Yen Momentum Slows After Slide, But Japan Bond Market Faces Takaichi Test – Action Forex

Volatility across major currency pairs eased in Asian session today, with markets showing a brief pause after several sessions of outsized moves. Yen initially extended losses as the Nikkei 225 surged to another record high for a second straight day, but later steadied as profit-taking emerged following the sharp depreciation seen earlier in the week.

While the short-term selling momentum in the Yen appears to have cooled, there is no sign of a firm bottom yet. Renewed weakness could resume at any time, especially if risk appetite stays elevated. The broader tone remains fragile, with positioning still heavily tilted against the currency.

In fixed income markets, the 10-year Japanese government bond yield jumped to its highest level since July 2008, edging close to the 1.7% mark. The move signals renewed stress in Japan’s long-dormant bond market, long insulated by the BoJ’s yield curve control framework and decades of deflationary pressure.

Markets are now adjusting to the prospect of a new political era under Sanae Takaichi, who is expected to become Japan’s first female prime minister after winning the ruling Liberal Democratic Party’s leadership race on Saturday. Takaichi is expected to be confirmed by parliament on October 15.

Meanwhile, expectations for an October BoJ rate hike have faded. Market-implied odds have fallen sharply after the leadership change, with Deutsche Bank reportedly exiting its long-Yen positions, citing uncertainty around Takaichi’s policy priorities and the timing of the BoJ’s hiking cycle. The shift reinforces speculation that the central bank will remain cautious and maintain its current settings through year-end.

Meanwhile, Euro also remained soft, weighed by renewed political instability in France. President Emmanuel Macron was hit by another crisis following the shock resignation of Prime Minister Sebastien Lecornu after just 27 days in office — the shortest-lived government in modern French history. Macron now faces mounting calls to resign, appointing a new government, or dissolving parliament for early elections, as opposition pressure intensifies.

Across the week so far, Aussie leads gains, followed by Dollar and Loonie. Yen remains the weakest performer, trailed by Euro. Sterling, Swiss Franc, and Kiwi trade mixed in the middle.

In Asia, at the time of writing, Nikkei is up 0.10%. Hong Kong and China are on holidays. Singapore Strait Times is up 0.95%. Japan 10-year JGB yield is down -0.006 at 1.674. Overnight, DOW fell -0.14%. S&P 500 rose 0.36% NASDAQ rose 0.71%. 10-year yield rose 0.043 to 4.162.

ECB’s Lagarde: Disinflation over, range of risks narrow

ECB President Christine Lagarde told a European Parliament’s committee that the Eurozone’s “disinflationary process is over”, with inflation now hovering around 2% and expected to remain near target over the medium term. She said this backdrop justified the Governing Council’s recent decision to keep interest rates unchanged.

Lagarde noted that risks to economic growth have become “more balanced”, as the likelihood of severe tariff-related downside shocks has eased following the trade deal. Still, she warned that renewed trade tensions could weigh on exports, investment, and consumption, while persistent geopolitical uncertainty continues to cloud the outlook for both growth and prices. On the positive side, Lagarde highlighted that higher defence and infrastructure spending and productivity-boosting reforms could support growth momentum ahead.

She also emphasized that the inflation outlook remains “more uncertain than usual”, reflecting the “still volatile global trade policy environment” that poses both upside and downside risks. However, she added that the “range of risks on both sides has narrowed” as new data arrives.

Her comments are interpreted as confirmation that the ECB remains firmly on hold, awaiting clearer signals before considering any recalibration of its policy stance.

Fed’s Schmid warns inflation broadening, despite muted tariff effects

At an event overnight, Kansas City Fed President Jeff Schmid warned that price increases have become “more widespread”, with 80% of inflation categories rising, compared with 70% earlier this year. He called the trend “worrying,” indicating that underlying inflation pressures remain entrenched.

Schmid said he sees a “relatively muted effect” from tariffs on inflation, but viewed that as a signal that monetary policy is well positioned, not as evidence to justify “aggressively lowering” rates.

He added that the Fed faces difficult trade-offs between its dual mandates but insisted it “must maintain its credibility on inflation”.

Australia Westpac consumer sentiment slumps to firmly pessimistic level, RBA November cut not assured

Australian consumer sentiment dropped -3.5% mom to 92.1 in October, according to the Westpac-Melbourne Institute survey, erasing all gains seen between May and August when rate cuts briefly lifted confidence. The index has returned to “firmly pessimistic” territory, signaling renewed caution among households.

Westpac said consumers were unsettled by recent inflation updates, with partial indicators suggesting annual price growth has edged back toward the top of the RBA’s 2–3% target range. Signs of stronger consumer demand and a reviving housing market have also stoked speculation that the RBA may not ease policy as quickly as previously expected.

