Asia Shakes Off Iran Strike Fears, But Oil Market Still on Alert – Action Forex

Asian markets opened the week lower following the US military strikes on Iranian nuclear sites, marking a dramatic escalation in the Middle East. However, losses were limited and short-lived, with major indexes across the region quickly recovering earlier declines. Oil prices also staged a muted response. While WTI spiked on the news, the rally has since moderated.

There was no sign of panic selling (or buying in oil), suggesting that investors view the situation as contained for now. The tempered market reaction could be attributed to a sense of relief that a perceived nuclear threat in the region has been neutralized. Moreover, the conflict is currently isolated, with limited risk of broader regional contagion, at least in the near term.

Still, markets are not complacent. The possibility of Iran retaliating by disrupting oil shipments through the Strait of Hormuz remains a critical risk. The waterway handles roughly 20% of global crude flows, and any closure or threat to shipping lanes could propel WTI well above 100, as some analysts have warned.

In currency markets, nevertheless, safe haven demand is clearly evident. Swiss Franc is the strongest performer of the day so far. Dollar followed as it continues to benefit from Middle East tensions. Euro is also firmer, supported by its perceived reserve status. In contrast, commodity currencies such as the Aussie and Loonie are under pressure, alongside Yen and Pound.

Looking ahead, flash PMIs from the Eurozone, UK, and US will offer a crucial read on business sentiment as tariff and trade war effects ripple through supply chains. Later in the week, attention turns to Fed Chair Jerome Powell’s congressional testimony, though expectations for policy revelations remain low following last week’s FOMC hold and updated forecasts.

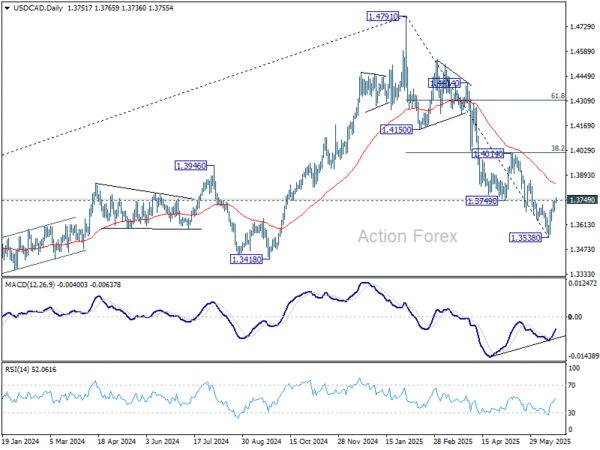

Technically, USD/CAD’s breach of 1.3749 support confirms short term bottoming at 1.3538, on bullish convergence condition in D MACD. Rebound from there is now see as forming a corrective pattern to the five-wave decline from 1.4791. Further rise should be seen in the near term to 55 D EMA (now at 1.3839). But strong resistance should be seen from 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) to limit upside, at least on first attempt.

In Asia, at the time of writing, Nikkei is down -0.18%. Hong Kong HSI is up 0.65%. China Shanghai SSE is up 0.68%. Singapore Strait Times is down 0.26%. Japan 10-year JGB yield is up 0.008 at 1.411.

WTI oil soars on US strikes in Iran; 80 now the line between calm and 100+ chaos

WTI crude surged at the start of the week as geopolitical tensions flared after US airstrikes hit Iranian nuclear targets over the weekend. The move marks a dramatic escalation in the long-simmering conflict between Iran and Israel, now drawing in direct US involvement. Investors are now awaiting Tehran’s next move after Iranian officials said “all options” remain on the table in response.

Attention is now centered on the Strait of Hormuz, a strategic waterway through which one-fifth of the world’s oil flows. Iranian lawmakers have approved a non-binding motion to shut down the strait, though the final decision lies with the National Security Council. Any disruption to shipments through Hormuz would have a profound impact on global supply chains and energy prices.

Technically, WTI crude’s surge from the 55.20 low is now approaching a key resistance at 81.01. Barring a broader escalation, the rally could stall here, especially with overbought momentum indicators flashing caution. A break below 73.69 would be an early sign of stabilization and may trigger profit-taking correction.

