Markets Calm as US CPI Leaves Fed Outlook Unchanged, Yen Slides Continue – Action Forex

Markets shrugged off the latest US CPI release, with muted reactions across assets. While annual core inflation ticked slightly higher, the modest rise appears to be a relief for Fed and investors alike. Overall, the data does little to shift expectations around the Fed’s easing path.

The July FOMC meeting remains firmly priced for a hold, with over 97% probability. As for September, futures imply around 60% odds of a rate cut. However, with US tariffs set to escalate from August 1 and trade talks still ongoing, there is considerable uncertainty over the coming weeks.

In FX, the standout move is the continued weakness in Yen. The currency is under pressure as investors position cautiously ahead of this weekend’s upper house elections. Sharp gains in long-dated JGB yields reflect growing anxiety over future fiscal policies and deficit spending, regardless of the outcome.

Elsewhere, the Dollar and Euro are also softer. Sterling and Swiss Franc are trading closer to the middle of the pack. Commodity currencies are outperforming, led by Kiwi and Aussie, followed by the Loonie.

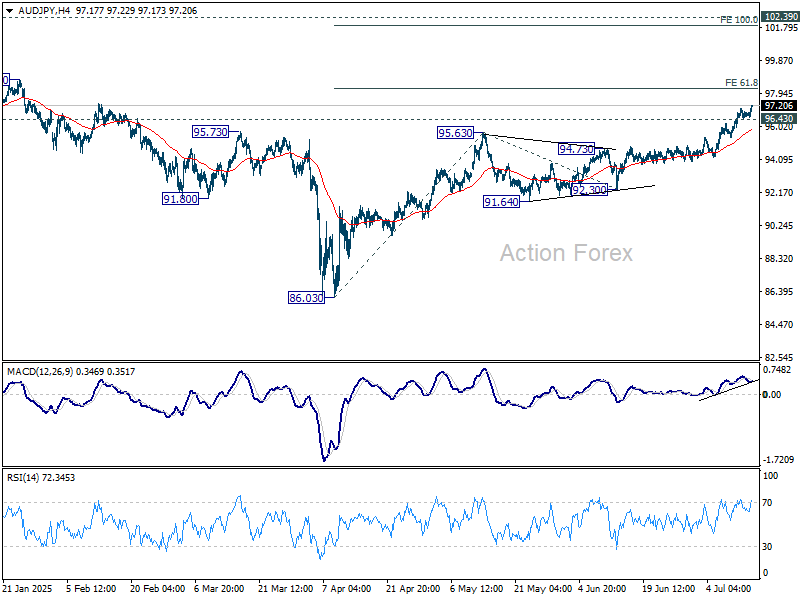

Technically, AUD/JPY’s rally continues today and is on track to 61.8% projection of 86.03 to 95.63 from 92.30 at 98.23. Decisive break there could prompt further upside acceleration to 100% projection at 101.90. On the downside, break of 96.43 support will bring consolidations first.

In Europe, at the time of writing, FTSE is up 0.03%. DAX is up 0.14%. CAC is up 0.01%. UK 10-year yield is down -0.044 at 4.564. Germany 10-year yield is down -0.054 at 2.678. Earlier in Asia, Nikkei rose 0.55%. Hong Kong HSI rose 1.60%. China Shanghai SSE fell -0.42%. Singapore Strait Times rose 0.26%. Japan 10-year JGB yield rose 0.015 to 1.592.

US CPI jumps to 2.7% yoy in June, core CPI undershoots expectation at 2.9% yoy

US CPI climbed 0.3% mom in June, matching forecasts, with the increase largely driven by a 0.2% mom rise in shelter costs and a 0.9% mom gain in energy prices. Food prices also edged higher, up 0.3% mom on the month. While the headline data aligned with expectations, the core CPI—excluding food and energy—rose just 0.2% mom, slightly below the anticipated 0.3% mom gain.

On a year-over-year basis, headline inflation jumped from 2.4% to 2.7%, in line with projections. However, core inflation ticked up only marginally from 2.8% to 2.9%, coming in under the 3.0% consensus. The annual energy index fell -0.8%, offering some offset to stickier components like food, which rose 3.0% over the year.

Canada’s CPI rises to 1.9% yoy in June, core measures unchanged

Canada’s CPI rose 0.1% mom in June, falling short of the expected 0.2% mom gain. On an annual basis, headline inflation accelerated from 1.7% yoy to 1.9% yoy, matching expectations. The increase was driven partly by a smaller year-on-year decline in gasoline prices and firmer price gains in durable goods like vehicles and furniture.

Meanwhile, BoC’s preferred core inflation measures remained unchanged, with median and trimmed CPI steady at 3.0% and the common measure holding at 2.6%.

German ZEW jumps to 52.7, positive sentiment firmly established

Germany’s ZEW Economic Sentiment index jumped from 47.5 to 52.7 in July, beating expectations of 50.2 and marking the third consecutive monthly rise. Current Situation Index also improved sharply from -72 to -59.5, above forecast of -66.0. The data suggests that investor confidence is firming despite lingering global trade tensions, likely supported by hopes for a de-escalation in US-EU tariff threats and anticipated domestic fiscal stimulus.

