Loonie Steady as BoC Cuts as Expected, Fed Now in Spotlight – Action Forex

The forex markets were steady in early U.S. trading, with the BoC’s widely expected 25bps rate cut to 2.50% generating little reaction. The decision was fully priced in, and the absence of fresh guidance left traders reluctant to adjust positions.

The BoC struck a cautious balance in its statement, offering no explicit signal of further cuts. Policymakers acknowledged risks to both growth and inflation, but the tone suggested slightly more concern about the economy and labor markets than price pressures. This leaves the door open for more easing, though the Bank appears inclined to proceed carefully.

Attention now shifts firmly to the Fed’s policy announcement. A 25bps cut to 4.00–4.25% is widely anticipated, but the real market drivers will be the voting split, the updated economic projections, and the tone of Chair Jerome Powell’s press conference. Together, these will shape expectations for the pace of easing into 2026.

In currency performance so far this week, Dollar remains the weakest, reflecting markets’ anticipation of Fed easing. Aussie and Kiwi have also lagged, while Sterling and Loonie are holding steady in the middle of the pack. Safe-haven demand has supported Swiss Franc, which leads the majors, followed by Euro and then Yen.

For now, traders are in wait-and-see mode. The Fed’s communication will be decisive in determining whether Dollar’s selloff deepens, whether yields break below 4%, and whether risk assets such as equities and Gold extend their strong runs.

In Europe, at the time of writing, FTSE is up 0.47%. DAX is up 0.44%. CAC is down -0.08%. UK 10-year yield is down -0.013 at 4.631. Germany 10-year yield is down -0.015 to 2.680. Earlier in Asia, Nikkei fell -0.25%. Hong Kong HSI rose 1.78%. China Shanghai SSE rose 0.37%. Singapore Strait Times fell -0.32%. Japan 10-year JGB yield fell -0.012 to 1.592.

BoC cuts to 2.50%, warns trade shocks still a drag

The BoC lowered its overnight rate by 25bps to 2.50% at today’s meeting, in line with widespread expectations. The move underscores the central bank’s effort to provide additional support as Canada’s economy struggles with weaker growth and softer inflation risks.

In its statement, the Governing Council said a “weaker economy and less upside risk to inflation” justified the cut, helping to better balance risks. The Bank highlighted that shifts in global trade continue to “add costs” even as they “weigh on economic activity.”

Looking ahead, policymakers said they will be closely monitoring how U.S. tariffs and evolving trade relationships affect exports, investment, employment, and household spending. They also flagged the risk that supply chain reconfiguration could pass higher costs onto consumers, stressing that inflation expectations remain a key guide for future decisions.

Eurozone CPI finalized at 2.0%, services drive price growth

Eurozone inflation was confirmed at 2.0% yoy in August, unchanged from July, while core CPI held steady at 2.3% yoy. Services remained the main driver of inflation, contributing +1.44 percentage points to the annual rate, followed by food, alcohol, and tobacco (+0.62pp), and non-energy industrial goods (+0.18pp). Energy remained a drag, subtracting -0.19pp.

For the EU as a whole, CPI was finalized at 2.4%, also unchanged from the previous month. Inflation trends varied sharply across member states. Cyprus (0.0%), France (0.8%), and Italy (1.6%) registered the lowest rates, while Romania (8.5%), Estonia (6.2%), and Croatia (4.6%) recorded the highest. Compared with July, annual inflation fell in nine member states, was stable in four, and rose in fourteen.

UK CPI steady at 3.8% in August, goods prices firm, services ease

Inflation in the UK held steady in August, with CPI unchanged at 3.8% yoy, matching consensus. On the month, prices rose 0.3%. Core CPI, which strips out food, energy, alcohol, and tobacco, eased from 3.8% yoy to 3.6% yoy, a notch below expectations of 3.7% yoy and another sign that underlying pressures are easing gradually.

Goods prices provided an offset, rising from 2.7% yoy to 2.8% yoy, their highest since October 2023. By contrast, services inflation slowed from 5.0% to 4.7%, pointing to softer domestic price dynamics. While still elevated, the services pullback is significant given its importance in shaping medium-term inflation risks.

The BoE meets tomorrow and is expected to hold rates steady, but the August CPI figures will feed into the debate over November’s decision. Softer core and services readings suggest disinflationary progress is intact, leaving policymakers room to consider another rate cut if incoming data on growth and jobs reinforce the trend.

Japan August exports near flat, -13.8% US plunge balanced by other markets

Japan’s trade deficit narrowed in August to JPY -242.5B, smaller than expectations for JPY -513.6B, as exports outperformed forecasts. Overall exports dipped just 0.1% yoy to JPY 8425B, beating projections for a 1.9% yoy decline. Imports, however, fell -5.2% yoy to JPY 8668B, a steeper drop than the -4.2% yoy contraction expected.

