Wall Street Finds Footing After Bank Rout, but Conviction Still Lacking – Action Forex

As markets enter into U.S. session, sentiment showed signs of stabilization, as investors cautiously stepped back into equities after a sharp selloff in regional banks yesterday. Concerns over credit quality and loan losses had triggered a steep decline in financial stocks, but bargain-hunting helped bank shares rebound, lifting broader index futures in premarket trading. The recovery suggests investors see the recent slump as overdone for the immediate term.

Still, sentiment remains cautious and directionless, with traders reluctant to take bold positions amid a backdrop of multiple macro headwinds — including the U.S. government shutdown, trade friction with China, and geopolitical uncertainty. The market’s current tone suggests consolidation rather than conviction, as participants wait for clearer signals on both policy and economic momentum before re-engaging.

In the currency markets, performance remains consistent with a cautious, risk-off tone. The Swiss Franc continues to lead the week as the strongest major currency, followed by Sterling and Yen, while Loonie lags behind. Dollar and Kiwi are also under pressure, with Aussie and Euro trading mid-range.

In Europe, at the time of writing, FTSE is down -0.96%. DAX is down -1.42%. CAC is up 0.02%. UK 10-year yield is up 0.044 at 4.546. Germany 10-year yield is up 0.013 at 2.588. Earlier in Asia, Nikkei fell -1.44%. Hong Kong HSI fell -2.48%. China Shanghai SSE fell -1.95%. Singapore Strait Times fell -0.63%. Japan 10-year JGB yield fell -0.026 to 1.631.

BoE’s Pill: Risk of self-sustaining inflation calls for more cautious pace in cuts

BoE Chief Economist Huw Pill said today that the UK’s inflation remains far stickier than expected, reinforcing the case for a slower pace of monetary easing.

In a speech, Pill noted the “lack of progress” in reducing inflation as “disappointing”. He cautioned that the persistence of above-target inflation, combined with heightened sensitivity among firms and households to price developments, risks creating “self-sustaining inflation dynamics”. The prominence of food prices, which directly affect household perceptions of inflation, could further embed inflation expectations if not carefully managed.

This, he argued, calls for a “more cautious pace in withdrawing monetary policy restriction so as to ensure continuation in disinflation towards the 2% target.” While Pill reiterated that future rate cuts remain likely over the next year if the outlook evolves as expected, he stressed the importance “to guard against the risk of cutting rates either too far or too fast.”

Eurozone CPI finalized at 2.2%, driven by services and food prices

Eurozone inflation edged higher in September, with headline CPI finalized at 2.2% yoy, up from 2.0% in August. The core measure, which excludes energy, food, alcohol & tobacco, also firmed to 2.4% yoy from 2.3%.

The main driver of the increase came from services, which contributed +1.49 percentage points to the annual rate, followed by food, alcohol, and tobacco (+0.58 pp), and non-energy industrial goods (+0.20 pp). Energy continued to be a drag, subtracting -0.03 pp.

Across the broader European Union, annual inflation was finalized at 2.6% yoy, up from 2.4% in August, with wide divergence among member states. Cyprus (0.0%), France (1.1%), and Italy and Greece (1.8%) recorded the lowest rates, while Romania (8.6%), Estonia (5.3%), and Croatia and Slovakia (4.6%) posted the highest. Inflation fell in 8 countries, was stable in 4, and rose in 15.

Ueda signals watchful patience as BoJ weighs October policy options

BoJ Governor Kazuo Ueda reiterated overnight that the central bank will consider rate hikes “if our confidence in hitting the outlook increases”. He added that he intends to continue gathering informations before making any decisions at the October 29–30 policy meeting.

Ueda observed that G20 members regard the world economy as broadly stable but facing persistent risks, from trade disputes to geopolitical frictions. “Many institutions and observers still factor them into their outlooks, or at least treat them as downside risks when assessing the global and U.S. economies,” he said.

BoJ’s Uchida: Further hikes if outlook holds

BoJ Deputy Governor Shinichi Uchida said in a speech on today that the central bank remains prepared to raise interest rates further if its current projections for growth and inflation are realized. He emphasized that the BoJ will “judge without any pre-conception” while monitoring both domestic and global conditions.

