French Politics Weighs on Euro, But Selling Fails to Gain Momentum – Action Forex

Currency markets stayed quiet overall, even though French politics briefly unsettled sentiment. French stocks dropped sharply as Prime Minister Francois Bayrou’s government looked increasingly at risk ahead of a September 8 confidence vote on his proposed budget cuts. Euro softened in response, though losses were limited.

Bayrou’s chances of survival are slim after three main opposition parties — the National Rally, Greens, and Socialists — confirmed they would not back him. Should the government lose the vote, President Emmanuel Macron would have to either name a new prime minister, keep Bayrou in a caretaker role, or call snap elections, all scenarios that would extend political uncertainty.

In the broader FX market, Dollar is the strongest performer for the day so far, followed by Aussie and Loonie. Euro lagged most, with Yen and Swiss Franc also soft, while Sterling and the Kiwi traded mid-pack.

Attention now shifts to Australia, where July CPI is due in the upcoming Asian session. Headline inflation is forecast to rise to 2.3% yoy from 1.9% yoy, though the increase largely reflects statistical effects from the expiry of electricity rebates.

Focus now shifts to the upcoming Australian monthly CPI release. Inflation is expected to jump from 1.9% yoy to 2.3% yoy, largely due to the unwinding of electricity rebates. A softer reading would provide some relief for the RBA but is unlikely to accelerate its easing timeline.

As highlighted in today’s RBA minutes, policymakers will need clearer evidence of labor market slack before considering faster rate cuts. Until then, the central bank appears content with a gradual pace of easing.

US durable goods fall -2.8% mom, but core orders show resilience

U.S. durable goods orders fell -2.8% mom to USD 302.8B in July, marking the third decline in four months but performing better than forecasts of -4.0% mom. Transportation equipment, also down in three of the past four months, was the main drag, plunging -9.7% mom to USD 101.7B. Ex-defense orders also slipped -2.5% to USD 284.5B.

Stripping out the volatile transport sector, however, orders rose 1.1% mom to USD 201.1B, far stronger than the 0.3% mom expected. The positive core reading suggests that underlying business investment remains more stable than the headline figure implies, limiting concerns of a broader manufacturing downturn.

RBA minutes: Not yet possible to decide pace of further easing

Minutes of RBA’s August 11–12 meeting showed policymakers unanimously backed the 25bps cut to 3.60%, citing stronger evidence that inflation is heading sustainably toward the midpoint of the 2–3% target range. The Board agreed that full employment can be preserved while inflation continues easing, though members noted risks remain in both directions.

The central bank noted that some further reduction in cash rate likely to be needed “in the coming year”. But it also stressed that the pace of further reductions will be determined “meeting by meeting” as new data emerges. While some indicators still suggest a tight labor market and inflation projected to stay slightly above target in the medium term, private demand is recovering, supporting the case for a “gradual pace”.

At the same time, the minutes noted conditions that could justify a”slightly faster” pace of easing. If the labor market is already “in balance”, or if risks shift more clearly to the downside—whether through weaker global growth or slower employment handover—then a quicker reduction in the cash rate could be warranted to avoid undershooting inflation.

Overall, members concluded it is “not yet possible” to judge whether easing will be gradual or slightly faster. RBA left the door open for both paths, emphasizing that data will drive the speed of policy adjustments in the months ahead.

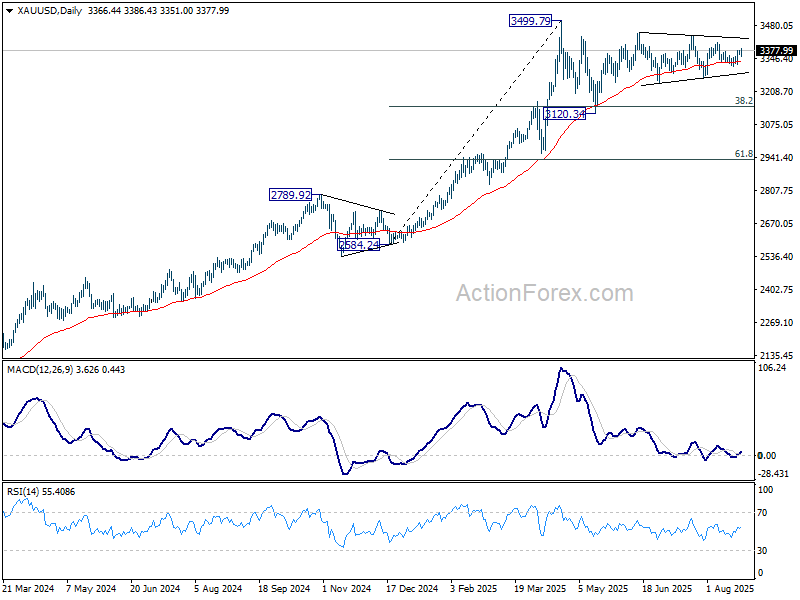

Gold bounces as Trump escalates clash with Fed, but gains lack follow-through

Gold bounced modestly this week as markets digested U.S. President Donald Trump’s unprecedented attempt to fire Fed Governor Lisa Cook. The move marked a sharp escalation in Trump’s long-running feud with the central bank, where he has repeatedly pressed for faster rate cuts but stopped short of threatening Chair Jerome Powell before his term expires next year.