The details highlighted stark divergences. Exports to the U.S. tumbled -13.8% yoy, the sharpest fall since February 2021, led by a -28.3% yoy plunge in autos and a -38.9% yoy drop in chipmaking equipment. By contrast, shipments to Asia rose 1.7% yoy, while exports to Western Europe jumped 7.7% yoy. Exports to mainland China slipped 0.5% yoy, though shipments to Hong Kong surged 14.4% yoy.

Australia leading index turns below trend, but RBA to wait until November to cut again

Australia’s Westpac Leading Index growth rate slipped into negative territory in August, falling from 0.11% to -0.16%. It marks the first below-trend reading since September 2024 and a sharp moderation from February’s peak of 0.86%.

Westpac noted the weakness is “not overly concerning” but highlights a “clear softening” from earlier in the year, consistent with the economy slowing after a relatively strong June quarter. It expects growth of 1.9% in 2025, better than the 1.3% expansion in 2024 but still below trend, with a return to trend pace only in 2026.

The RBA meets on September 29–30, where policymakers are almost certain to hold the cash rate steady at 3.6%. Westpac argues that incoming data should eventually validate benign inflation and soft demand, paving the way for a 25bp cut in November, followed by two further cuts in 2026. For now, the RBA will proceed cautiously, watching for confirmation of underlying trends before easing again.

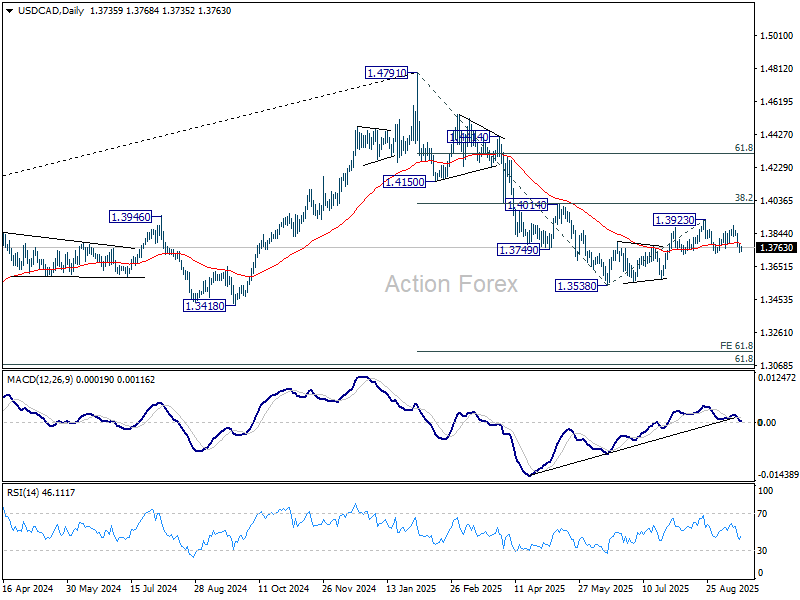

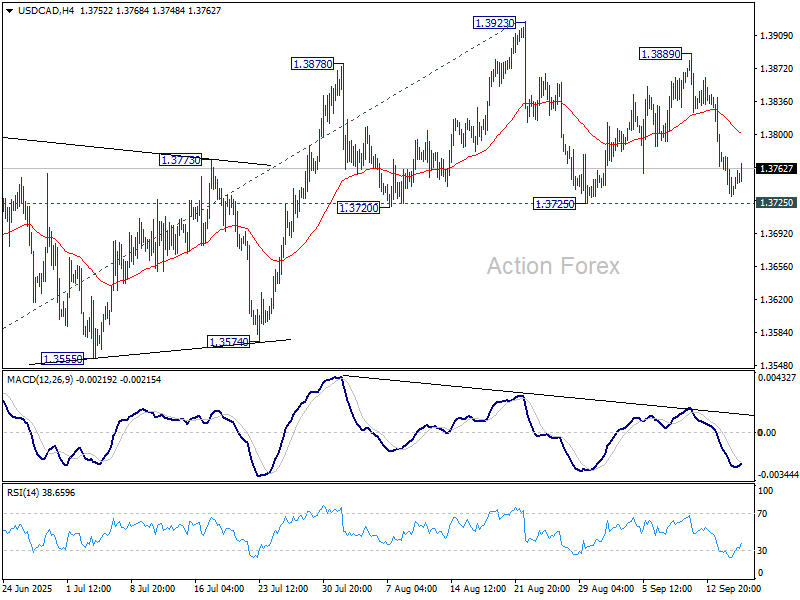

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3721; (P) 1.3752; (R1) 1.3770; More…

Outlook in USD/CAD is unchanged and intraday bias stays neutral. On the downside, firm break of 1.3725 support will complete a head and shoulder top (ls: 1.3878, h: 1.3923, rs: 1.3889). That would indicate that corrective rebound from 1.3538 has already completed, and turn near term outlook bearish. Deeper fall should then be seen to 1.3574 support. On the upside, however, break of 1.3923 will resume the rebound towards 1.4014 cluster resistance.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.