Hot US GDP Lifts Dollar, Eyes Now on Fed – Action Forex

Dollar strength resumed in early US session after US Q2 GDP blew past expectations with a 3.0% annualized growth rate. The data added further confirmation that the US economy remains remarkably resilient, reinforcing bullish bets on the greenback. Currency markets reacted swiftly, with traders piling back into Dollar longs after briefly taking profit earlier in the week.

Equity markets, however, were more subdued. Futures on major US indexes remained near flat, as investors chose to wait out the FOMC decision. Even with inflation clearly cooling, there’s little pressure on the Fed to act swiftly. Instead, today’s events may reaffirm a “higher for longer” stance as long as growth remains robust.

The Fed is widely expected to keep its policy rate unchanged at 4.25–4.50%. Attention will be on whether dovish members like Waller and Bowman continue to call for a cut, and if others show signs of joining them. Given today’s solid data, the bar for broader support for immediate easing likely remains high.

Attention will also be squarely on Chair Jerome Powell’s press conference and the FOMC statement for any hints of a September move. With market pricing hovering around a 65% chance for a cut, any less-than-dovish language could see Dollar bulls press further.

So far, the greenback is leading currency performance on the day, followed by Yen and Sterling. On the weak side, Aussie continues to lag after soft Q2 inflation readings. Euro and Swiss Franc also remain under pressure, while Kiwi and Loonie are stuck in the middle of the pack.

Looking ahead, the spotlight will shift quickly to BoJ’s decision in the Asian session. While a hold at 0.50% is expected, Deputy Governor Shinichi Uchida’s earlier remarks flagged that economic projections would reflect the positive impact of the US-Japan trade deal. That sets the stage for a potential hawkish twist. If BoJ drops even subtle hints that a rate hike later this year is back in play, Yen shorts may find themselves squeezed.

Technically, AUD/JPY’s price actions from 97.41 short term top are seen as a near term corrective pattern only. Another rally is still expected to 61.8% projection of 86.03 to 95.63 from 92.30 at 98.23. However, sustained break of 55 D EMA (now at 95.00) will raise the chance of bearish reversal, and target 92.30 support first.

In Europe, at the time of writing, FTSE is down -0.22%. DAX is up 0.10%. CAC is up 0.42%. UK 10-year yield is down -0.032 at 4.607. Germany 10-year yield is down -0.003 at 2.708. Earlier in Asia, Nikkei fell -0.05%. Hong Kong HSI fell -1.36%. China Shanghai SSE rose 0.17%. Singapore Strait Times fell -0.24%. Japan 10-year JGB yield fell -0.13 to 1.563.

US GDP surges 3.0% annualized in Q2, inflation gauges ease

US GDP growth accelerated to 3.0% annualized in Q2, far above expectations, as falling imports and firmer consumer spending powered the expansion. These gains were partially offset by weaker investment and exports, though the data suggest domestic demand remains firm.

Notably, inflation pressures eased significantly. The PCE price index rose just 2.1% in Q2, down from 3.7% in Q1, while the core PCE gauge slowed to 2.5% from 3.5%.

US ADP jobs grow 75k, ongoing labor market resilience

U.S. private payrolls grew 104k in July, beating expectations of 75k and suggesting continued strength in the labor market. Gains were broad-based, with 31k new jobs in goods-producing industries and 74k in services. Hiring was evenly spread across firm sizes, with both medium and large companies contributing 46k each.

Wage pressures held steady, with pay up 4.4% yoy for job-stayers and 7% for job-changers, unchanged for the fourth consecutive month.

ADP’s Chief Economist Nela Richardson noted the data points to “a healthy economy” as employers grow more confident in consumer resilience.

Eurozone GDP beats with 0.1% qoq growth, but Germany and Italy contract

Eurozone GDP grew 0.1% qoq in Q2, slightly above market expectations of flat growth, while the broader EU expanded 0.2% qoq. On a year-over-year basis, GDP rose 1.4% yoy in the Eurozone and 1.5% yoy in the EU—marking a mild deceleration from Q1’s annual pace of 1.5% yoy and 1.6% yoy respectively. .

Spain led the quarter with a strong 0.7% qoq gain, followed by Portugal (0.6%) and Estonia (0.5%). However, Germany and Italy both posted marginal contractions of -0.1%, and Ireland saw the largest drop at -1.0%. Despite the mixed quarterly results, all member states reported positive year-on-year growth.

Australia CPI cools to 2.1% in Q2, June reading undershoots

Australia’s inflation pressures continued to ease in Q2, reinforcing expectations for further policy easing from the RBA.

Headline CPI rose 0.7% qoq, down from Q1’s 0.9% qoq and under the 0.8% qoq consensus. On an annual basis, CPI slowed from 2.4% yoy to 2.1% yoy, the lowest since early 2021, and below expectation of 2.2% yoy.

