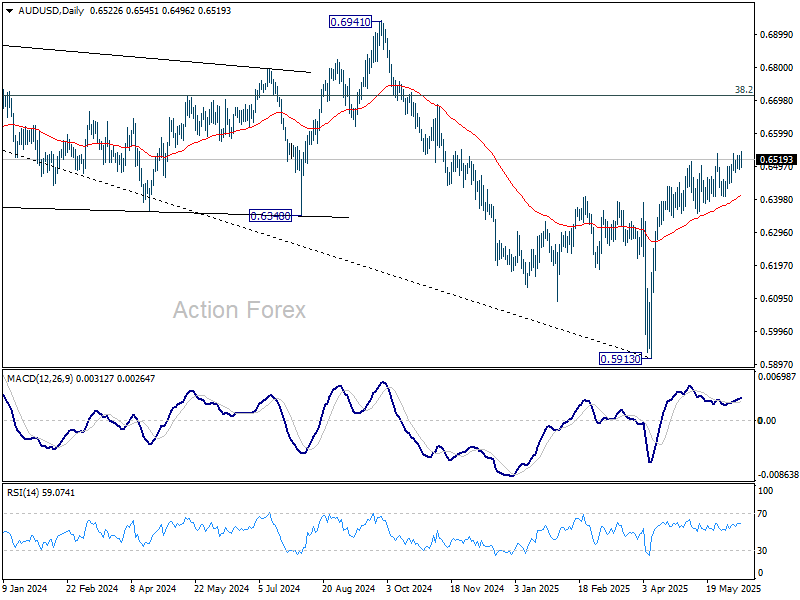

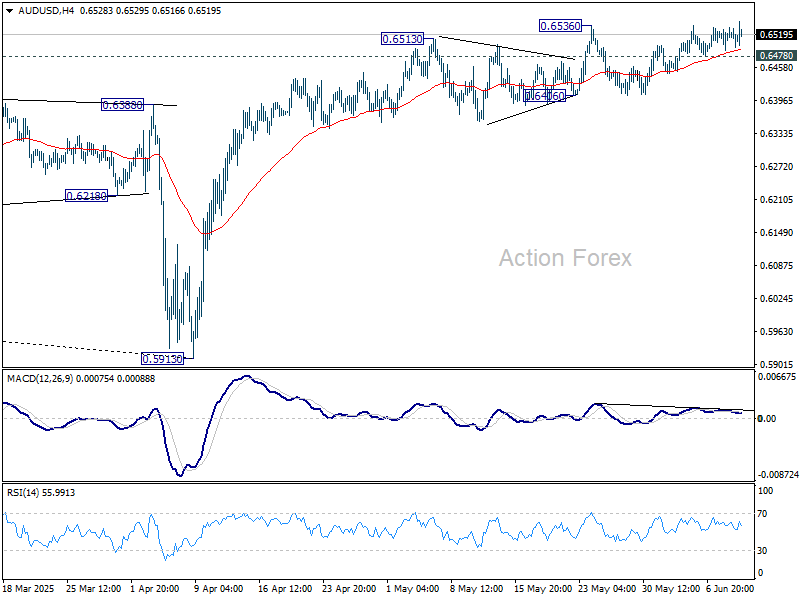

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6497; (P) 0.6515; (R1) 0.6540; More...

Intraday bias in AUD/USD is mildly on the upside with breach of 0.6536 resistance. Rise from 0.5913 could be resuming for 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, considering bearish divergence condition in 4H MACD, break of 0.6478 support will turn bias back to the downside for 55 D EMA (now at 0.6410) and possibly below.

In the bigger picture, AUD/USD is still struggling to sustain above 55 W EMA (now at 0.6443) cleanly, and outlook is mixed. Sustained trading above 55 W EMA will indicate that rise from 0.5913 is at least correcting the down trend from 0.8006 (2021 high), with risk of trend reversal. Further rise should be seen to 38.2% retracement of 0.8006 to 0.5913 at 0.6713. However, rejection by 55 W EMA will revive medium term bearishness for another fall through 0.5913 at a later stage.