Yen Leads as BoJ Hawkish Signals Build, Focus Turns to RBA – Action Forex

Yen held firm as the strongest performer heading into the US session, supported by mounting speculation that the BoJ is moving closer to a rate hike. Traders seized on a hawkish shift from a known dove on the Policy Board, a sign that internal momentum is building for further normalization.

This shift in tone from the BoJ was partly balanced by a cautious note from the Japanese government. In its September monthly report, the Cabinet Office kept its basic economic assessment unchanged, describing the recovery as “moderate” while highlighting the drag from US trade policies, particularly in the automotive sector. Officials also warned that attention should remain on downside risks linked to external headwinds.

Still, the currency’s next major driver will be global risk sentiment. Heavyweight US releases this week — highlighted by Friday’s non-farm payrolls — will be decisive for both stocks, bonds and currencies. Any data surprise strong enough to sway Fed expectations will inevitably spill over into USD/JPY and broader Yen crosses.

In the upcoming Asian session, attention is shifting to the RBA’s policy decision. The RBA is expected to keep rates on hold at 3.60%, but the outcome carries added weight after August CPI accelerated to 3.0% from 2.8%. While consensus sees a year-end rate of 3.35%, a handful of analysts have delayed their calls for a November cut in light of the firmer inflation print.

Australia’s largest banks are split: ANZ, CBA, and Westpac forecast a 25bps reduction in November, while NAB expects no easing until May. A Reuters poll found more than 80% of respondents still see a cut to 3.35% by year-end, though the number expecting no change has risen since August.

For the day so far, Dollar is the weakest major currency, followed by Swiss Franc and Loonie. Yen sits at the top of the ladder, ahead of Sterling and Aussie, with the Kiwi and Euro trading in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.54%. DAX is up 0.02%. CAC is up 0.26%. UK 10-year yield is down -0.038 at 4.72. Germany 10-year yield is down -0.023 at 2.731. Earlier in Asia, Nikkei fell -0.69%. Hong Kong HSI rose 1.89%. China Shanghai SSE rose 0.90%. Singapore Strait Times rose 0.09%. Japan 10-year JGB yield fell -0.013 to 1.647.

Eurozone economic sentiment inches higher to 95.5, jobs outlook softer

Economic sentiment in the Eurozone improved slightly in September, with the Economic Sentiment Indicator rising 0.2 points to 95.5. The broader EU also gained 0.6 points to the same level. Despite the uptick, sentiment remains below the long-term average of 100.

The modest gains were driven by stronger confidence in industry, services, and among consumers, offset partly by weaker retail sentiment and stable conditions in construction.

By contrast, labor market expectations slipped, with the Employment Expectations Indicator dropping -0.9 points in the EU and -1.3 points in the euro area, suggesting hiring momentum is fading.

Country-level trends were uneven. Spain led with a notable 3-point jump, followed by Italy (+0.7), while sentiment weakened in the Netherlands (-0.7) and Germany (-0.4). France (+0.3) and Poland (+0.1) saw little change.

BoJ dove Noguchi signals hawkish shift

BoJ board member Asahi Noguchi, long seen as one of the most dovish voices on the Board, struck a notably hawkish tone today. He argued that Japan is making steady progress toward its 2% inflation goal, citing stronger wage momentum and greater corporate willingness to pass on rising costs.

Noguchi said the “need to adjust the policy interest rate is increasing more than ever,” highlighting that upside risks to prices and growth now outweigh the downside. He noted the labor market is “close to full employment” and the output gap has “almost reached zero”, warranting a shift in policy perspective to address rising inflation risks.

His comments mark a significant departure from his usual stance, adding to expectations that the BoJ could deliver another rate hike in the near future. Noguchi did caution that U.S. tariffs remain a source of downside risk, but the overall message suggests growing consensus within the Board for normalization.

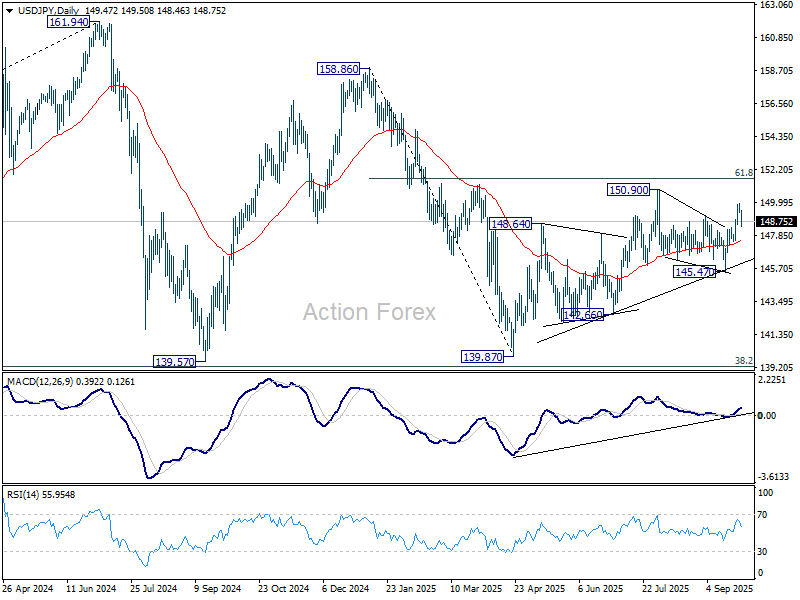

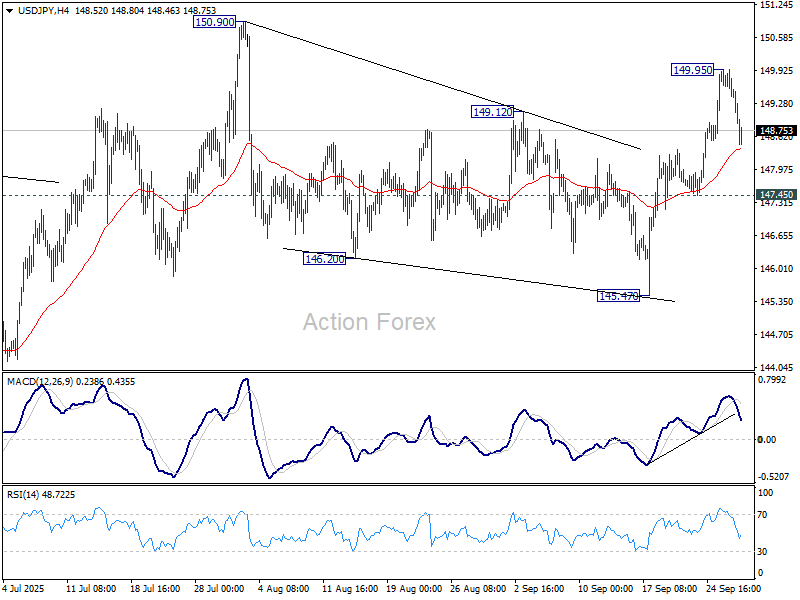

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.28; (P) 149.62; (R1) 149.83; More…

Intraday bias in USD/JPY stays neutral for the moment and some more consolidations could be seen below 149.95 temporary top. Further rally is expected as long as 147.45 support holds. Corrective pattern from 150.90 should have completed at 145.47. Above 149.95 will bring retest of 150.90 first. Firm break there will target 151.22 fibonacci level. However, sustained break of 147.45 will dampen this bullish view and bring deeper fall back to 145.47 support instead.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.