Aussie Surges on RBA Hawkish Tilt, Yen Supported Despite Data Weakness – Action Forex

Aussie rallied broadly after the RBA left policy unchanged at 3.60% but issued a statement that leaned hawkish. Traders were quick to note the Bank’s warning that Q3 inflation may come in stronger than projected in August, a reminder that the disinflation path remains far from assured.

The RBA’s tone suggested that the widely expected November cut is far from a done deal. Policymakers appear keen to leave flexibility in case inflation surprises higher, especially if robust consumption and firm labour markets give businesses scope to pass on costs. More importantly, scope for a deeper easing cycle is now more limited than markets had assumed. Even if the RBA delivers one cut in November, follow-up moves may prove difficult.

Meanwhile, Yen also stayed firm, supported by the BoJ’s Summary of Opinions, which revealed growing calls for rate hikes within the board. A number of board members argued that the time for action may be near, adding momentum to expectations of policy normalization.

Yet Japanese data continue to cast doubt on how soon that shift can occur. Industrial production contracted more than expected in August, and retail sales posted their first drop in 42 months. For now, the majority of the Board remains cautious, waiting for more evidence before endorsing a move.

Doves remain in the majority in the BoJ for now, and there is little hard evidence yet to tip the balance decisively toward an imminent hike. The next test will be the quarterly Tankan survey due tomorrow, which will provide a clearer read on business sentiment and capital expenditure plans.

In terms of weekly performance, Aussie is leading the pack for now, followed by Yen and Kiwi. Dollar sits at the bottom, trailed by Swiss Franc and Euro, while Sterling and the Loonie are holding in the middle of the field.

Elsewhere, Asian equities traded mixed after Wall Street’s modestly higher close overnight. Quarter-end lull and caution ahead of key US data — notably ISM Manufacturing tomorrow and non-farm payrolls on Friday — are keeping traders restrained, ensuring a steady but cautious tone across markets.

In Asia, at the time of writing, Nikkei is up 0.01%. Hong Kong HSI is down -0.13%. China Shanghai SSE is up 0.40%. Singapore Strait Times is up 0.40%. Japan 10-year JGB yield is down -0.013 at 1.634. Overnight, DOW rose 0.15%. S&P 500 rose 0.26%. NASDAQ rose 0.48%. 10-year yield fell -0.046 to 4.140.

RBA holds steady at 3.60%, warns Q3 inflation may surprise on upside

The RBA left its cash rate unchanged at 3.60% in a unanimous decision, in line with expectations. The move reflects the Board’s preference to pause while monitoring whether recent economic surprises point to a more persistent inflation challenge.

According to the RBA, recent partial data suggest that September-quarter inflation may come in above projections made in August. At the same time, labor market indicators show conditions have been steady and remain “a little tight”, reinforcing the risk that price pressures may not ease as quickly as anticipated.

The Bank outlined two contrasting scenarios for household demand. Stronger consumption may reflect rising real incomes and wealth, potentially allowing firms to raise prices more easily and encouraging further hiring. Alternatively, this consumption rebound may not last if households turn more cautious amid uncertainty around overseas developments.

BoJ summary reveals rising hawkish pressure, but board still divided

The BoJ’s September Summary of Opinions revealed that members debated the feasibility of raising interest rates in the near term, with some arguing that conditions were aligning for another move. The release underscores a growing hawkish tilt inside the Board, even as the majority voted to hold steady at 0.50%.

One member argued that “judging solely from the perspective of Japan’s economic conditions, it may be time to consider raising the policy interest rate again,” noting that more than six months have passed since the last hike. Another highlighted easing concerns from U.S. tariffs, suggesting external impact on inflation had “abated” and that the BoJ could “return to its stance to raise the policy interest rate.”

At the same time, caution was evident. Some warned against surprising markets with a hike, stressing that Japan’s domestic demand remains vulnerable to external shocks. The view was that it would be better to wait for more hard data before making another adjustment.

At the September 18–19 meeting, the BoJ left rates at 0.50%, though two members dissented in favor of a hike to 0.75%.

Japan’s industrial output falls -1.2% mom in August, retail sales contracts

Japan’s latest data painted a downbeat picture of economic momentum in August. Industrial production slipped -1.2% mom, falling short of the expected -0.8%. Of the 15 industrial sectors, 12 including metal products, and inorganic and organic chemicals, saw output decreases.

METI maintained its description of output as “fluctuates indecisively”. Officials stressed that firms remain highly cautious in their production planning. Still, manufacturers surveyed see output rising 4.1% in September and another 1.2% in October.

Household demand faltered at the same time, with retail sales tumbling -1.1% yoy, marking the first decline in 42 months.

China’s NBS PMI points to easing manufacturing weakness, services soft patch

China’s official PMI data for September signaled tentative improvement in industry but lingering softness in services. The NBS Manufacturing PMI rose to 49.8 from 49.4, its highest since March, though it still pointed to contraction. The gauge has been under 50 since April, reflecting headwinds for large and state-linked producers.

The NBS Non-Manufacturing PMI slipped from 50.3 to 50.0, effectively flatlining and pointing to a loss of momentum in construction and services. That stagnation raises questions about the strength of domestic demand, even as authorities step up stimulus efforts.

In contrast, the RatingDog (S&P Global) surveys offered a more optimistic take. Manufacturing improved to 51.2 from 50.5, the strongest since May, suggesting that private and export-focused companies are benefiting from external demand. Services edged down slightly from 53.0 to 52.9 but remained firmly in growth territory.