Trimmed mean inflation, the RBA’s preferred gauge, also moderated from 0.7% qoq to 0.6% qoq. Annual rate fell from 2.9% to 2.7% yoy, matched expectations, and marking the lowest since Q4 2021.

Underlying disinflation is broadening too. Annual services inflation cooled from 3.7% yoy to 3.3% yoy, the weakest since Q2 2022. Goods inflation dipped back to 1.1% yoy after a brief uptick from Q4’s 0.8% yoy to Q1’s 1.3% yoy.

The June monthly CPI dropped from 2.1% yoy to 1.9% yoy, also below expectations of 2.1% yoy, and undershoots RBA’s 2-3% target band.

NZ ANZ business confidence ticks up to 47.8, easing inflation signals more RBNZ cuts ahead

New Zealand’s ANZ Business Confidence ticked higher in July, rising from 46.3 to 47.8. Own Activity Outlook edged down slightly from 40.9 to 40.6. The share of firms expecting to raise prices over the next three months dropped to 43.5%—the lowest since December 2024. Inflation expectations also dipped from 2.71% to 2.68%.

ANZ described the inflation signals as “benign,” noting declines across both cost and pricing expectations. The bank suggested that RBNZ may soon shift from worrying about inflation staying too high to concerns about it falling too low, implying a greater likelihood of deeper monetary easing than currently priced in by markets or flagged by the RBNZ itself.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1510; (P) 1.1554; (R1) 1.1590; More…

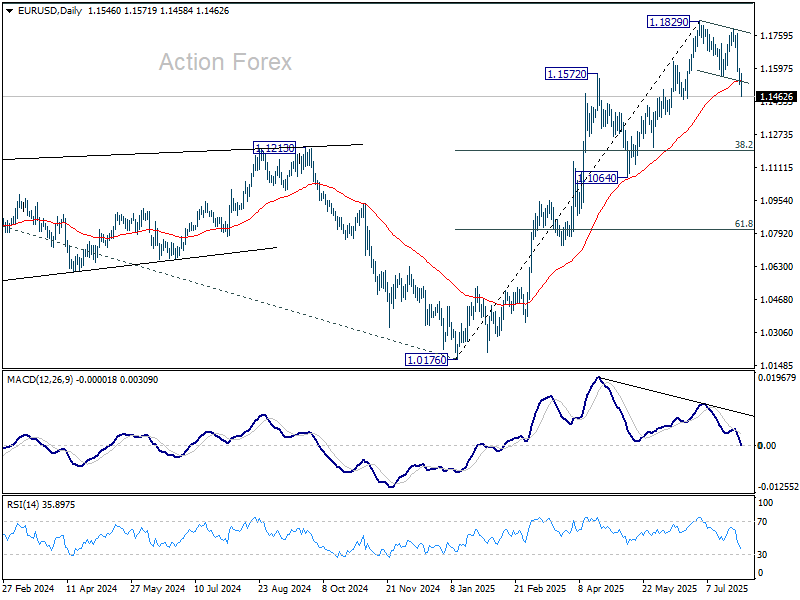

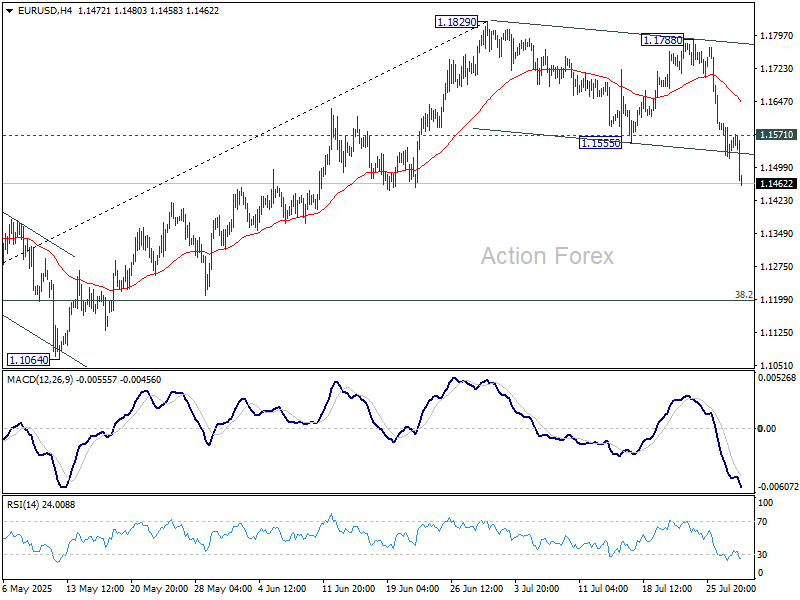

EUR/USD’s current downside acceleration and strong break of 55 D EMA (now at 1.1536) suggests that fall from 1.1829 is already correcting the whole rally from 1.0176. Intraday bias stays on the downside for 38.2% retracement of 1.0176 to 1.1829 at 1.1198. On the upside, above 1.1571 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.