Dollar Softens, Yen Leads as Markets Eye ECB Minutes – Action Forex

U.S. equities closed higher overnight, but Asian markets turned mixed on Thursday as risk sentiment remained muted. Nvidia’s stronger-than-expected earnings beat on both revenue and profit dominated headlines but failed to deliver a sustained boost to risk appetite.

In currency markets, Dollar softened as this week’s rebound lost steam. Overall trading remained subdued with no major catalysts. Yen led gains on the day, followed by Loonie and Swiss Franc. On the downside, Euro lagged most, trailed by Dollar and Kiwi, while Sterling and Aussie held middle ground.

Focus in Europe was on the release of the ECB’s July meeting minutes. Policymakers left rates unchanged at 2.00% and subsequent data has pointed to stronger-than-expected growth alongside inflation holding near the 2% target. That combination has reduced the urgency for further easing in the near term.

Trump’s imposition of a 15% tariff on most EU goods has so far tracked with ECB assumptions, averting worst-case outcomes. As a result, markets now largely expect the ECB to stand pat again on September 11, barring sharp downside surprises in upcoming flash inflation and survey data. The debate has shifted toward whether there will be a case for more easing later in the year, but for now the bar remains high.

On the trade front, Japan’s top negotiator Ryosei Akazawa canceled a trip to Washington that was intended to cover tariff issues. Chief Cabinet Secretary Yoshimasa Hayashi said technical disagreements had surfaced, requiring continued talks at the administrative level instead.

Kyodo News reported no decision has been made on rescheduling, while Reuters suggested Akazawa could head to Washington next week. Tokyo has made clear it will press the U.S. to revise its reciprocal tariff order and seek lower duties on autos and parts. The delay highlights the fragility of trade talks even between close partners.

In Asia, at the time of writing, Nikkei is up 0.69%. Hong Kong HSI is down -1.12%. China Shanghai SSE is down -0.22%. Singapore Strait Times is down -0.03%. Japan 10-year JGB yield is flat at 1.626. Overnight, DOW rose 0.32%. S&P 500 rose 0.24%. NASDAQ rose 0.21%. 10-year yield fell -0.020 to 4.238.

NZ ANZ business confidence rises to 49.7, weak spots reinforce RBNZ’s dovish tilt

New Zealand’s ANZ Business Confidence index improved modestly in August, rising to 49.7 from 47.8. However, firms’ Own Activity Outlook slipped to 38.7 from 40.6. Sector pressures also persisted, with reported employment in construction falling sharply.

Inflation indicators eased further. The share of firms expecting to raise prices in the next three months fell to 43%, while cost expectations edged down to 74%. One-year inflation expectations also dipped to 2.63% from 2.68%. Wage growth expectations 12 months out softened to 2.4% from 2.5%.

ANZ said the survey aligns with the RBNZ’s updated view that the economy requires “a little more support” to ward off downside risks. While confidence is stabilizing, the recovery will unfortunately “not come soon enough for some”.

