Sterling Holds Ground After BoE, Dollar Loses Momentum – Action Forex

Sterling traded steadily mixed today, showing little reaction to the BoE’s decision to hold rates at 4.00%. The 7–2 vote leaned slightly dovish, with Swati Dhingra and Alan Taylor backing a 25bps cut, but the outcome was broadly expected given their well-established dovish leanings. Importantly, the MPC’s statement flagged that medium-term inflation risks remain “prominent,” sending a clear signal that policymakers are not yet comfortable opening the door to more near-term easing.

For markets, the key question is whether November will deliver a cut. On that, the announcement offered little clarity. Progress in services and core disinflation remains uneven, and policymakers may conclude there is insufficient evidence by November to justify a move.

Another complication is fiscal policy. The UK government is scheduled to present its budget in late November, and some MPC members may prefer to wait until the impact of tax and spending plans is clearer before adjusting interest rates. That raises the risk that a December or early-2026 move may be more likely.

On the broader FX board, Kiwi remains the weakest performer of the week after a sharp GDP miss fueled calls for a 50bps RBNZ cut in October. Dollar is the second weakest, as its post-FOMC bounce shows signs of fading, while Aussie sits third from the bottom after soft jobs data.

By contrast, Swiss Franc leads as the strongest performer, followed by Euro and Loonie. Yen and Sterling sit mid-table, though Yen could slide lower if U.S. and European yields extend their rebound into week’s end.

In Europe, at the time of writng, FTSE is up 0.17%. DAX is up 1.05%. CAC is up 1.04%. UK 10-year yield is up 0.039 at 4.668. Germany 10-year yield is up 0.035 at 2.709. Earlier in Asia, Nikkei rose 1.15%. Hong Kong HSI fell -1.35%. China Shanghai SSE fell -1.15%. Singapore Strait Times fell -0.26%. Japan 10-year JGB yield rose 0.008 to 1.601.

US initial jobless claims fall back to 231k, vs exp 240k

US initial jobless claims fell -33k to 231k in the week ending September 13, below expectation of 240k. Four-week moving average of initial claims fell -750 to 240k. Continuing claims fell -7k to 1920k in the week ending September 6. Four-week moving average of continuing claims fell -10k to 1933k.

BoE holds at 4.00%, two doves dissent,

BoE left its Bank Rate unchanged at 4.00% today, in line with expectations. The decision came with a slight dovish tilt, as two members of the Monetary Policy Committee—Swati Dhingra and Alan Taylor—voted for an immediate 25bps cut. The MPC also voted by 7–2 to continue reducing the stock of UK government bonds held for monetary policy purposes by GBP70 billion over the next 12 months, taking the total down to GBP488 billion.

Policymakers reiterated that a “gradual and careful” approach remains appropriate, with the timing of further easing dependent on the extent of disinflation. The statement stressed that policy is not on a pre-set course and will respond flexibly to new data.

On inflation, the Bank acknowledged progress but kept risks in focus. CPI was steady at 3.8% in August and is expected to edge slightly higher in September before trending back toward the 2% target. Wage growth has slowed from its peak and is expected to decelerate further, while services inflation has held broadly flat. Still, the BoE cautioned that medium-term upside risks remain “prominent.”, particularly if the temporary uptick in CPI feeds into wages and price-setting.

NZ economy shrinks -0.9%, bets of 50bps RBNZ cut rises

New Zealand’s economy contracted far more than expected in Q2, with GDP falling -0.9% qoq against consensus forecasts of -0.3% qoq. The release confirmed a deeper downturn, with economic activity now having declined in three of the last five quarters. The breadth of weakness points to rising headwinds that could force the RBNZ into a more aggressive easing cycle.

Goods-producing industries led the contraction with a -2.3% drop, while primary industries fell -0.7% and services output was flat. “The 0.9 percent fall in economic activity in the June 2025 quarter was broad-based with falls in 10 out of 16 industries,” said economic growth spokesperson Jason Attewell. Manufacturing was the single largest drag, contracting -3.5% in the quarter, while construction fell -1.8% following a modest rebound in Q1.

The scale of contraction triggered a wave of forecasts for deeper RBNZ easing. Westpac now expects a 50bp cut in October followed by a further 25bp reduction in November, compared with earlier projections of 25bp moves at both meetings. That would lower the OCR from the current 3.00% to 2.25% by year-end.