Uchida highlighted rising uncertainty surrounding overseas economies, particularly due to shifting trade policies that could influence Japan’s external demand and price trends. “It’s necessary to closely monitor how these developments may affect financial and foreign exchange markets, as well as Japan’s economy and prices,” he said.

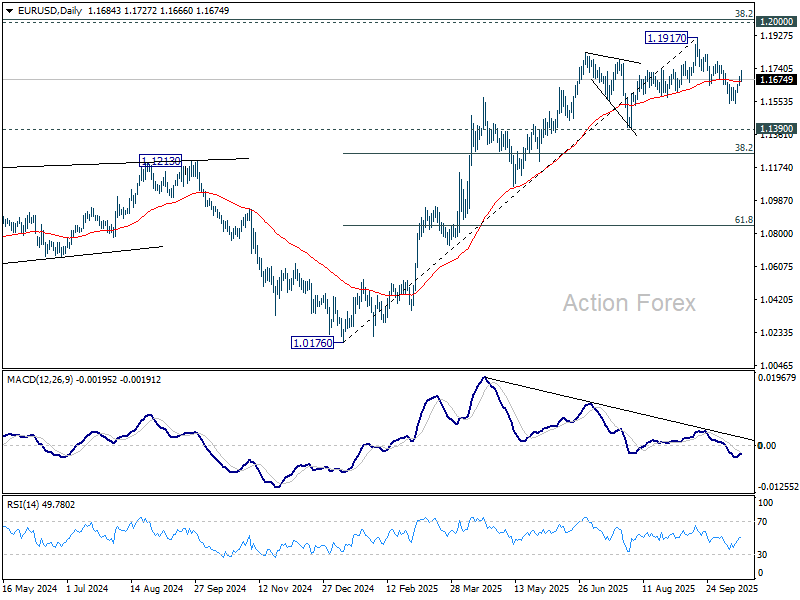

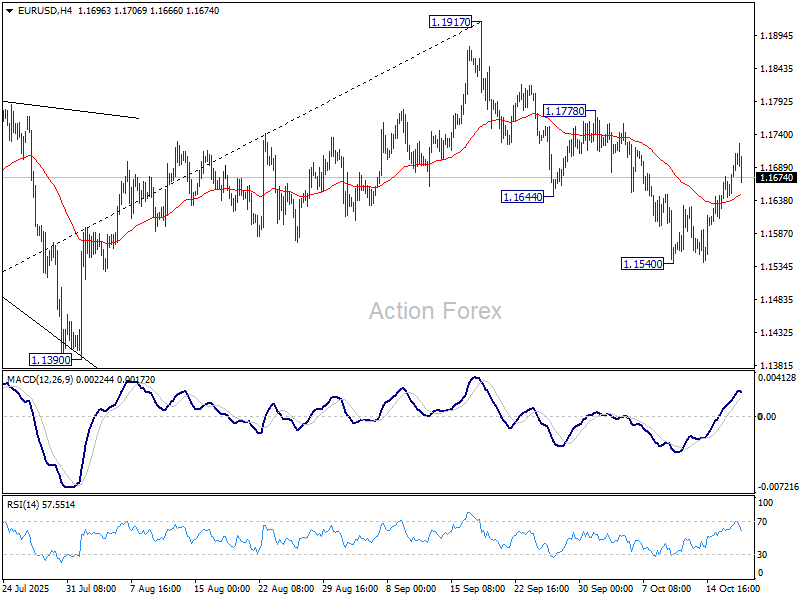

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1655; (P) 1.1675; (R1) 1.1706; More…

EUR//USD retreated well ahead of 1.1778 resistance and intraday bias stays neutral. Further decline is still expected with 1.1778 resistance intact. On the downside, break of 1.1540 will resume the fall from 1.1917 to 1.1390 , or further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. However, firm break of 1.1778 will suggest that pullback from 1.1917 has completed, and bring retest of this high.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1274) holds, the up trend from 0.9534 (2022 low) is still extended to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.