Risk Appetite Holds, Dollar Extends Losses Markets Eye PCE into Friday’s Finish – Action Forex

Global risk sentiment remains firm heading into the weekend, with both S&P 500 and NASDAQ pushing near record highs overnight. Asian markets followed suit, with Japan’s Nikkei breaking above the symbolic 40k mark, extending its robust rally driven by AI optimism and strong corporate earnings.

The bullish tone persists despite persistent warnings from Fed officials that a July rate cut is unlikely. Instead, Fed’s consistent message of “not now, but likely later” is reinforcing market hopes that easing will resume by fall. Most policymakers continue to emphasize patience due to tariff-related inflation risks, yet concede that inflation appears to be trending back toward target. This dovish tilt later in the year is offering enough support for equity bulls to stay in control.

Traders are now squarely focused on May’s US PCE inflation release. A modest rise is expected, with headline PCE set to climb to 2.3% and core PCE to 2.6%. A soft reading would further cement the case for September easing, while any significant surprise to the upside could temporarily dampen sentiment. For now, though, investors appear optimistic that inflation remains manageable.

In contrast, China delivered fresh disappointment. Industrial profits plunged -9.1% yoy in May, the steepest drop since last October, reflecting continued weakness in domestic demand and pricing power. Cumulative profits are down 1.1% year-to-date, despite Beijing’s targeted stimulus. The data highlight the limits of China’s support measures and add to growth concerns.

In currency markets, Dollar remains under pressure and looks set to finish the week as the worst performer, followed by Loonie and Yen. Swiss Franc leads on the upside, with Sterling and Kiwi close behind. Euro and Aussie are positioning in the middle.

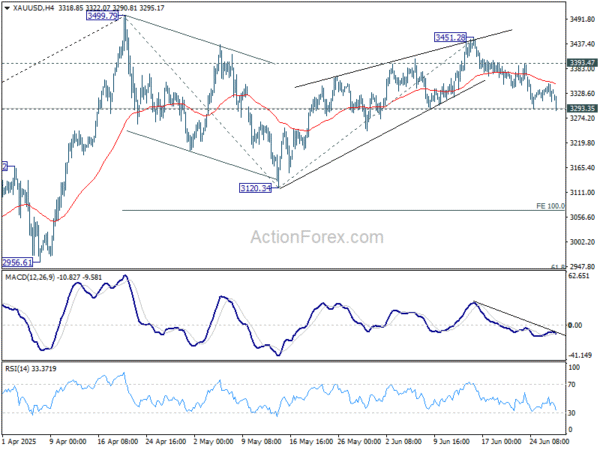

Technically, Gold’s weakness returns today and focus is back on 3293.35 support. Firm break there will resume the fall from 3451.28. That would also solidify the case that whole corrective pattern from 3499.79 is already in the third leg. Deeper decline should then be seen back to 3120.34 support.

In Asia, at the time of writing, Nikkei is up 1.56%. Hong Kong HSI is down -0.06%. China Shanghai SSE is down -0.21%. Singapore Strait Times is up 0.64%. Japan 10-year JGB yield is up 0.01 at 1.434. Overnight, DOW rose 0.94%. S&P 500 rose 0.80%. NASDAQ rose 0.97%. 10-year yield fell -0.040 to 4.253.

Tokyo core inflation slows to 3.1% in June, but food costs still surging

Tokyo’s core CPI (ex-fresh food) slowed more than expected in June, coming in at 3.1% yoy versus 3.6% yoy in May and below forecasts of 3.4% yoy. The decline was largely driven by the resumption of fuel subsidies and temporary reductions in utility charges. Core-core CPI, which strips out both fresh food and energy, also eased to 3.1% yoy from 3.3% yoy.

However, the figure masks ongoing strain on household budgets. Food prices (excluding volatile items) rose a sharp 7.2% yoy, accelerating from May’s 6.9% yoy. Tokyo consumers paid nearly 90% more for rice and faced eye-watering increases in chocolate and coffee costs. Service prices edged down slightly but remained elevated at 2.1%.

On the labor side, Japan’s May jobless rate held steady at 2.5%, while the job-to-applicant ratio slipped slightly to 1.24.

Fed’s Barr: Tariffs pose dual risk to inflation and jobs, justifying wait and see

Fed Governor Michael Barr said overnight that tariffs may pose a dual threat to the economy—lifting inflation expectations while simultaneously slowing growth. He pointed to survey data showing households anticipate sharp near-term price increases, which, coupled with supply chain reconfiguration and second round effects effects, could result in “some inflation persistence.”

At the same time, Barr acknowledged tariffs could cause the economy to slow and unemployment to rise,” disproportionately impacting low-income workers.

Given these uncertainties, Barr advocated for a patient policy approach. “Monetary policy is well positioned to allow us to wait and see how economic conditions unfold,” he said.

