Safe Havens Surge as Market Nerves Deepen Ahead of Weekend – Action Forex

Safe-haven demand is dominating global markets as traders head into the final trading day of the week. Gold has surged past 4,300 mark to a new record high, putting it on track for its best weekly performance in five years, while the Swiss Franc is rallying sharply across the board. The flight to safety reflects deepening concerns about financial stability and the global outlook as investors seek shelter from mounting geopolitical and economic uncertainty.

The latest catalyst came from a renewed wave of anxiety over the U.S. regional banking sector, after a string of lenders disclosed rising bad loans. The headlines have revived memories of the mini banking crisis in 2023, which began with the collapse of Silicon Valley Bank, followed soon after by Signature Bank and First Republic Bank. The unease comes just as markets grapple with a series of unresolved macro risks that continue to weigh on sentiment.

Among those, U.S.–China trade tensions remain front and center, with no visible progress toward de-escalation before the November 1 deadline for 100% tariffs. Both sides have hardened their rhetoric, leaving investors uncertain about whether negotiations will resume or break down completely. The lack of clarity is amplifying volatility across equities and commodities, while reinforcing demand for traditional safe havens.

Adding to the fog, the U.S. government shutdown continues with no resolution in sight, delaying key economic data releases and leaving policymakers and investors without a reliable read on the economy—especially on the labor market. The blackout has made it harder for traders to assess whether growth is holding up or slipping, further encouraging defensive positioning in the absence of clear signals.

For the week so far, Swiss Franc leads as the strongest major currency, rebounding after a brief pullback yesterday. Euro and Yen also gained on safe-haven flows. Loonie lags behind, hit by weaker risk appetite and falling oil prices. Dollar, Aussie, and Kiwi are also under pressure, with Sterling trading mid-pack. Sentiment is not yet in freefall, but with nerves running high and multiple risks unresolved, markets are increasingly vulnerable to a sharper turn south.

In Asia, at the time of writing, Nikkei is down -1.58%. Hong Kong HSI is down -1.84%. China Shanghai SSE is down -1.27%. Singapore Strait Times is down -0.55%. Japan 10-year JGB yield is down -0.033 at 1.624. Overnight, DOW fell -0.65%. S&P fell -0.63%. NASDAQ fell -0.47%. 10-year yield fell -0.070 to 3.976.

US 10-year yield breaks 4% on bank fears, watch 3.9% as market stress builds

U.S. 10-year Treasury yield tumbled decisively below the 4.00% mark overnight, hitting its lowest level since April and flashing renewed signs of market stress. The next key support lies at around 3.9%, where some stabilization should occur. However, decisive break below 3.9% would be a serious warning signal that could trigger an accelerated decline toward 3.70%, signaling a sharp escalation in risk aversion.

The sharp drop was driven by flight to safety following unsettling developments in the U.S. regional banking sector. Shares of Zions Bancorporation and Western Alliance plunged after both lenders revealed unexpected bad loans, igniting fears of loose credit standards and potential contagion across smaller financial institutions. The news came on the heels of two recent auto industry-related bankruptcies, which have amplified concerns about tightening credit conditions and balance sheet vulnerabilities.

Markets now turn to Friday’s wave of regional bank earnings, seen as the next test of sector stability. Investors will be watching closely to gauge whether the problem is contained or spreading. A weak showing could deepen risk aversion and accelerate the rush into Treasuries, further suppressing yields.

Technically, 10-year yield’s fall from the recent peak of 4.629 resumed with conviction after breaking below 3.992 support. Next near term target lies at 61.8% projection of 4.493 to 4.205 from 4.200 at 3.891. Some stabilization should emerge there, at least on the first attempt.

However, decisive break below 3.891 would raise the risk of a deeper slide toward 100% projection at 3.699. A bounce from the 3.900 area could still restore some calm — but failure to hold that line risks triggering a deeper wave of safe-haven buying across the Treasury curve.

