Dollar Slips as Softer Core Inflation Reinforces Bets on Two More Fed Cuts This Year – Action Forex

Dollar eased in early U.S. session after the latest inflation report came in slightly softer than expected, reinforcing expectations of continued monetary easing by the Fed. The pullback was modest, but sentiment turned more dovish as traders focused on the dip in core inflation, which may be seen as evidence that price pressures have peaked during the summer. While still early to call a full victory on inflation, the data injected a sense of guarded optimism into markets.

Rate expectations shifted quickly, with futures markets now nearly fully pricing a December rate cut following next week’s anticipated 25bps reduction. Fed funds futures indicate a 99% probability that policy rates will be lowered to the 3.50–3.75% range by year-end.

Elsewhere, U.S. stock futures rose modestly after the release, buoyed by expectations of a friendlier rate environment. DOW edged closer to its record highs, though whether buying momentum can sustain through the session remains to be seen. Meanwhile, Treasury yields tumbled, with the 10-year yield falling back sharply after briefly testing 4.0%, signaling that the market may have just given its final “kiss goodbye” to that level for now.

In commodities, Gold staged a modest recovery, continuing to defend the 4,000 mark despite muted momentum. The metal remains supported by lower yields and lingering geopolitical concerns, though traders appear hesitant to extend the rally until the Dollar’s next clear directional move.

Across the currency markets, commodity-linked currencies continue to lead weekly performance — Kiwi remains the strongest, followed by Aussie and Loonie. Yen stays under broad pressure, trailed by Sterling and Euro. Dollar and Swiss Franc are holding mid-pack, though momentum suggests Dollar could slide further before the weekly close if risk appetite persists.

In Europe, at the time of writing, FTSE is up 0.12%. DAX is up 0.21%. CAC is down -0.34%. UK 10-year yield is down -0.02 at 4.415. Germany 10-year yield is up 0.03 at 2.619. Earlier in Asia, Nikkei rose 1.35%. Hong Kong HSI rose 0.74%. China Shanghai SSE rose 0.71%. Singapore Strait Times rose 0.13%. Japan 10-year JGB yield fell -0.002 to 1.659.

US CPI rises to 3.0%, but Core eases, both miss expectations

US inflation ticked higher in September, but the details of the report suggested price pressures are cooling beneath the surface. Headline CPI accelerated to 3.0% yoy, up from 2.9% but slightly below expectations of 3.1%. That marks the highest level since January.

Though, core CPI — excluding food and energy — slowed from 3.1% to 3.0%, undershooting forecasts and easing from 3.1% in the previous two months. After holding at 3.1% for two consecutive months, the core rate could be entering into a gradual downtrend.

On a monthly basis, headline prices rose 0.3% mom, while core prices increased just 0.2%, both softer than expected. Energy costs were again the key driver of the headline gain, with the gasoline index surging 4.1% and the broader energy index up 1.5%. Food prices also continued to edge higher, rising 0.2% as grocery costs climbed more sharply than dining-out prices.

UK PMI composite improves to 51.1, but indicates just sluggish 0.1% GDP growth

The latest UK flash PMI data offered a glimmer of optimism for the economy, with Manufacturing jumping from 46.2 to 49.6 in October — its highest level in 12 months. Services rose from 50.8 to 51.1, lifting the Composite index from 50.1 to 51.1. The survey suggests business conditions are slowly improving after a soft September, marking the first sign of renewed momentum since midyear.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, said the data “brings hope that September was a low point,” noting the first manufacturing growth in over a year and stronger consumer demand for services. He added that inflationary pressures are easing back toward levels “consistent with the Bank of England’s 2% target,” while job losses are moderating and business confidence is ticking up slightly.

Still, the overall pace of expansion remains modest, consistent with GDP growth of only about 0.1%. Export weakness persists due to global trade disruptions tied to U.S. tariff policy. Firms are also cautious ahead of the November 26 Budget, with many delaying hiring and investment decisions. While the PMI data point to stabilization, the recovery remains fragile and heavily dependent on fiscal clarity and external demand.

UK retail sales rise 0.5% mom in September, hitting highest level mid-2022

UK retail activity surprised to the upside in September, with sales volumes rising 0.5% mom, defying expectations of a -0.2% mom decline. The gain marked the fourth consecutive monthly increase, lifting total sales to their highest level since July 2022. Stronger non-store and clothing sales helped offset weakness in fuel and other discretionary categories.