But if the conflict deepens and prices break decisively above 81.01, the rally could accelerate toward through 38.2% retracement of 131.82 (2022 high) to 55.20 at 84.46. Sustained break above 84.46 would mark a significant reversal of the long-term downtrend from the 2022 high and open the path to 95.50 or even to 61.8% retracement at 102.55.

With tensions high and the market highly headline-sensitive, holding below 80 will be key to preventing a return to 100+ oil—and renewed inflationary concerns worldwide.

Japan PMI composite rises to 51.4, but trade uncertainty weighs on demand

Japan’s private sector showed a modest rebound in June, with PMI Composite rising from 50.2 to 51.4, the highest reading since February. The pickup was led by stronger services sector, which rose from 51.0 to 51.5. PMI Manufacturing returned to expansion territory at 50.4, up from 49.4.

Annabel Fiddes of S&P Global noted that business activity gained momentum into quarter-end, but demand conditions remained fragile. New business rose only slightly, while foreign demand for manufactured goods weakened further. Firms cited ongoing concerns over US tariffs and global trade uncertainty, which continued to weigh on client orders and export sales.

Still, there were signs of easing cost pressures, with input prices rising at the slowest pace in 15 months. Employment also improved, with overall job creation accelerating to the fastest rate in nearly a year.

Australia PMIs improve modestly, support case for further RBA cuts

Australia’s private sector showed modest improvement in June, with the S&P Global PMI Composite rising from 50.5 to 51.2. PMI Services climbed from 50.6 to 51.3, while PMI manufacturing held steady at 51.0.

According to S&P Global’s Jingyi Pan, forward-looking indicators present a mixed picture. While output expectations remain positive, divergences between sectors were notable. New orders and future output softened more clearly in manufacturing, while services continued to gain traction. Weak external demand remains a concern, with export orders seeing their sharpest drop in nearly a year.

Combined with signs of easing inflation and slower employment growth, the PMI report supports the case for further rate cuts by RBA in the second half of 2025.

Fed Powell testimony in focus, but no surprises expected

Fed Chair Jerome Powell’s testimony to Congress, on Tuesday and Wednesday, is the marquee event for markets this week. But investors shouldn’t expect any fireworks. with Fed having just held rates steady at 4.25–4.50% and published updated economic projections last week, markets aren’t expecting any major policy revelations. The subsequent Monetary Policy Report released Friday reinforced the central bank’s cautious, data-dependent stance in the face of tariff-related uncertainty.

Powell is likely to reiterate that monetary policy is “in a good place,” and that officials are watching closely to assess the pass-through of tariffs to inflation. Last week, he emphasized that no FOMC member is particularly confident in the current projections, highlighting just how clouded the outlook has become. While markets still expect rate cuts beginning in September, Powell will likely avoid committing to any specific timing.

In the meantime, US data flow will offer more clues on how the economy is absorbing the tariff shock. Durable goods orders, preliminary PMIs, goods trade balance, and consumer confidence are all due this week.

In Europe, hopes of a growth rebound are gaining traction. Analysts have pointed to signs that both Germany and the broader Eurozone could be turning a corner, helped by rising expectations of fiscal support. This week’s Eurozone PMIs and Germany’s Ifo index will either validate that story—or expose it as premature optimism.

Meanwhile, Summary of Opinions from BoJ’s June meeting could reveal increasing skepticism among policymakers about delivering another rate hike this year. That would reinforce market expectations that the next tightening move will be pushed into 2026. Elsewhere, inflation data from Australia and Canada will be important for timing rate cuts from RBA and BoC, both of which remain in easing mode.

Here are some highlights for the week:

- Monday: Australia PMIs; Japan PMIs; Eurozone PMIs; UK PMIs; US PMIs, existing home sales.

- Tuesday: Germany Ifo business climate; Canada CPI; US current account, house price index, consumer confidence.

- Wednesday: New Zealand trade balance; BoJ summary of opinions; Australia monthly CPI; Swiss UBS expectations; US new home sales.