Australia jobs disappoint in August as employment falls -5.4k

Australia’s labor market weakened in August as total employment fell by -5.4k, against expectations for a 21.2k gain. The headline masked stark contrasts, with full-time jobs dropping by -40.9k while part-time roles increased by 35.5k. Hours worked fell -0.4% mom, underscoring signs of cooling demand for labor.

The unemployment rate held steady at 4.2% in line with forecasts, though the participation rate edged down to 66.8% from 67.0%. The data suggest that while unemployment remains low, underlying labor market conditions are softening.

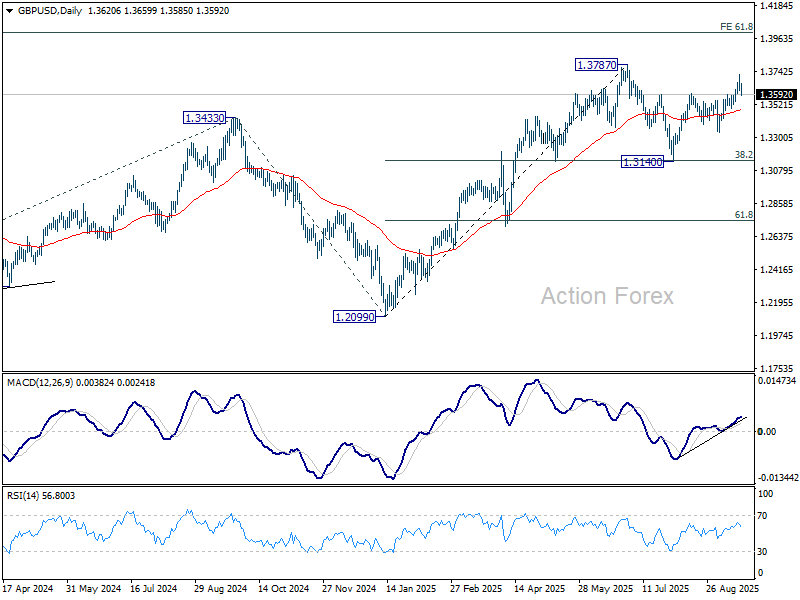

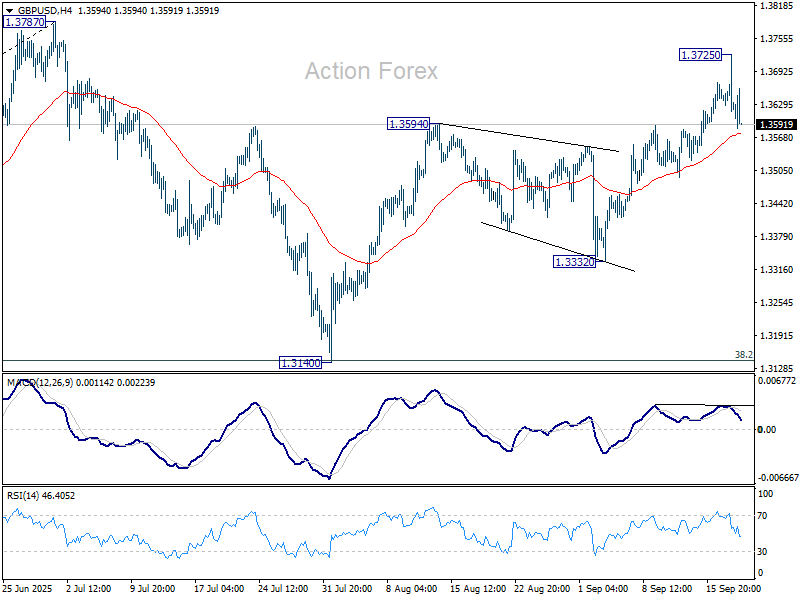

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3588; (P) 1.3657; (R1) 1.3694; More…

Intraday bias in GBP/USD remains neutral and more consolidations could be seen below 1.3725. Further rise is expected as long as 55 D EMA (now at 1.3488) holds. Above 1.3725 will bring retest of 1.3787 high first. Decisive break there will resume larger up trend to 1.4004 projection level. However, sustained break of 55 D EMA will indicate that corrective pattern from 1.3787 is extending with another falling leg, and bring deeper fall to 1.3332 support and below.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3151) holds, even in case of deep pullback.