Breakout or Breakdown? Gold, Dollar, and China Rally to Shape Risk Into Year-End – Action Forex

The past week was anything but quiet for global markets, even if headline price moves in currencies looked muted. Beneath the surface, three powerful narratives are colliding: political turmoil in the U.S. that threatens the independence of its central bank, a legal battle that could reshape global trade policy, and a relentless equity surge in China that is redefining investor sentiment.

Each of these developments carries implications that stretch beyond their immediate headlines. For some, it means renewed demand for havens. For others, it means technical signals flashing warnings of a deeper turn ahead. And for risk-sensitive currencies, it offers both opportunity and vulnerability.

Gold has reemerged as a crisis hedge, propelled higher by institutional uncertainty and legal challenges in Washington. Dollar, despite firm U.S. data, continues to wobble as traders look ahead to the anticipated Fed cut within weeks. Meanwhile, the Shanghai Composite’s march toward a pivotal resistance level has injected new energy into Asia-linked trades, with Australian Dollar riding the wave.

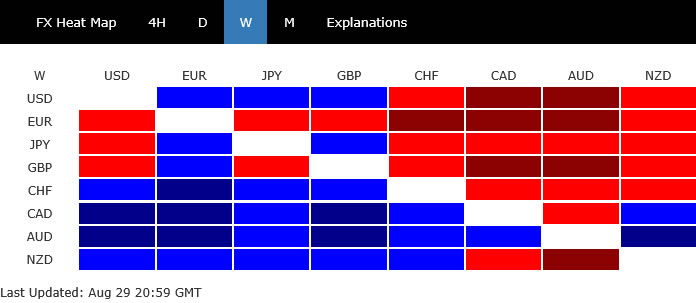

For currency traders, the week’s performance scoreboard told its own story: commodity currencies surged, with the Aussie leading, followed by Loonie and Kiwi. At the other end, European majors lagged, with Euro, Sterling, and Yen under pressure. Dollar and Franc sat uncomfortably in the middle.

Against this backdrop, the coming weeks may prove decisive. Will Gold confirm its breakout, will Dollar lose its structural footing, and can Chinese equities sustain their ascent? The answers could reshape FX flows and risk sentiment into year-end.

Gold Rally Signals Crisis Hedge as Fed Fight and Tariff Ruling Stir Risks

Gold’s performance last week stood out sharply against otherwise subdued global markets. The precious metal gained momentum for its role as a refuge in times of deepening political and institutional turmoil in the US.

The most pressing issue for markets has been the ongoing challenge to the Fed’s independence. U.S. President Donald Trump has made no secret of his desire to bring interest rates down more aggressively and has sought to exert stronger influence over the central bank. His latest move — an attempt to fire Fed Governor Lisa Cook — has intensified fears about the Fed’s autonomy.

Cook has filed a lawsuit contesting the legality of her removal. A hearing on her request for a temporary bar against Trump’s action ended Friday without a ruling, leaving markets in limbo. Legal experts note that the case could ultimately land in the Supreme Court, potentially setting precedent on whether presidents have authority to dismiss Fed officials at will.

If Trump prevails, he would likely be able to install a majority of the Fed Board aligned with his policy preferences. That would mark a profound shift in how monetary policy is set, raising concerns that rate decisions could be guided more by political imperatives than by economic data. For Gold, such risks have reinforced safe-haven flows.

The second area of turbulence is trade policy. On Friday, a U.S. appeals court ruled 7-4 that most of Trump’s tariffs are illegal, challenging one of his hallmark economic strategies. The decision applies to the “reciprocal” tariffs imposed in April and to earlier measures targeting China, Canada, and Mexico.

While the court allowed tariffs to remain in place until October 14 pending appeal, the ruling casts doubt on their durability. Markets now await whether the Trump administration will pursue a Supreme Court appeal. Analysts believe the White House has been preparing contingency plans — a “Plan B” — to preserve tariffs under different legal statutes should this challenge succeed.