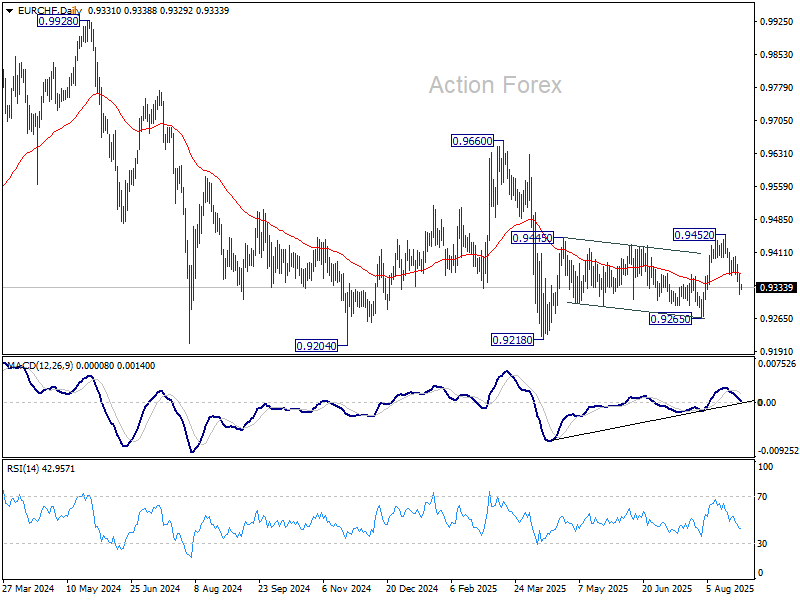

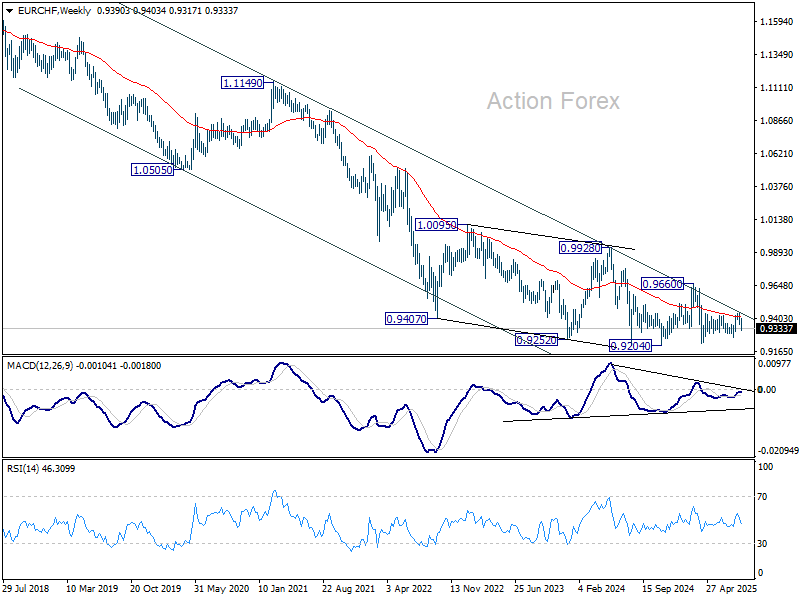

EUR/CHF turns lower as risk sentiment outweighs Swiss fundamentals

Swiss Franc extended gains against Euro this week, driven primarily by risk-off sentiment. French political turmoil hit the common currency, and the scale of Franc’s move highlighted how haven demand eclipsed domestic policy and economic debates.

SNB Vice Chairman Antoine Martin’s remarks on inflation and negative rates provided some context, but they did little to alter the market narrative. Martin noted the central bank sees no risk of deflation and expects inflation to rise, while stressing that the bar for reintroducing negative rates is high.

Domestic developments, including the 39% U.S. tariffs on Swiss exports and today’s Q2 GDP release, carry weight in principle. But markets view these as secondary in the near term, with the real impact of tariffs unlikely to be visible until later this year.

Technically, this week’s extended decline in EUR/CHF suggests that corrective rebound from 0.9218 has completed with three waves up to 0.9452. That came after rejection by falling 55 W EMA (now at 0.9359). Outlook is clearly still bearish. Deeper fall should be seen to 0.9265 support in the near term. Firm break there will open deeper decline, at least for a retest of 0.9204 support (2024 low).

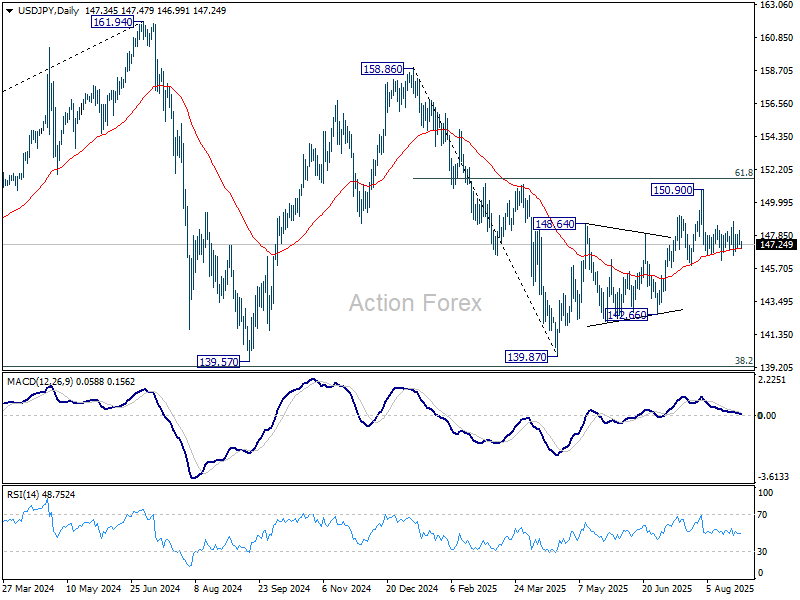

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.08; (P) 147.63; (R1) 147.97; More…

USD/JPY dips mildly today but stays in range of 146.20/148.76 and intraday bias stays neutral first. On the downside, firm break of 146.20 will resume the fall from 150.90. Also, that would argue that rebound from 139.87 has completed as a corrective move to 150.90. Deeper fall should be seen to 142.667 support for confirmation. On the upside, above 148.76 will bring another rise to retest 150.90 instead.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.