Short-Covering Continues to Lift Yen, EU Said to Brace for Tariff Fight – Action Forex

Yen continues to lead the currency markets today, with fresh buying emerging in the early US session, particularly against Dollar. However, the rally appears more technical than structural, largely driven by short covering after Japan’s weekend election delivered no major surprises. Prime Minister Shigeru Ishiba’s Liberal Democratic Party lost its upper house majority, but the outcome had been widely anticipated.

Despite today’s gains, the broader outlook for Yen remains clouded by unfavorable fundamentals. Political uncertainty now looms larger, with Ishiba expected to cling to power through cooperation with opposition parties. That instability could complicate ongoing trade negotiations with the US, while keeping BoJ on the sidelines amid increased policy inertia.

Overall the currency markets, European currencies are also showing relative strength, led by Sterling which holds a mild edge over both Euro and Swiss Franc. On the other end, Dollar is underperforming, followed by commodity currencies including the Aussie and Kiwi and Loonie.

Tariff risks are back in focus following a Reuters report citing unnamed EU diplomats. US President Donald Trump’s threat of a 30% tariff by August 1 has raised alarm within the EU. Despite last week’s meetings between EU Trade Commissioner Maros Sefcovic and US officials, prospects for rolling back existing tariffs—such as the 50% on steel and 25% on autos—appear slim. The US has also floated baseline tariff rates well above 10%.

As the August 1 deadline approaches, EU policymakers appear more prepared to retaliate, even as they continue to prefer negotiation. A EUR 21B tariff package remains suspended until August 6, while another set targeting EUR 72B in US exports is under active consideration. More importantly, support is growing for deploying the EU’s anti-coercion instrument, though formal activation would require backing from a qualified majority.

Looking ahead, the upcoming RBA minutes will be closely scrutinized during the Asian session. This was the first meeting to reveal unattributed votes, showing a 6–3 split in favor of holding rates steady at 3.85%. The minutes may clarify whether it was a tactical delay or a sign of deeper dissent.

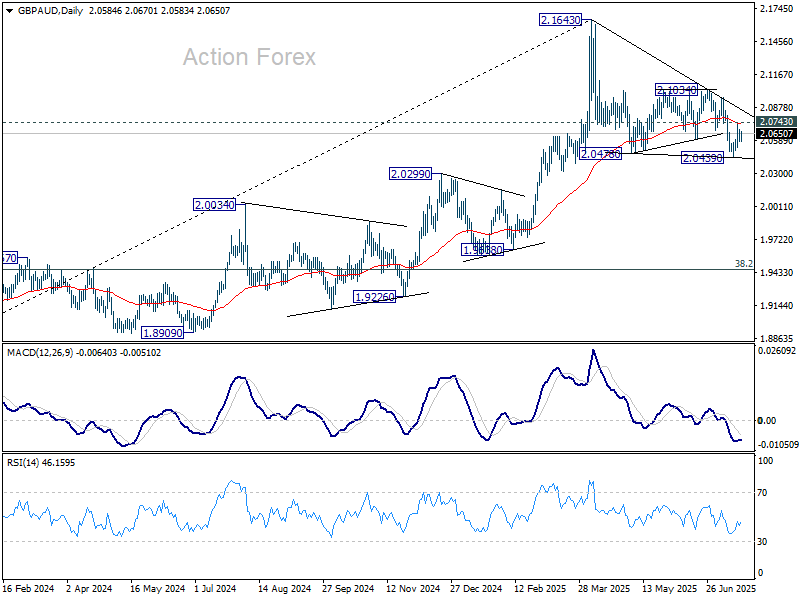

Technically, GBP/AUD could have formed a short term bottom at 2.0499 last week. Immediate focus is now on 2.0743 resistance and 55 D EMA (now at 2.0733). Sustained trading above this resistance zone will suggest that corrective pattern from 2.1643 has completed with three waves to 2.0499. Further rally should be seen to 2.1034 resistance next. Nevertheless, rejection by the EMA will extend the correction through 2.0439 before completion.

In Europe, at the time of writing, FTSE is down -0.09%. DAX is down -0.05%. CAC is down -0.41%. UK 10-year yield is down -0.061 at 4.618. Germany 10-year yield is down -0.068 at 2.629. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 0.68%. China Shanghai SSE rose 0.72%. Singapore Strait Times rose 0.42%.

ECB SAFE survey: Firms see slower inflation, trade shocks reorder priorities

The ECB’s latest SAFE (Survey on the Access to Finance of Enterprises) report showed that Eurozone firms have revised down their short-term inflation expectations while maintaining a cautious view on long-term price pressures. The median forecast for inflation one year ahead dropped to 2.5% from 2.9%. Expectations for three- and five-year horizons remained steady at 3.0%.

When asked about risks to five-year inflation, 52% of firms still viewed them as skewed to the upside, though that figure declined slightly from 55%. The share of firms seeing balanced risks increased to 33%, while those perceiving downside risks remained unchanged at 14%.