For Gold, the combination of political disputes, Fed instability, and trade-policy risk forms a potent mix of supportive drivers. Investors are seeking insurance against outcomes that could shake confidence in both U.S. institutions and the global trading system.

Technically, Gold accelerated higher towards the end of the week and breached 3451.28 resistance. here are various interpretations on the price actions from 3499.79 record high. But in any case, further rally is now expected in Gold as long as 3404.20 support holds. Next target is 3499.79 high, and break there will pave the way to 161.8% projection of 3267.90 to 3408.21 from 3311.30 at 3538.32 in the near term.

More importantly, decisive break of 3499.79 will confirm long term up trend resumption. That would set the stage for medium term rally to 261.8% projection of 1160.17 to 2074.84 from 1614.60 at 4009.20, that is 4000 psychological level.

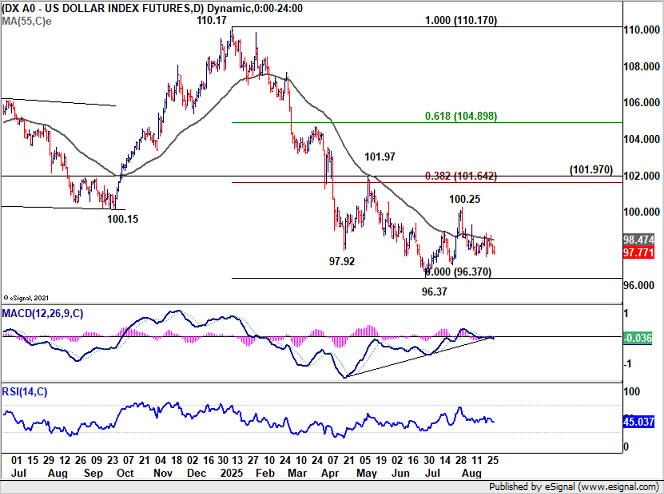

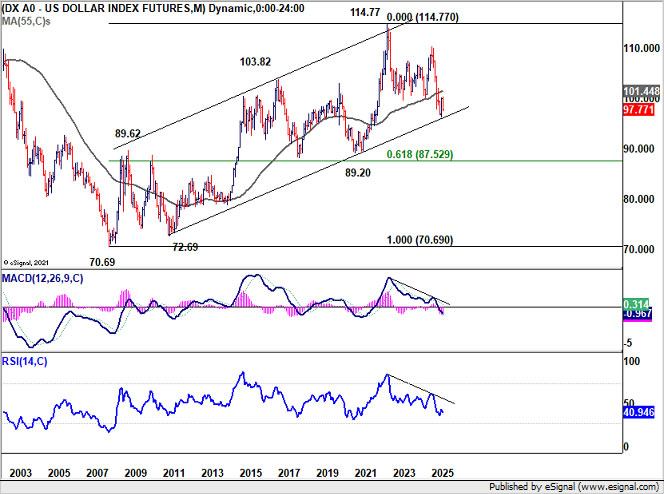

Dollar Index Fails 55 D EMA Again, Risk Builds for Break Below 96.37

Dollar closed last week on a sluggish note, with a half-hearted rally attempt fading quickly and leaving the greenback mixed across the board. Despite relatively upbeat economic data, sentiment around the currency remains heavy, with markets firmly focused on the Fed’s expected easing in September.

Durable goods orders surprised to the upside, Q2 GDP was revised higher, and jobless claims edged down. Personal spending also impressed, reinforcing the view that households remain in strong shape despite global headwinds. Inflation data provided no surprises, with both headline and core PCE landing on expectations.

The resilience in data, however, did little to sway Fed expectations. Markets continue to price a September rate cut as the beginning of a new easing cycle, with two cuts expected in total this year.

The more intriguing development came from Fed Governor Christopher Waller. He warned that waiting for further labor market deterioration would risk the Fed “falling behind the curve.” He argued conditions already justify a shift toward neutral policy, which he places near 3%—some 125 to 150 basis points below current levels.

