Dollar Holds Firm in Quiet Trade, EU Moves to Accelerate Tariff Cuts – Action Forex

Dollar firmed again today in what remains a subdued week for markets, with no top-tier European economic data releases so far and little central bank commentary on the docket. The summer lull has left trading ranges tight, and with nothing scheduled during the US session, conditions are expected to remain muted.

For the week so far, Dollar continues to hold the top spot in FX performance, followed by Loonie and Aussie. At the other end, the Euro has been the weakest, trailed by Yen and Kiwi, while the Swiss Franc and Sterling sit in the middle of the pack.

Attention in Europe turned to trade developments. According to Bloomberg, the European Union is preparing to fast-track legislation to remove tariffs on U.S. industrial goods. The move comes after Washington insisted that lower duties on EU autos and parts would only take effect once Brussels acted to eliminate industrial tariffs more broadly.

Currently, European cars and auto parts face a steep 27.5% U.S. tariff. While the U.S. and EU agreed last month on a framework that would lower tariffs on nearly all EU exports to 15%, US President Donald Trump stressed that autos were excluded until the EU presented legislative changes. If Brussels delivers by month-end, the tariff rate on cars would be retroactively reduced to 15% effective August.

Still, the German Chambers of Industry and Commerce, DIHK, urged caution. In its August survey, firms stressed the need for a consistent strategy from EU policymakers, arguing that the bloc must not compromise its “economic sovereignty” for short-term trade concessions.

Negotiations between Washington and Brussels remain ongoing. While the July framework and subsequent joint statement offered progress, significant uncertainty persists over tariff treatment for metals and cars, leaving exporters wary. DIHK added that the EU should be ready to use countermeasures if needed, while continuing to push for the eventual abolition of tariffs deemed inconsistent with WTO rules.

In Europe, at the time of writing, FTSE is flat. DAX Is down -0.08%. CAC is up 0.44%. UK 10-year yield is down -0.024 at 4.721. Germany 10-year yield is down -0.018 at 2.712. Earlier in Asia, Nikkei rose 0.30%. Hong Kong HSI fell -1.27%. China Shanghai SSE fell -1.76%. Singapore Strait Times rose 0.04%. Japan 10-year JGB yield rose 0.001 to 1.627.

German Gfk consumer confidence falls to -23.6 on job fears

Germany’s GfK Consumer Sentiment index for September dropped to -23.6 from -21.7, falling short of expectations at -21.2. It was the third consecutive monthly decline, with NIM’s Rolf Bürkl describing sentiment as “definitely in the summer slump.”

The key driver was a sharp fall in income expectations as worries about job security intensified. Registered unemployment remained just below three million in July, but analysts expect that mark to be breached in August. Consumers’ expectations of rising unemployment have reached their highest level of the year.

Australia CPI jumps to 2.8%, highest in a year, rules out September RBA cut

Australia’s monthly CPI spiked to 2.8% yoy in July, well above expectations of 2.3% yoy and up sharply from 1.9% yoy in June. It was the highest annual inflation rate since July 2024, breaking several months of easing price pressures. Core measures also firmed, with CPI excluding volatile items rising from 2.5% yoy to 3.2% yoy and trimmed mean jumping back from 2.1% yoy to 2.7% yoy, a pace last seen three months ago.

The result adds to concern that inflation is proving sticky, though July’s data, as the first month of the quarter, is skewed toward goods and offers less insight into services inflation than subsequent months.

For the RBA, the print is a warning sign but not a trigger for panic. Policymakers will want to wait for the full quarterly inflation update before adjusting course. Today’s data nonetheless rules out a September cut.

Barring a significant deterioration in the labor market or other downside shocks, the more realistic timeline for the next rate move remains November.

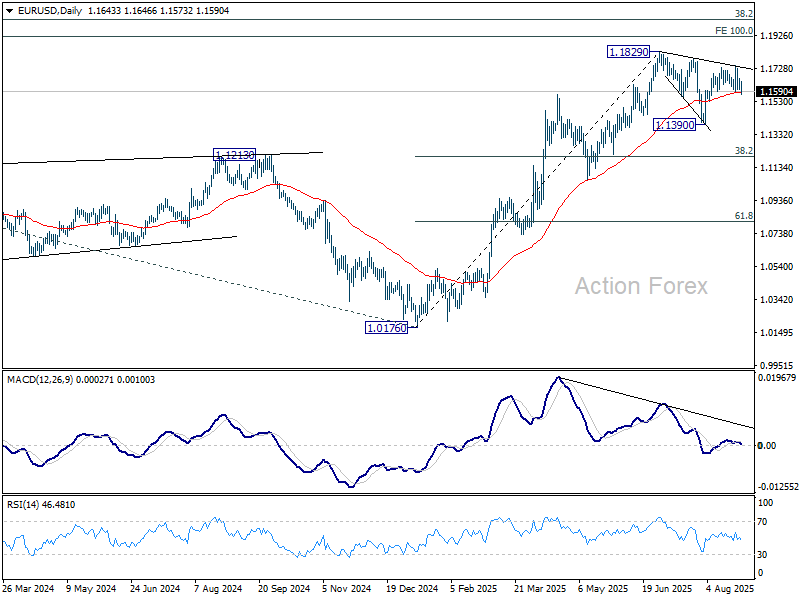

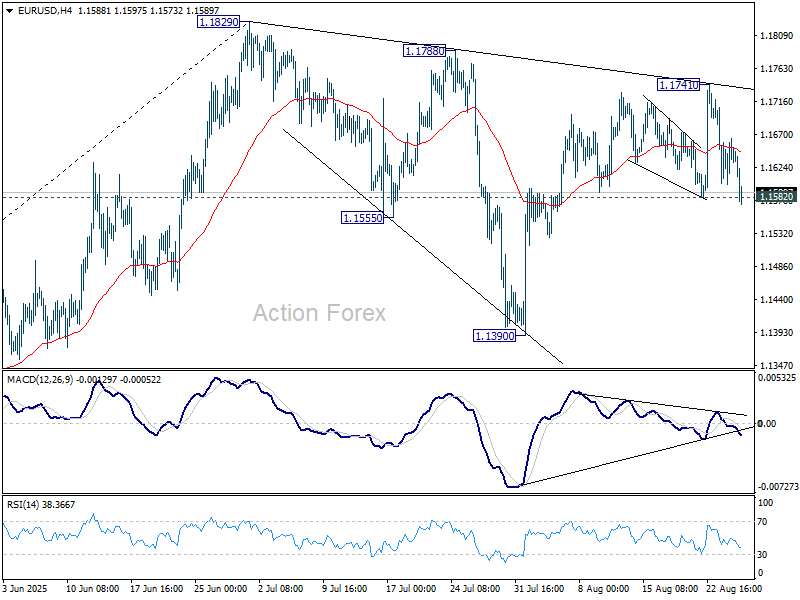

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1607; (P) 1.1636; (R1) 1.1670; More…

EUR/USD breached 1.1582 support briefly but cannot sustain below the level yet. Intraday bias stays neutral first. On the upside, above 1.1741 will resume the rally from 1.1390 to retest 1.1829 high. Firm break there will extend larger up trend. However, decisive break of 1.1582 will extend the corrective pattern from 1.1829 with another downleg, and target 1.1390.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.