Fed’s Collins: July cut too soon, needs more data before moving

Boston Fed President Susan Collins said in a Bloomberg interview that July is too soon for a rate cut, pointing to the limited data available between now and the next FOMC meeting. “We’re only going to have really one more month of data before the July meeting,” she noted, adding, “I expect to want to see more information than that.”

Collins emphasized there’s no urgency to ease policy and reaffirmed her baseline view that cuts are likely later this year. Whether that translates to “one rate cut” or potentially more, she said, will depend entirely on how the data evolves.

Fed’s Kashkari needs clarity before cutting rates

Minneapolis Fed President Neel Kashkari reiterated the cautious stance on monetary policy, citing continued uncertainty over the inflationary impact of new tariffs. Speaking at an event overnight, Kashkari said the Fed needs to “go slow” until it gains more clarity, adding, “We still need to get a better assessment of what impact tariffs are going to have on the economy. We just don’t know yet.”

He noted that many businesses are hesitating to raise prices, fearing a backlash if tariffs are later reversed. Kashkari also highlighted the ability of supply chains to adapt and “find their way around and through barriers,” suggesting the inflation impact might be more muted than expected.

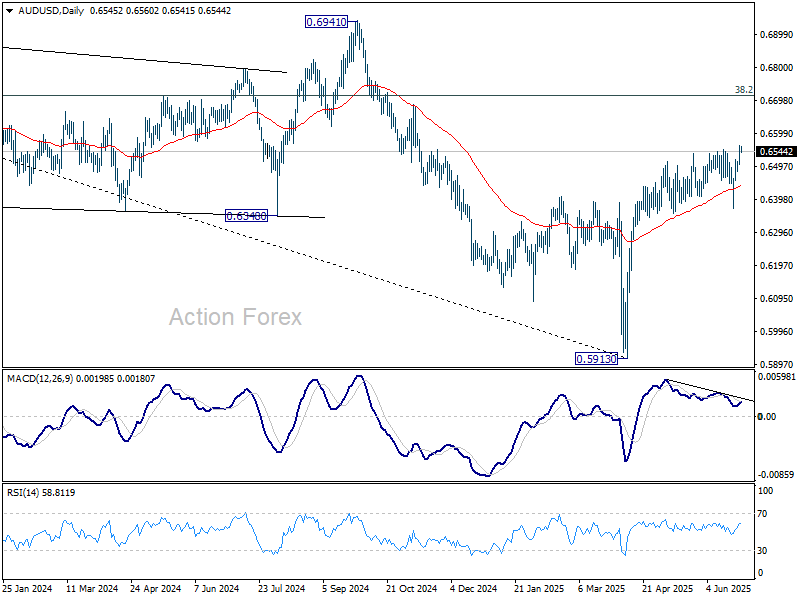

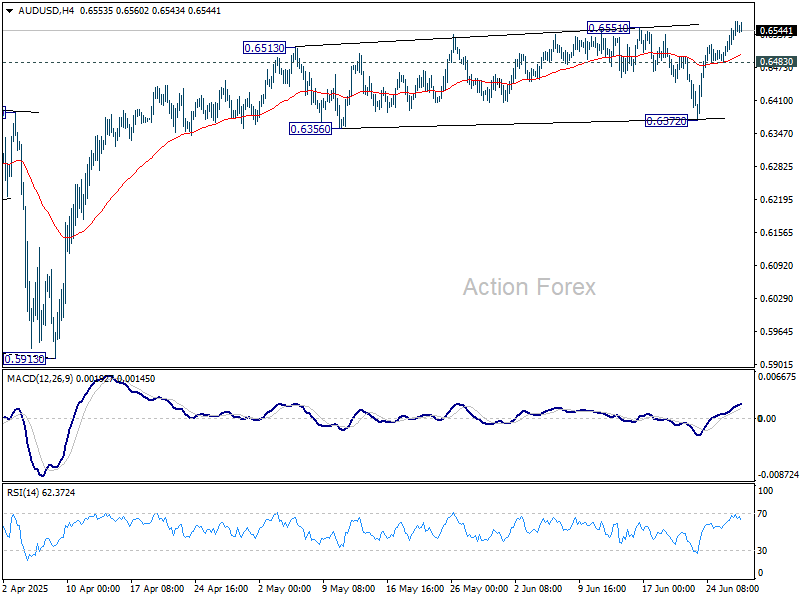

AUD/USD Daily Report

Daily Pivots: (S1) 0.6511; (P) 0.6538; (R1) 0.6572; More...

AUD/USD’s rise from 0.5913 finally resumed by breaking 0.6551 resistance. Intraday bias is back on the upside for 0.6713 fibonacci level. On the downside, below 0.6483 minor support will turn intraday bias neutral first. But near term outlook will now stay bullish as long as 0.6372 support holds, in case of retreat.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).