Waller suggested more easing will come over the next three to six months, though the pace remains open—whether as a sequence of cuts or gradual moves with pauses. His clear message was that policy should move steadily toward neutral, with the only question being how quickly.

Crucially, Waller is seen as a potential successor to Chair Jerome Powell when his term ends next year. His alignment with Trump’s preferences, and the possibility of the administration securing a majority on the Board by removing Governor Lisa Cook, highlights how Fed policy could be reshaped if political influence grows.

Technically, the Dollar Index has once again failed to sustain a break above its 55 D EMA (now at 98.47). Near-term risks remain tilted to the downside, with a retest of 96.37 low likely.

Importantly, firm break of 96.37 could mark a decisive move out of the long-standing uptrend channel from the 2008 low at 70.69, signaling the start of a medium-to-long-term downtrend toward sub-90 levels.

Meanwhile, even if the corrective pattern from 96.37 manages to have another rising leg, strong resistance should be seen from 38.2% retracement of 110.17 to 96.37 at 101.64 to cap upside.

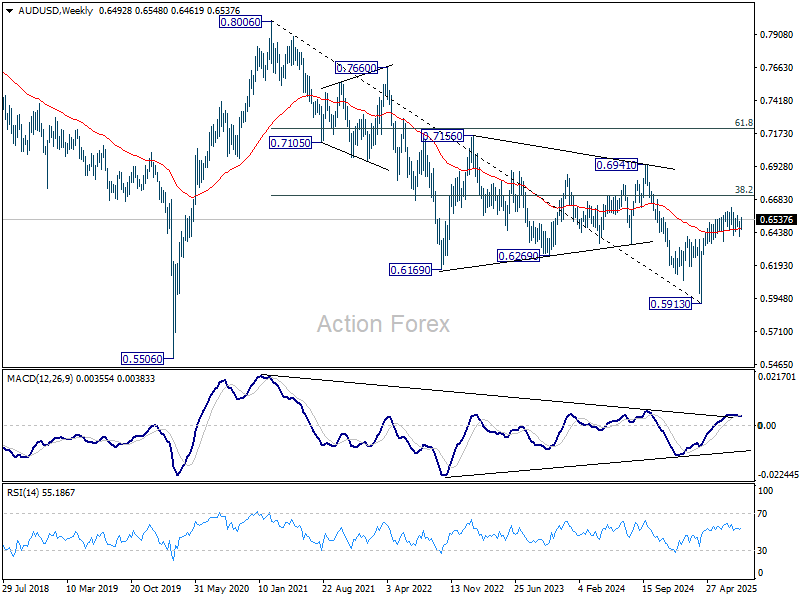

China’s SSE Rally Nears Pivotal 4000, Aussie Awaits Break or Rejection

Chinese equities have surged to decade highs last week, with the rally fueled by state-backed institutions, large investors, and gradually returning retail participation. The powerful move has provided a much-needed boost to market sentiment, with ripple effects extending to currencies tied closely to China, notably Australian Dollar.

On the bullish side, relatively low valuations and ample liquidity are highlighted as reasons for the rally’s sustainability. Retail investors, who has been keeping a large portion of their savings in low-yielding deposits in the past few years, are expected to start rotating into equities. This flow of funds could create a fresh wave of demand, reinforcing momentum in the months ahead.

Yet skepticism lingers about the durability of this boom. The majority of Chinese household wealth is tied up in property, which remains in a prolonged downturn. Without stronger property markets, the wealth effect of equities alone may be limited.

For now, however, optimism is dominant, and Aussie has emerged as the strongest performer in the currency markets, riding on hopes of sustained Chinese strength. Should SSE Composite extend its rally further, the tailwind for AUD could help offset the drag from expectations of additional RBA easing.

Technically, the 4000 level on the Shanghai SSE Composite presents a formidable resistance. It coincides with both 100% projection of 2689.70 to 3674.40 from 3040.69 at 4027.24 and the major trendline that has spanned for nearly two decades. This zone is likely to prove difficult to overcome, at least on the first attempt.