Investors interpreted the move as an effort to reshape the Fed’s balance, raising the risk of a more politically driven policy stance. That uncertainty spurred some safe-haven demand for Gold, but follow-through buying has been limited. The metal remains confined within this month’s 3,300–3,400 range.

In the bigger picture, Gold has been trapped between 3,100 and 3,500 for more than three months. The long-term uptrend remains intact, but it’s unsure whether another leg down will unfold before the market finally tests resistance at the 3,500 threshold.

For now, break above near-term resistance at 3,408.21 is needed to signal momentum is turning higher. Without that, Gold’s outlook stays neutral, with sideways trading likely to dominate in the days ahead.

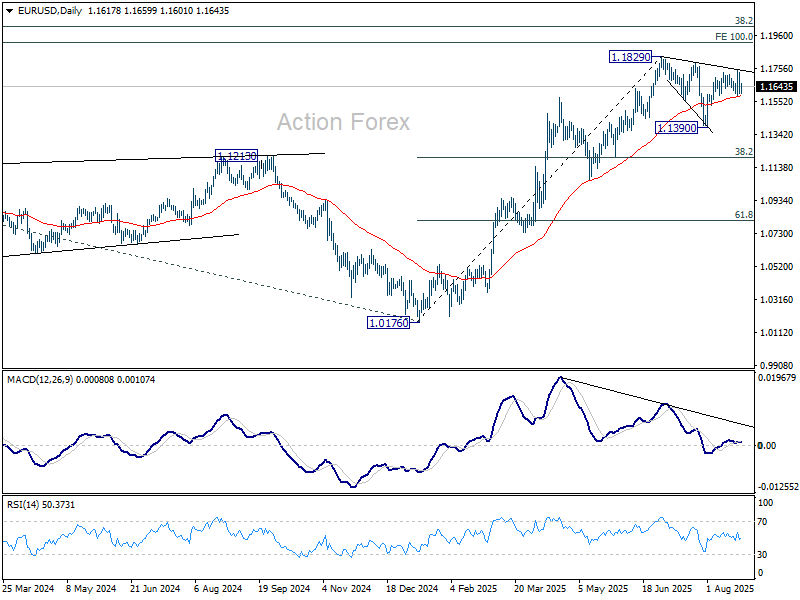

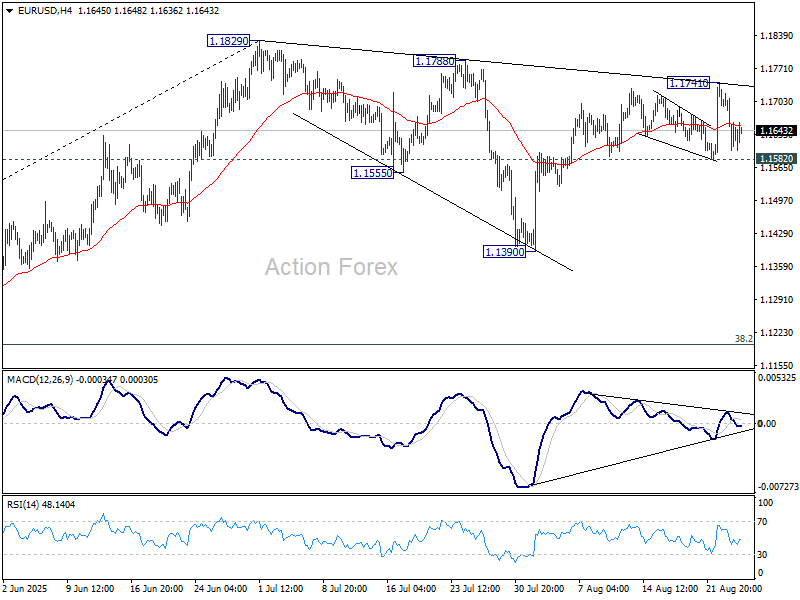

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1572; (P) 1.1650; (R1) 1.1697; More…

EUR/USD is holding above 1.1582 support despite current retreat. Intraday bias remains neutral and further rise is in favor. Above 1.1741 will resume the rally from 1.1390 to retest 1.1829 high. Firm break there will extend larger up trend. However, decisive break of 1.1582 will extend the corrective pattern from 1.1829 with another downleg, and target 1.1390.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.