U.S.–China War of Words Jolts Asia, Yet U.S. Futures Signal Contained Fallout – Action Forex

Asian equities started the week sharply lower after renewed flare-up in U.S.–China trade tensions, though signs from U.S. futures suggested that sentiment hadn’t worsened materially beyond last Friday’s selloff. Hong Kong’s Hang Seng Index slumped nearly -3.5% by midday, leading regional loss. The declines came after Beijing recently tightened export controls on rare earth minerals, prompting US President Donald Trump to retaliate with a threat of 100% tariffs on all Chinese imports starting November 1.

China’s Ministry of Commerce struck a combative tone over the weekend, saying the country was “not afraid of” a trade war and accusing Washington of a “textbook double standard.” The tit-for-tat rhetoric revived fears of a deeper standoff between the world’s two largest economies, though investors were quick to note that the broader risk mood had not deteriorated further. U.S. stock futures traded higher, signaling that Wall Street was stabilizing after last week’s sharp drop and that the Asian session was largely a delayed reaction rather than fresh panic selling.

Trump appeared to soften his stance on Sunday, posting online that “Don’t worry about China, it will all be fine!” and calling President Xi “highly respected.” He added that neither side wanted a depression, emphasizing that “the U.S.A. wants to help China, not hurt it.” The conciliatory tone contrasted sharply with his tariff threat days earlier and helped reassure investors that negotiations remain possible.

Vice President JD Vance echoed this calibrated approach in an interview with Fox News, saying the U.S. “will negotiate if Beijing is willing to be reasonable,” while reminding that Washington still “holds more cards.” Together, their remarks were interpreted as an attempt to de-escalate market fears without undermining the U.S. negotiating position.

Some observers see this exchange as part of a tactical phase rather than a reversion to the full-scale trade war. Both sides appear to be hardening their rhetoric strategically ahead of a potential Trump–Xi meeting at the APEC summit in South Korea later this month. Such posturing allows both governments to project strength domestically, and is more about negotiation leverage than policy action. For now, traders are watching for signs of follow-through, but few expect immediate disruption to trade flows.

In currencies, risk sentiment remained mixed but orderly. Aussie led gains for the day so far, followed by Kiwi and Loonie. Yen and Swiss Franc weakened while Euro dipped modestly. Sterling and Dollar traded mid-range. Overall, the currency markets are signaling unease, but not alarm.

In Asia, Japan is on holiday. At the time of writing, Hong Kong HSI is down -3.49%. China Shanghai SSE is down -1.17%. Singapore Strait Times is down -1.19%.

China trade in September, exports and imports surge, surplus narrows

China’s trade figures for September delivered a mixed picture. Exports rose 8.3% yoy, well above forecasts of 6.0% and marking the fastest pace in six months. Imports jumped 7.4% yoy, the strongest gain since April 2024 and far exceeding expectations of 1.5%.

However, the details showed signs of strain beneath the surface. Exports of rare earths—a key strategic material—fell -30.9% from August to 4,000 tonnes, the lowest level since February, amid tighter export restrictions. Meanwhile, soybean imports surged to the second-highest level on record, boosted by heavy purchases from South America as buyers avoided U.S. supplies in response to the escalating trade conflict.

Overall, China’s trade surplus narrowed to USD 90.5B from USD 102.3B, undershooting expectations of USD 98.5B. The surplus with the U.S. widened to USD 22.8B, even as total bilateral trade continued to shrink—exports to the U.S. fell nearly -17% in the first three quarters, while imports declined -11.6%. At the same time, trade deficit with Russia expanded to its widest level in six months at USD 2.1B.

NZ BNZ services at 48.3, contracts for 19th month as signs of strain persist

New Zealand’s services sector remained mired in contraction in September, with BNZ Performance of Services Index edging up modestly from 47.6 to 48.3. While the improvement marks a slight lift in momentum, the index has now stayed below the 50-point expansion threshold for 19 consecutive months.

Activity and sales rose to 47.8, and new orders improved to 49.6, but both remained in negative territory. Employment slipped to 47.8, reflecting ongoing caution among firms facing soft sales and squeezed margins.

BNZ reported that 58% of survey comments were negative, only marginally below August’s 59.6%. Respondents cited weak consumer confidence, rising living costs, and reduced discretionary spending as key drags. Many businesses also noted clients delaying projects and contracts amid broader economic uncertainty.

