Tariff Update Sparks Limited Market Fallout, Dollar Eyes NFP for Further Gains – Action Forex

Asian equities slipped slight today after U.S. President Donald Trump issued a long-anticipated executive order updating tariff rates following the August 1 trade truce deadline. But losses were relatively restrained as many of Asia’s key exporters avoided the harshest duties. While tariffs now top out at 41%, nations like Thailand, Malaysia, and Taiwan saw their rates reduced from previous threats. US equity futures were also little changed while the currency markets are largely stable. As the latest trade war escalation may already be well priced in, traders are now turning attention to upcoming U.S. non-farm payroll data.

On the FX board, Dollar is easily the strongest performer for the week so far. Better-than-expected ADP and jobless claims data earlier in recent weeks have raised the likelihood of a firm NFP print. A stronger jobs number would likely reinforce the Fed’s hold stance and put further pressure on expectations for multiple cuts this year. Also in focus is ISM manufacturing report for July.

Loonie has also held up well. Trump’s threat to penalize Ottawa with new tariffs over its foreign policy was shrugged off by traders, given that affected goods are outside the USMCA framework. Sterling remains solid as well, with no major data shocks and the BoE maintaining its slow-but-steady easing path.

At the weaker end, Euro leads losses, but it;s; just largely correcting its late-July rally. Swiss Franc and Kiwi are not far behind. Aussie and Japanese are trading in mid-pack territory. Yen has settled after a volatile week dominated by mixed interpretation on BoJ’s stance on future rate hikes.

On the trade front, Trump’s new tariff order imposes reciprocal duties between 10% and 41% on dozens of nations. In addition, a 40% duty will apply to any transshipped goods designed to circumvent tariffs. Unlisted nations automatically fall under a 10% surcharge. These tariffs will begin on August 7 to give US customs officials time to prepare.

Among major takeaways, Switzerland and South Africa face sharp tariffs of 39% and 30%, respectively. In contrast, Thailand and Malaysia see their rates trimmed to 19%, down from 36% and 24% respectively. Taiwan will face a 20% tariff, cut from the earlier 32% level. Importantly, China remains untouched under this directive, as both sides continue to negotiate toward a longer-term deal after the 90-day truce expires on August 12.

In Asia, at the time of writing, Nikkei is down -0.64%. Hong Kong HSI is down -0.77%. China Shanghai SSE is down -0.49%. Singapore Strait Times is down -0.28%. Japan 10-year JGB yield is down -0.001 at 1.555. Overnight, DOW fell -0.74%. S&P 500 fell -0.37%. NASDAQ fell -0.03%. 10-year yield fell -0.016 to 4.360.

Gold and Silver vulnerable as strong NFP could supercharge Dollar rally

Copper’s collapse this week has triggered renewed weakness across metals, with Silver and Gold also on the back foot. However, underlying, it’s Dollar’s unrelenting strength that’s proving most punishing for precious metals. The next catalyst? The July US non-farm payroll report due today.

NFP is expected to show 102k job growth, a slight rise in the unemployment rate from 4.1% to 4.2%, and solid wage gains of 0.3% mom.

This month, only two of the usual four leading indicators are available to help guide expectations. The ADP report posted a 104k rise in private jobs, a bounce from last month’s downward surprise. Meanwhile, the 4-week moving average of initial jobless claims fell to 221k.

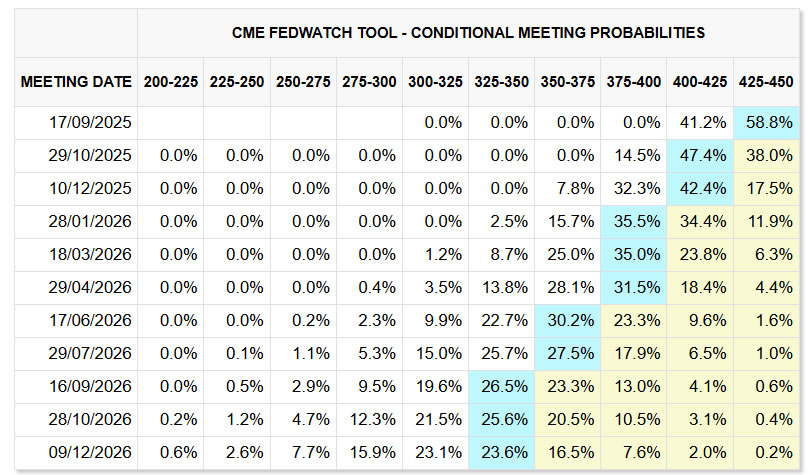

Taken together, these suggest a decent chance of an upside surprise in today’s payrolls release. That would likely trigger further hawkish adjustment in Fed expectations. After this week’s solid GDP and Powell’s cautious tone, markets have already dialed back bets on aggressive easing.

Fed fund futures are pricing just a .2% chance of a September rate cut, and only 40.1% chance of two cuts this year. A robust NFP report could shift expectations further toward a single cut in 2025, providing fresh tailwinds for the Dollar and keeping downward pressure on Gold and Silver.