Failure at 4000 would likely result in a pullback, with a drop below 3704.99 pointing to rejection and setting up deeper correction toward 55 D EMA (now at 3612.66).

Conversely, decisive break above 4000 would be a game-changer, signaling strong underlying momentum in Chinese equities. Medium-term target would then point toward 161.8% projection at 4635.79. .

A strong break of SSE above 4000 could be a trigger for AUD/USD to break through 38.2% retracement of 0.8006 (2021 high) to 0.5913 at 0.6713 to set up long term bullish trend reversal.

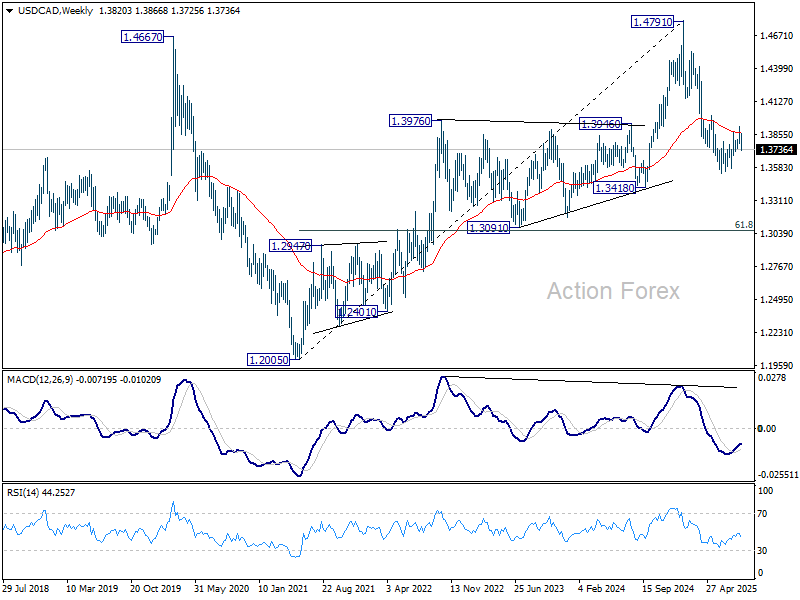

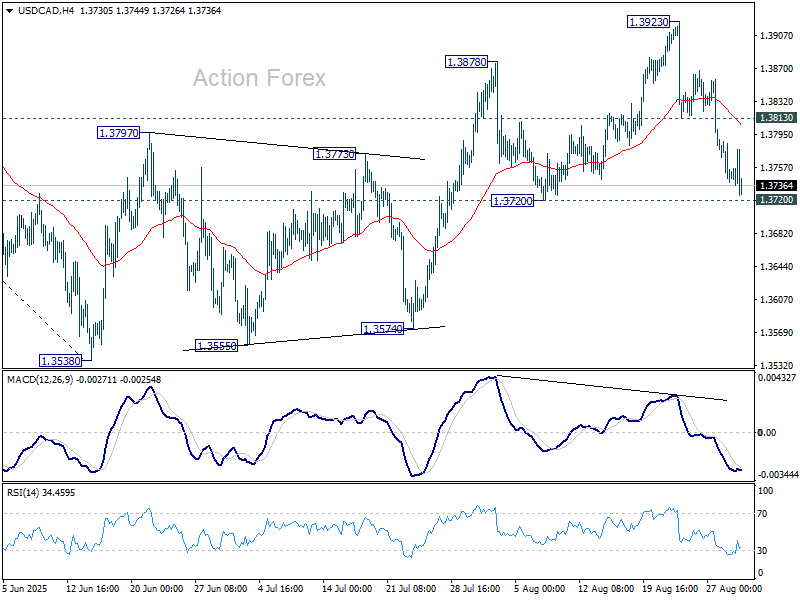

USD/CAD Weekly Outlook

USD/CAD dropped sharply last week but still hold on to 1.3720 support. Initial bias stays neutral this week first. On the downside, decisive break of 1.3720 will argue that the corrective pattern from 1.3538 has already completed at 1.3923. Intraday bias will be back on the downside for 1.3574 support first. Break there will bring retest of 1.3538 low. On the upside, though, break of 1.3813 resistance will retail near term bullishness, and bring retest of 1.3923 high instead.