- Thursday: Germany Gfk consumer sentiment; US Q1 GDP final, jobless claims, durable goods orders, goods trade balance, pending home sales.

- Friday: Japan Tokyo CPI, retail sales; Canada GDP; US personal income and spending, PCE inflation.

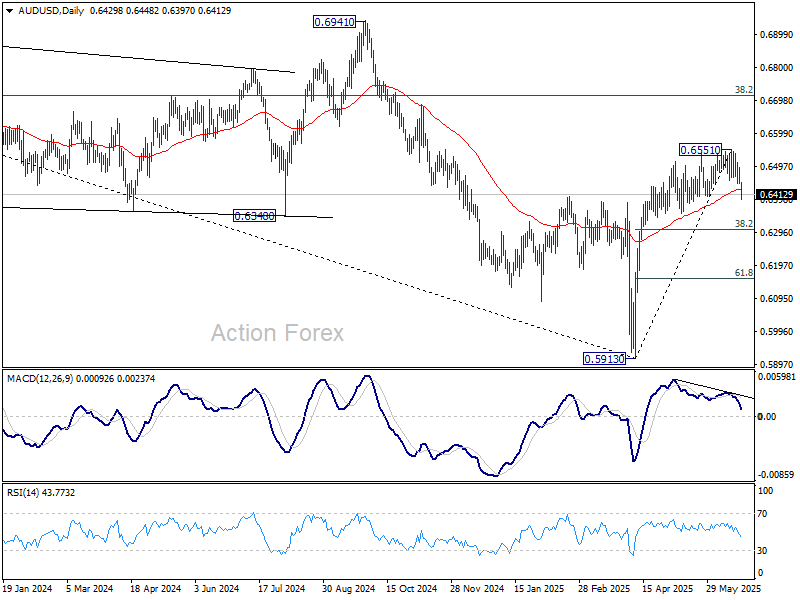

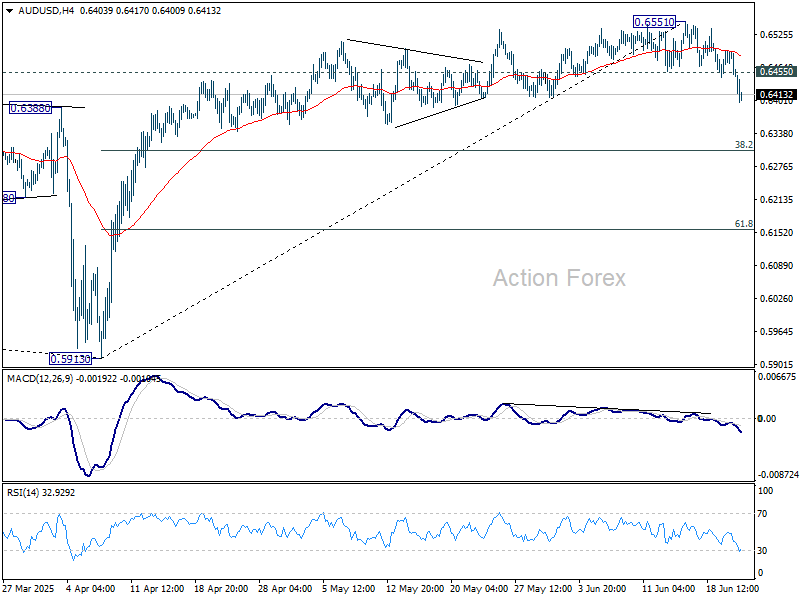

AUD/USD Daily Report

Daily Pivots: (S1) 0.6433; (P) 0.6465; (R1) 0.6481; More...

AUD/USD’s downside acceleration today confirms short term topping at 0.6551. Intraday bias is now on the downside for 38.2% retracement of 0.5913 to 0.6551 at 0.6307, even as a correction. Strong bounce from there will keep the fall as a corrective move. However, decisive break of 0.6307 will argue that it’s already reversing the rise from 0.5913 and target 61.8% retracement at 0.6157.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).