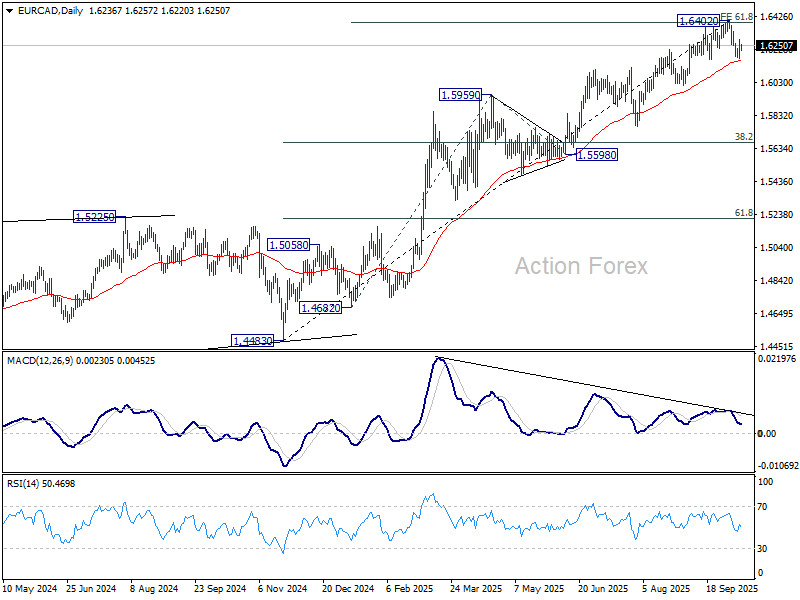

EUR/CAD: Euro pullback and Loonie resilience could amplify downside risks

Canadian Dollar is holding its ground as one of the month’s best-performing currencies so far, supported by surprisingly strong domestic data despite a slump in oil prices. WTI crude’s drop through 60 last week would normally pressure the Loonie, but September’s upbeat employment figures more than offset that drag.

The standout feature of the report was rebound in manufacturing jobs — the sector’s first monthly gain since January — signaling renewed momentum in an area hard-hit by global trade tensions. The improvement was particularly welcome after a weak summer stretch that had driven the BoC’s 25bps rate cut in September.

Markets are now looking to the October 21 CPI report for confirmation. Inflation would probably need to print well below expectations to confirm the case for another cut on October 29. For now, the data flow leans toward a pause.

Technically, EUR/CAD shows early signs of exhaustion after meeting upside target of 61.8% projection 1.4682 to 1.5959 from 1.5598 at 1.6387. Visible bearish divergence on D MACD reinforces the case that upward momentum is fading.

Sustained break below the 55 D EMA (now at 1.6160) should indicate medium term topping at 1.6402. Deeper decline could then be seen to correct whole five-wave rally from 1.4483 (Nov 2024 low), and target 38.2% retracement of 1.4483 to 1.6402 at 1.5669. Nevertheless, strong bounce from 55 D EMA will retain near term bullishness and set up another rally through 1.6402 instead.

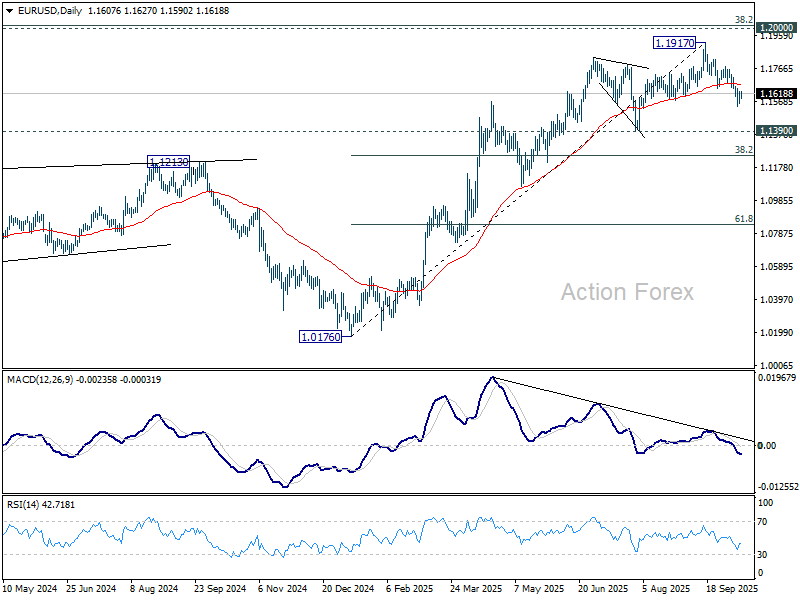

Also, it should be noted that cross-currency dynamics point to growing downside risk for EUR/CAD. EUR/USD has failed to break through the key 1.2000 cluster resistance and has since retreated from 1.1917. Deeper pullback or even a shift toward bearish reversal could be underway.

At the same time, USD/CAD is testing strong cluster resistance near 1.4000, where a corrective dip appears likely after months of steady advance.

Should both patterns materialize—Euro weakening against Dollar while Loonie strengthens versus the Greenback—EUR/CAD would accelerate its decline, reinforcing the view that a medium-term top is in place. However, sustained strength in USD/CAD or stabilization in EUR/USD would shift the odds away from this bearish case in EUR/CAD.

UK and Australia take focus as shutdown delays U.S. CPI

It’s set to be a relatively quiet week in terms of data releases. The US calendar is near empty due to ongoing government shutdown. The most notable casualty is September’s CPI report, originally slated for Wednesday, which is now postponed. It’s reported that the Bureau of Labor Statistics confirmed that it will “promptly resume” work, with CPI now scheduled for October 24 — nine days later than planned. The timing ensures the Fed will have the data in hand ahead of its October 28–29 policy meeting.