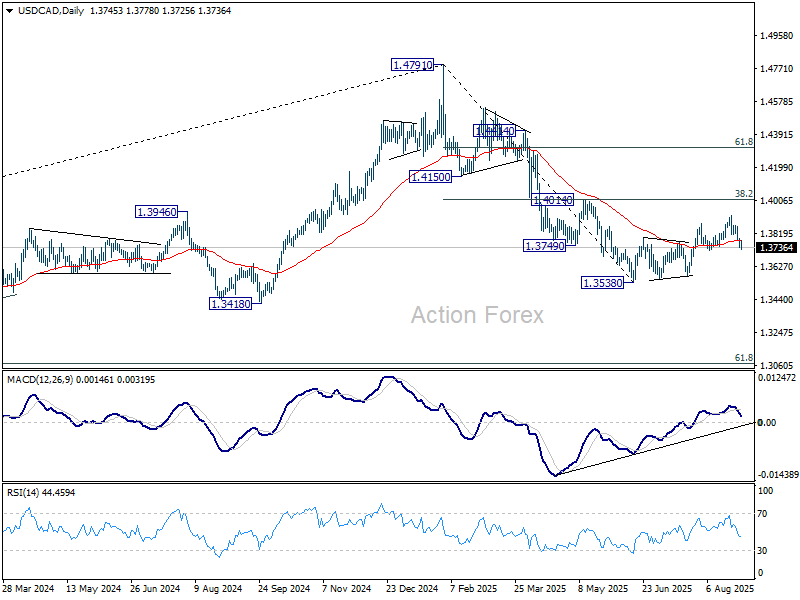

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

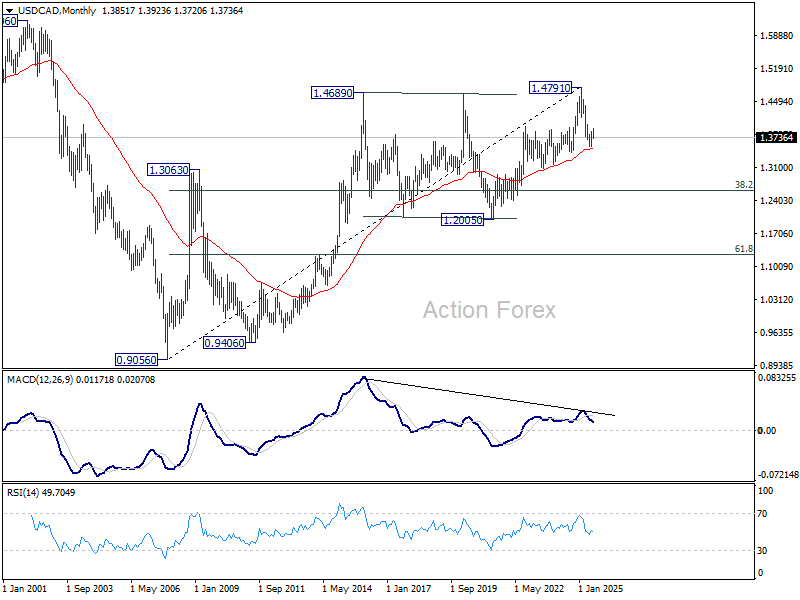

In the long term picture, as long as 55 M EMA (now at 1.3514) holds, up trend from 0.9056 (2007 low) should still resume through 1.4791 at a later stage. However, sustained trading below 55 M EMA will argue that the up trend has already completed, with rise from 1.2005 to 1.4791 as the fifth wave. 1.4791 would then be seen as a long term top and deeper medium term down trend should then follow.