Eurozone sentiment also edged up modestly, with the expectations index rising from 35.3 to 36.1, though falling short of the 37.8 consensus. The current conditions measure rose by 6.5 points to -24.2, signaling a gradual improvement in the broader bloc’s outlook.

ZEW President Achim Wambach noted that nearly two-thirds of respondents expect Germany’s economy to improve, citing optimism tied to a resolution of the US-EU trade standoff and government-led investment. Expectations were especially upbeat in sectors like machinery, metals, and electrical manufacturing.

Eurozone industrial production grows 1.7% mom in May, EU up 1.5% mom

Eurozone industrial production jumped 1.7% mom in May, comfortably beating market expectations of 1.1% mom. The strength was broad-based across key sectors, with notable gains in energy (+3.7%), capital goods (+2.7%), and non-durable consumer goods (+8.5%). However, weakness in intermediate goods (-1.7%) and durable consumer goods (-1.9%) tempered the overall picture.

Across the broader EU, industrial production rose 1.5% mom. At the national level, Ireland led the surge with a sharp 12.4% mom rise, followed by Malta (+3.4%) and Germany (+2.2%). On the flip side, industrial activity contracted most in Croatia (-2.9%), Slovakia (-2.8%), and Belgium (-2.7%).

Australia Westpac consumer sentiment edges up to 93.1, RBA hold damps household optimism

Australia’s Westpac Consumer Sentiment index edged up 0.6% mom to 93.1 in July, but the modest gain masked a clear sense of disappointment among households.

Westpac noted that sentiment was noticeably stronger before the RBA’s July meeting, with those surveyed prior to the decision reporting a reading of 95.6. That slipped to 92 among those surveyed after the RBA unexpectedly held rates steady, suggesting the decision dashed hopes for relief.

As a result, consumer confidence remains stuck at what Westpac called “cautiously pessimistic” levels.

Looking ahead, markets are eyeing the RBA’s next meeting on August 11–12. While the central bank may pause again if Q2 inflation overshoots, the more likely scenario is a confirmation that inflation stays inside the 2–3% target range. That would pave the way for a 25bps rate cut in August, with another expected in November.

China Q2 GDP growth slows to 5.2%, but beats expectations

China’s economy expanded 5.2% yoy in Q2, slightly above expectations of 5.1% yoy but down from 5.4% yoy in Q1. Sector data showed balanced growth across industries—primary output rose 3.7%, secondary 5.3%, and tertiary 5.5%. The National Bureau of Statistics noted that macroeconomic policies have supported stability, but also flagged persistent weakness in domestic demand and external headwinds.

June’s data painted a mixed picture. Industrial production accelerated from 5.8% yoy to 6.8% yoy, beating forecasts of 5.6% yoy and suggesting continued strength in export-facing sectors and manufacturing. However, retail sales cooled to 4.8% yoy, down sharply from May’s 6.4% yoy and missed expectation of 5.2% yoy.

Fixed asset investment year-to-date slowed to 2.8%, well below expectations of 3.7%. The decline in property investment deepened, falling -11.2% in H1, and private investment contracted -0.6%.

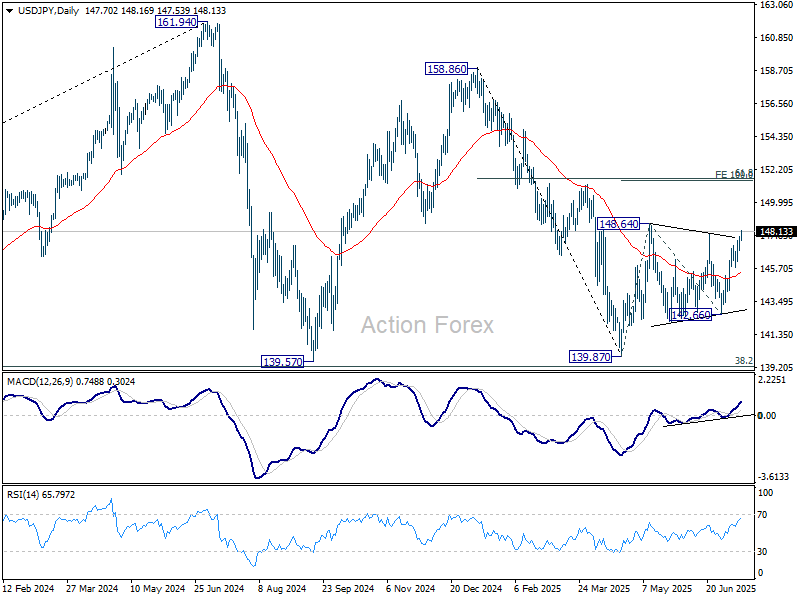

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.13; (P) 147.46; (R1) 148.05; More…

USD/JPY’s breach of 148.01 resistance suggests that corrective pattern from 148.64 has completed with three waves to 142.66. Intraday bias is on the upside for 148.64 resistance first. Firm break there will confirm and target 100% projection of 139.87 to 148.64 from 142.66 at 151.43. That is close to 61.8% retracement of 158.86 to 139.87 at 151.22. On the downside, below 146.84 minor support will mix up the outlook and turn intraday bias neutral again first.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.