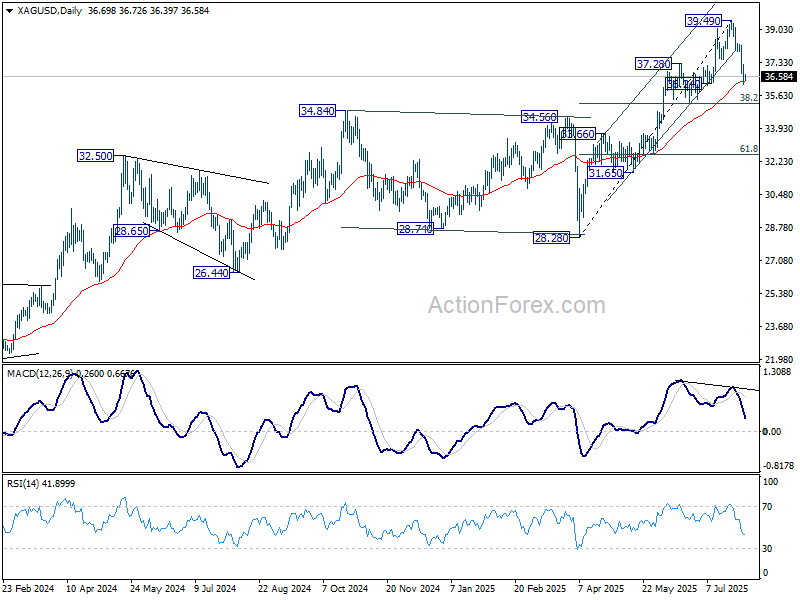

Technically, Silver’s extended fall this week should confirm completion of the five-wave rally from 28.28, on bearish divergence condition in D MACD. While 55 D EMA (now at 36.33) might provide interim support, the correction from 39.49 should at least extend to 38.2% retracement of 28.28 to 39.49 at 35.20 before completion.

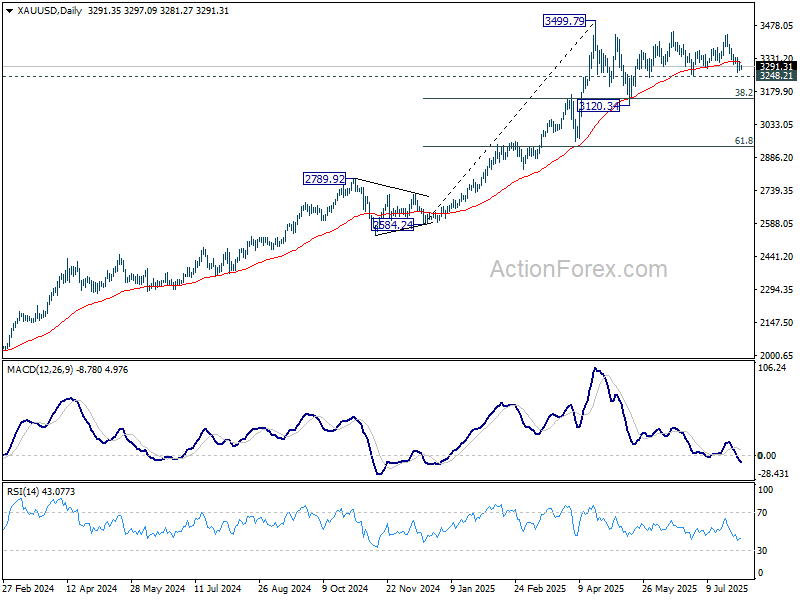

Gold is extending the medium term corrective pattern from 3499.79 high. Immediate focus is on 3248.21 support. Firm break there will open up deeper fall to test 38.2% retracement of 2584.24 to 3499.79 at 3150.04 again.

China Caixin PMI manufacturing contracts again as export demand falters

China’s Caixin Manufacturing PMI dropped from 50.4 to 49.5 in July, signaling renewed contraction in factory activity and marking the second sub-50 reading in the past three months.

S&P Global’s Jingyi Pan noted that manufacturing production declined for only the second time since October 2023, as firms pulled back operations amid cautious demand outlook heading into H2 2025.

Weaker foreign demand was again a key drag, with export orders remaining sluggish amid global trade tensions. Domestic sales saw some resilience thanks to business development efforts, but overall growth was described as “only fractional.”

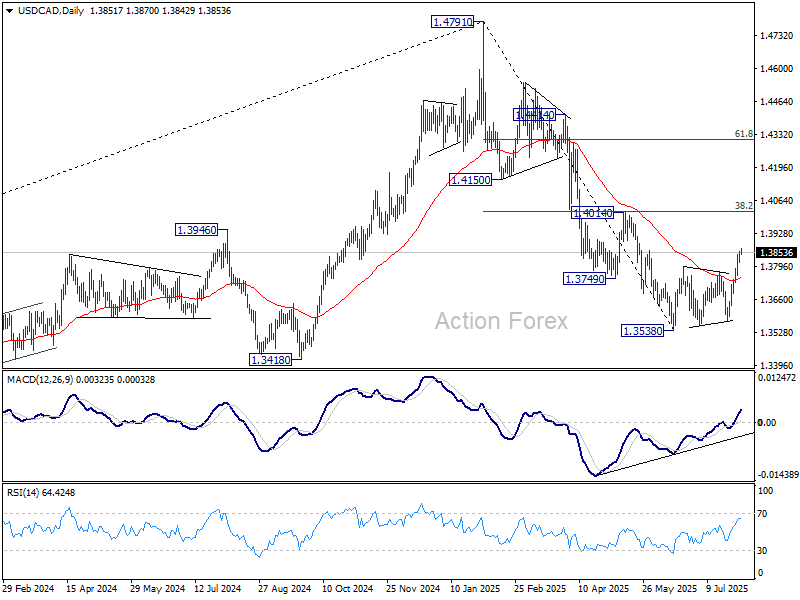

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3828; (P) 1.3843; (R1) 1.3873; More…

USD/CAD’s rally is in progress and intraday bias stays on the upside. Rise from 1.3538 is seen as correcting the decline from 1.4791 and would target 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 14017). But strong resistance should be seen there to limit upside. On the downside, below 1.3812 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.