NZ ANZ business confidence ticks down, but activity outlook improves

New Zealand’s ANZ Business Confidence edged slightly lower in September, slipping from 49.7 to 49.6. Though, Own Activity Outlook improved to 43.4 from 38.7.

Inflation pressures ticked mildly higher. One-year-ahead inflation expectations rose to 2.71% from 2.63%,. The share of firms expecting to raise prices in the next three months climbed to 46%. Cost expectations also edged up, with 75% of respondents seeing higher input costs.

ANZ noted that the RBNZ is positioned to support growth with a lower Official Cash Rate. While the exact path of policy easing remains uncertain, the bank said the OCR will ultimately reach the level required to ensure the recovery takes hold.

Fed’s Williams: Makes sense to ease policy a little bit to support jobs

New York Fed President John Williams said overnight that it made sense for the central bank to ease policy “a little bit” to reduce restrictiveness to support the labor market while maintaining downward pressure on inflation.

Williams acknowledged progress toward the 2% inflation target but cautioned that more work remains. He underscored the Fed’s dual mandate, stressing the need to avoid “undue harm” to employment at a time when job creation has been gradually weakening. “I don’t want to see that go too far,” he said.

Encouragingly, Williams noted that some inflation worries have eased “”The tariff effects have been smaller than most people thought, and there doesn’t seem to be any signs of inflationary pressures building,” he noted.

Fed’s Musalem open to cuts but urges cautions

St. Louis Fed President Alberto Musalem said monetary policy is now “somewhere between modestly restrictive and neutral.”

Musalem, who votes on policy this year, said he is “open minded” to further rate cuts but stressed that caution is needed. With limited room before policy turns “overly accommodative”, he signaled the Fed should proceed carefully.

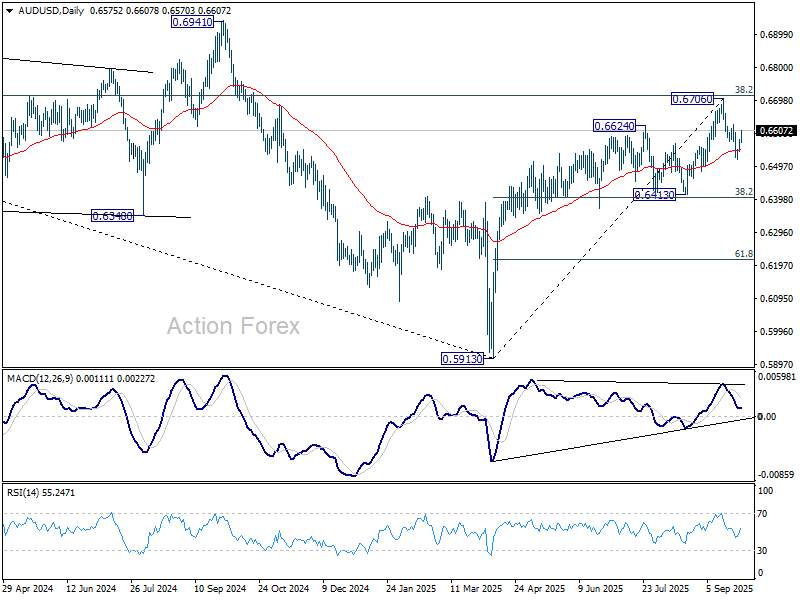

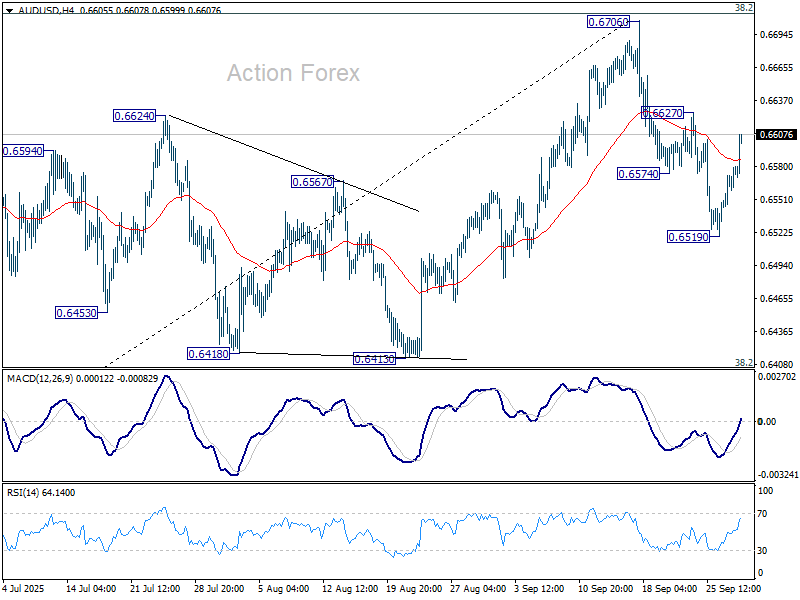

AUD/USD Daily Report

Daily Pivots: (S1) 0.6555; (P) 0.6568; (R1) 0.6589; More...

Focus is back on 0.6627 resistance in AUD/USD with current extended rebound. Break there will suggest that pullback from 0.6706 has completed as correction, after drawing support from 55 D EMA (now at 0.6546). That will keep the larger rally from 0.5913 alive and bring retest of 0.6706 high. However, on the downside, sustained trading below 55 D EMA will confirm rejection by 0.6713 fibonacci resistance, and bring deeper fall to 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403).

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.