This round also included ad hoc questions about the impact of rising trade tensions, particularly recent US tariff announcements. The survey revealed uneven exposure across firms, with exporters to the US and manufacturing companies facing the greatest challenges. About 30% of respondents reported concerns over supply chain disruptions, including delays and shortages.

In response, many businesses are already pivoting. Firms cited plans to reorient sales toward domestic and EU markets and restructure supply chains to reduce dependency on vulnerable links.

NZ CPI rises to 2.7% yoy in Q2, tradeabales jump

New Zealand’s CPI rose 0.5% qoq in Q2, slightly below expectations for 0.6% qoq. Annual inflation ticked up to 2.7% yoy from 2.5% yoy but still undershot 2.8% yoy forecast. Headline inflation remained comfortably within the RBNZ’s target range of 1-3%. Tradeables inflation climbed sharply to 1.2% yoy from 0.3% yoy. Non-tradeables eased to 3.7% yoy from 4.0% yoy, indicating moderating domestic pressures.

The quarterly print showed notable increases in cultural services (+9.5% qoq), electricity (+4.9% qoq), and vegetables (+10.0% qoq), which together accounted for over 70% of the total quarterly CPI rise. However, these gains were partially offset by a -4.8% qoq drop in petrol prices and -9.2% qoq decline in domestic accommodation services.

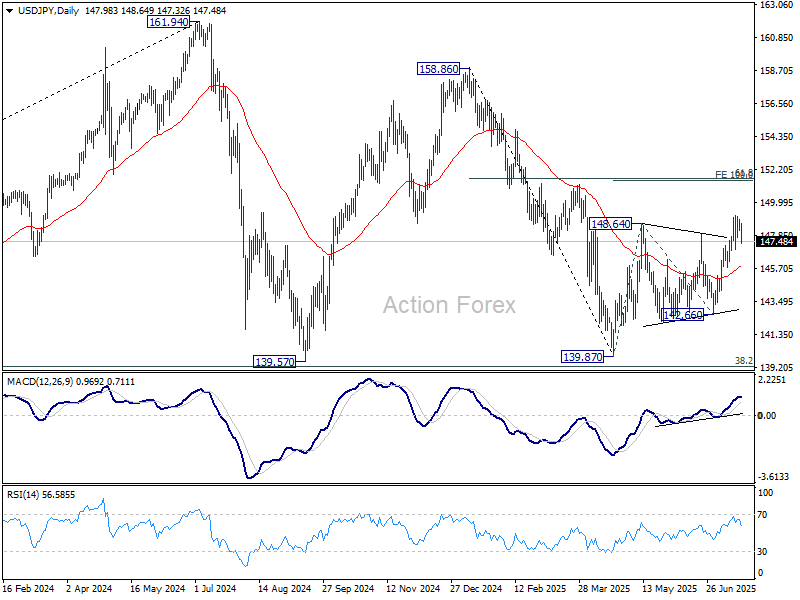

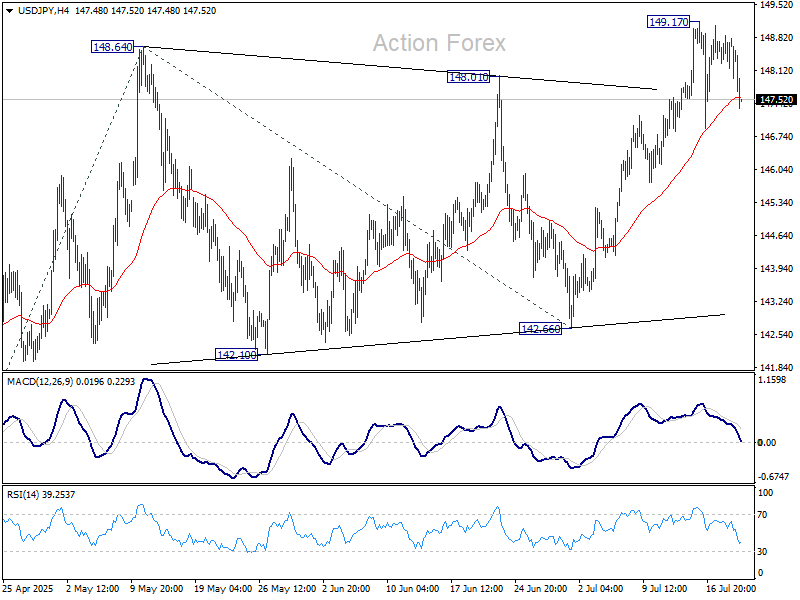

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.39; (P) 148.64; (R1) 149.08; More…

USD/JPY dips lower today as consolidations continues below 149.17. Intraday bias stays neutral and further rally is expected as long as 55 D EMA (now at 145.86) holds. On the upside, break of 149.17 will target 100% projection of 139.87 to 148.64 from 142.66 at 151.43. That is close to 61.8% retracement of 158.86 to 139.87 at 151.22.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.