Fed’s Kashkari sees inflation as stubborn but not dangerous

Minneapolis Fed President Neel Kashkari said overnight that the balance of risks in the U.S. economy has shifted, with greater danger of a labor market slowdown than of a sharp rebound in inflation. Neveretheless, he added that while policymakers may be leaning toward the view that the economy is weakening, “we’re more likely betting that the economy is really slowing more than it really is.”

Kashkari downplayed fears of inflation reaccelerating to 4% or 5%, noting that the arithmetic of tariff effects does not support such a scenario. Instead, he described the main concern as “persistence”, with price pressures potentially staying near 3% for “an extended period” rather than spiking.

He also addressed the impact of the ongoing government shutdown, saying that while the lack of official data complicates decision-making, Fed officials still have access to timely private indicators and feedback from business outreach.

“We can make our way through while the shutdown is happening,” Kashkari said. “But the longer it goes on, the less confidence I have that we are reading the economy appropriately.”

ECB’s Lagarde: Well positioned to weather future shocks

Speaking at an IMF event, ECB President Christine Lagarde said the Eurozone economy has reached a point of relative stability, with inflation now close to the ECB’s 2% goal. “We are in a good place, and we are well positioned to face future shocks,” she said.

Lagarde cautioned, however, that several unpredictable risks remain on the horizon, from trade-related frictions to the continuing conflict in Ukraine. She said that while uncertainty is still elevated, some feared disruptions “were not as bad as we had anticipated.”

Ueda signals watchful patience as BoJ weighs October policy options

BoJ Governor Kazuo Ueda reiterated overnight that the central bank will consider rate hikes “if our confidence in hitting the outlook increases”. He added that he intends to continue gathering informations before making any decisions at the October 29–30 policy meeting.

Ueda observed that G20 members regard the world economy as broadly stable but facing persistent risks, from trade disputes to geopolitical frictions. “Many institutions and observers still factor them into their outlooks, or at least treat them as downside risks when assessing the global and U.S. economies,” he said.

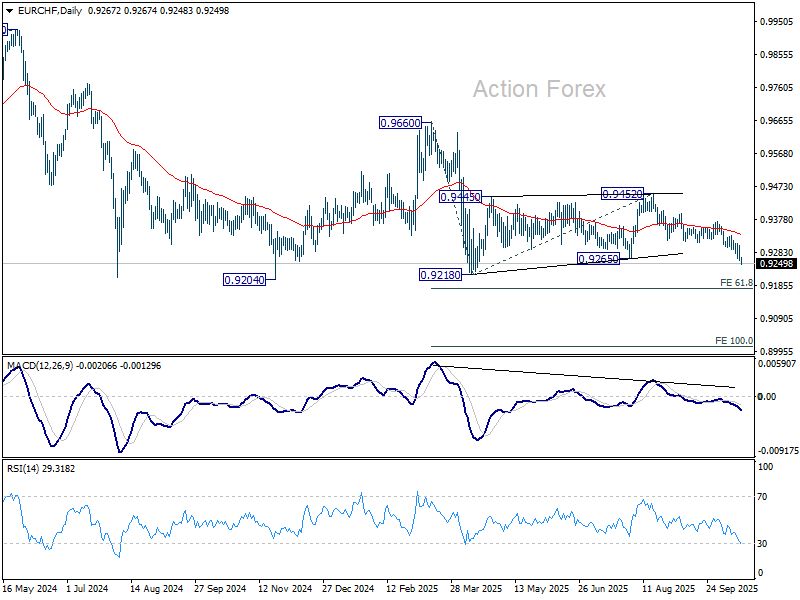

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9249; (P) 0.9277; (R1) 0.9293; More…

EUR/CHF’s is still in progress and intraday bias stays on the downside. Current development suggests that consolidation from 0.9218 has completed with three waves to 0.9452, and larger down trend is resumption. Further fall should be seen through 0.9204/18 support zone to 61.8% projection of 0.9660 to 0.9218 from 0.9452 at 0.9179 next. On the upside, above 0.9303 minor resistance will turn intraday bias neutral first.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. Bearishness is reaffirmed by rejection at 55 W EMA (now at 0.9405). Firm break of 0.9204 will confirm down trend resumption. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851.