With the RBA meeting scheduled for November 3–4, Westpac noted that a rate cut is “far from assured, though not off the table.” The bank added that the longer the RBA holds off on further easing, the greater the likelihood of deeper cuts later.

NZIER sees two more RBNZ cuts despite signs of inflation pick-up

The New Zealand Institute of Economic Research maintained its forecast for two additional 25bps cuts by the RBNZ at the October and November meetings, despite a mild uptick in inflation pressures during Q3.

In its latest Quarterly Survey of Business Opinion (QSBO), NZIER said a net 11% of firms raised prices, compared with 1% reporting price cuts in the previous quarter, suggesting that cost pressures are firming again. NZIER expects annual CPI inflation to rise slightly above 3% in the near term but sees it drifting back toward the 2% midpoint of the RBNZ’s target range as excess capacity continues to weigh on domestic demand.

Business sentiment, however, softened, with 15% of firms expecting economic improvement, down from 26% in Q2, while 14% reported weaker trading activity in their own businesses. The survey also pointed to declining hiring and investment intentions, as 23% of firms cut staff and a majority plan to reduce capital spending over the coming year.

The mixed picture—firmer inflation but softer demand—supports NZIER’s view that the RBNZ will deliver further easing to stabilize growth, even as it remains alert to temporary inflation volatility.

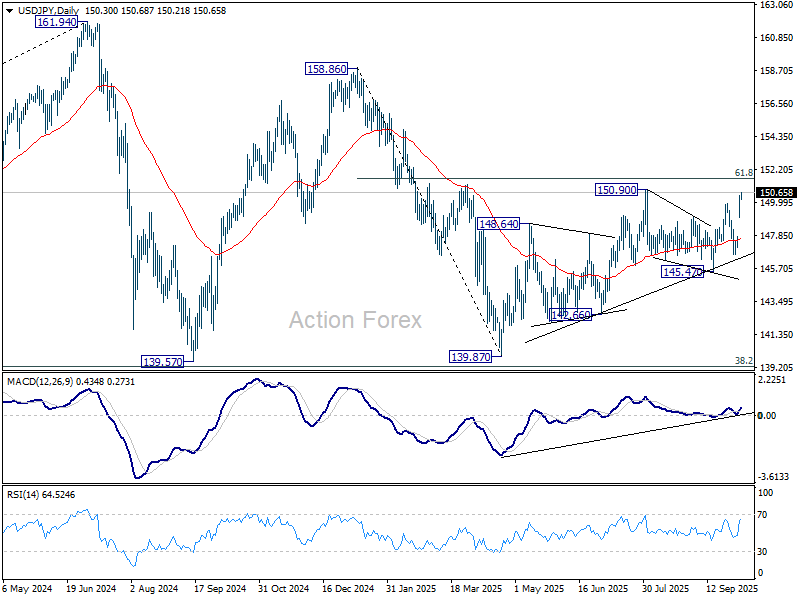

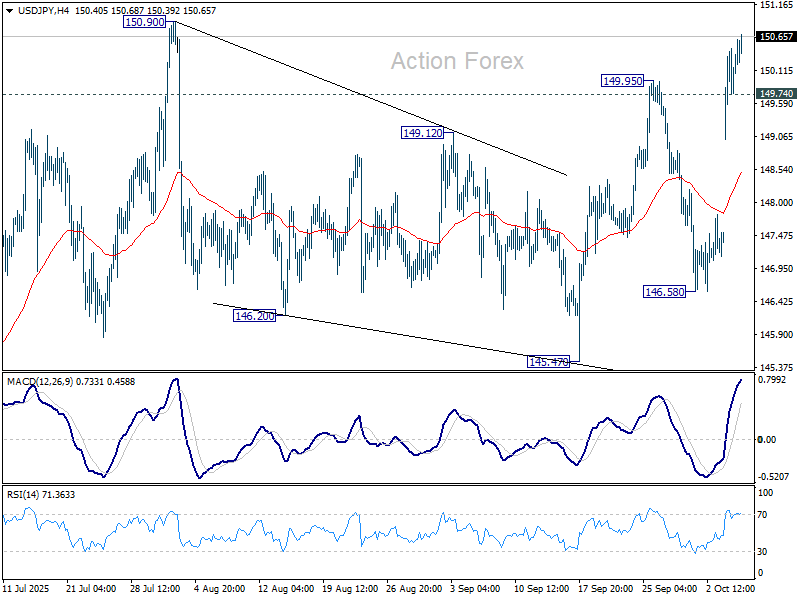

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.45; (P) 149.97; (R1) 150.88; More…

Intraday bias in USD/JPY remains on the upside at this point. Break of 150.90 will resume larger rally from 139.87 to 151.22 fibonacci level. Sustained break there will carry larger bullish implication. On the downside, below 149.74 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.