In the UK, labor market and GDP readings will be the main event. Speculation has already grown that the BoE’s easing cycle may be near its end, with policymakers keen to avoid reigniting inflationary pressures amid still-firm labor costs. Stronger wages or activity data this week would strengthen the case for the BoE to hold policy steady in November.

In the Asia-Pacific region, attention turns to Australia, where the RBA’s meeting minutes and September employment report will be closely watched. The November policy meeting remains live, with markets divided over whether another rate cut is warranted. The labor figures will be pivotal in shaping that debate, as resilient household spending has so far kept the RBA cautious about over-stimulating demand. The RBA’s minutes may offer some color on the internal balance of views but are unlikely to reveal new signals ahead of the more decisive Q3 CPI report later this month.

Here are some highlights for the week:

- Monday: New Zealand BNZ services index; China trade balance.

- Tuesday: RBA minutes, NAB business confidence; UK employment; Swiss PPI; German ZEW economic sentiment, CPI final; US NFIB small business index; Canada building permits.

- Wednesday: China CPI, PPI; Eurozone industrial production; Canada manufacturing sales, wholesale sales; US Empire state manufacturing, Fed’s Beige Book.

- Thursday: Japan machine orders; Australia employment; Japan tertiary industry index; UK GDP, trade balance; Swiss SECO economic forecasts; Eurozone trade balance; US Philly Fed survey, NAHB housing index.

- Friday: Eurozone CPI final.

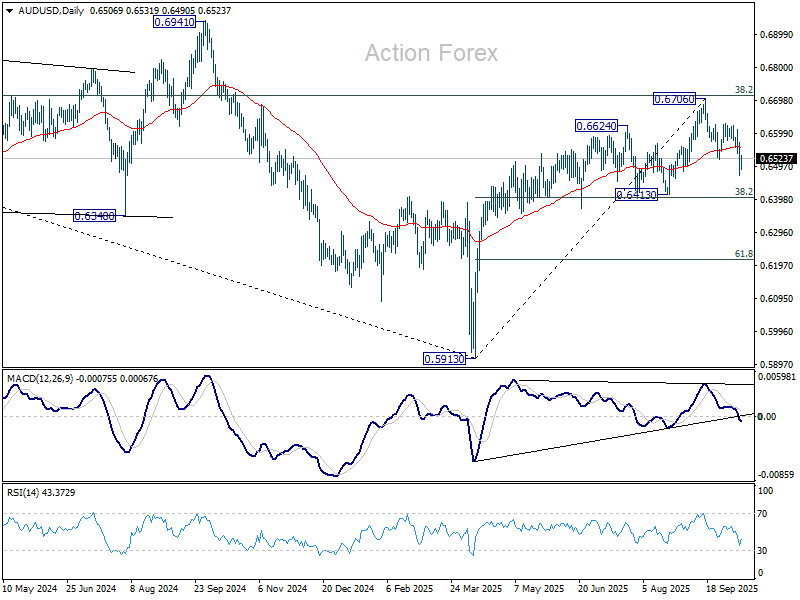

AUD/USD Daily Report

Daily Pivots: (S1) 0.6442; (P) 0.6508; (R1) 0.6542; More...

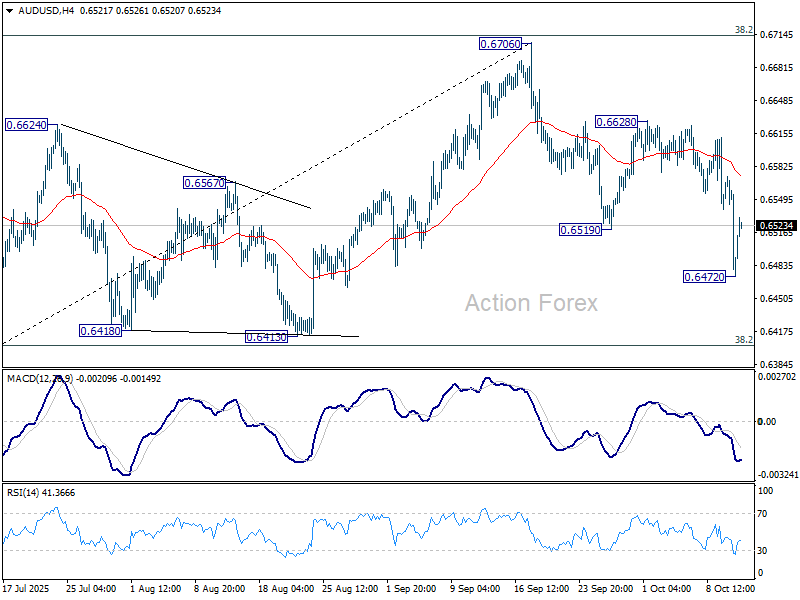

AUD/USD recovered notably today and intraday bias is turned neutral first. Still, risk will remain on the downside as long as 0.6628 resistance holds. Current development suggests rejection by 0.6713 fibonacci resistance. Below 0.6472 will resume the fall from 0.6706 to 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403).

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.