Over the third quarter, retail volumes grew 0.9% compared with the previous quarter, confirming a steady rebound in household demand through the summer. The good weather in July and August was cited as a key driver, boosting clothing sales and supporting outdoor-related spending. Online and non-store retailers also enjoyed sustained gains.

Eurozone PMI composite hits 17-mont high, services lead while France drags

Eurozone business activity accelerated in October, with PMI Composite rising to a 17-month high of 52.2 from 51.2, signaling the strongest expansion since mid-2024. The pickup was driven by services, where PMI Services index jumped from 51.3 to 52.6, a 14-month high, while Manufacturing finally edged up to the neutral 50.0 mark after months of contraction.

However, the upturn remains uneven across major economies. Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that France has increasingly become a drag, with its rate of contraction accelerating for two straight months amid political turmoil and budget disputes under Prime Minister Sébastien Lecornu. In contrast, Germany’s outlook “brightened significantly”, helping to lift the bloc’s overall figures. Still, manufacturing has been “stagnating for practically six months,” de la Rubia said, and weak new orders leave “little hope of a turnaround.”

Inflation trends offer some comfort for policymakers. Price pressures in the services sector — a key focus for the ECB — “remain moderate,” with sales price inflation slightly higher but still near long-term averages. The PMI data are therefore unlikely to alter the ECB’s cautious stance, reinforcing expectations that officials will hold off on further rate cuts until clearer signs of sustained disinflation emerge.

Japan CPI core Rises to 2.9%, ending three-month slowdown

Japan’s inflation picked up in September, with core CPI (excluding fresh food) rising from 2.7% to 2.9% yoy, matching expectations and marking the first acceleration in four months. The key gauge has stayed at or above the BoJ’s 2% target since April 2022. Headline CPI also rose from 2.7% to 2.9% yoy, in line with the core measure.

Underlying momentum was uneven. Core-core CPI, which strips out both energy and fresh food and is considered a closer measure of domestic demand, slowed to 3.0% from 3.3% yoy, suggesting that broader inflationary pressures are gradually easing.

Food prices continued to rise, but at a slower pace — non-fresh food prices gained 7.6%, down from 8.0% in August. Rice prices, which spiked earlier this year, rose 49.2%, their fourth consecutive month of deceleration after peaking at more than 100% growth in May.

Meanwhile, service prices, a metric closely watched by the BoJ for its link to wage growth, increased 1.4%, slightly below August’s 1.5%.

Japan PMI composite falls to 50.9, weak Yen keeps inflation hot

Japan’s private sector lost further momentum in October, with both manufacturing and services activity softening, according to S&P Global’s Flash PMI survey. The Manufacturing PMI slipped from 48.5 to 48.3, extending its contraction, while Services PMI fell from 53.3 to 52.4. As a result, Composite index eased from 51.3 to 50.9, signaling the slowest pace of overall growth since May.

Annabel Fiddes, Economics Associate Director at S&P Global Market Intelligence, said the survey showed the first decline in new business in 16 months. While the services sector remained the key driver of growth, its fading strength “will be a point of concern” as manufacturing continues to struggle. The factory sector’s downturn deepened, with new orders falling at the fastest pace in 20 months.

Inflationary pressures, however, remained elevated. Both input costs and output charges continued to rise at historically strong rates, driven by higher wage, fuel, and material costs, and alongside by a weaker Yen.

Australia PMI composite ticks up to 52.6, easing inflation keeps RBA on easing track

Australia’s private sector activity sent mixed signals in October, according to the S&P Global Flash PMI survey. Manufacturing PMI slipped back into contraction, falling from 51.4 to 49.7, while Services PMI rose to 53.1 from 52.4, lifting the Composite PMI modestly from 52.4 to 52.6. The data suggest that overall business activity grew at a slightly faster pace at the start of Q4, though the underlying picture remains uneven across sectors.

According to Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, the divergence between sectors was striking. Manufacturing “notably worsened,” with new orders dropping further and factories shedding jobs amid pressure on profit margins.

In contrast, services activity expanded at a solid pace, but even there, new business growth and hiring momentum slowed, and business confidence weakened.

On a positive note, price pressures continued to ease, with output price inflation falling to a five-year low. This cooling in inflation dynamics should reassure the RBA, which remains on track to pursue further monetary easing.

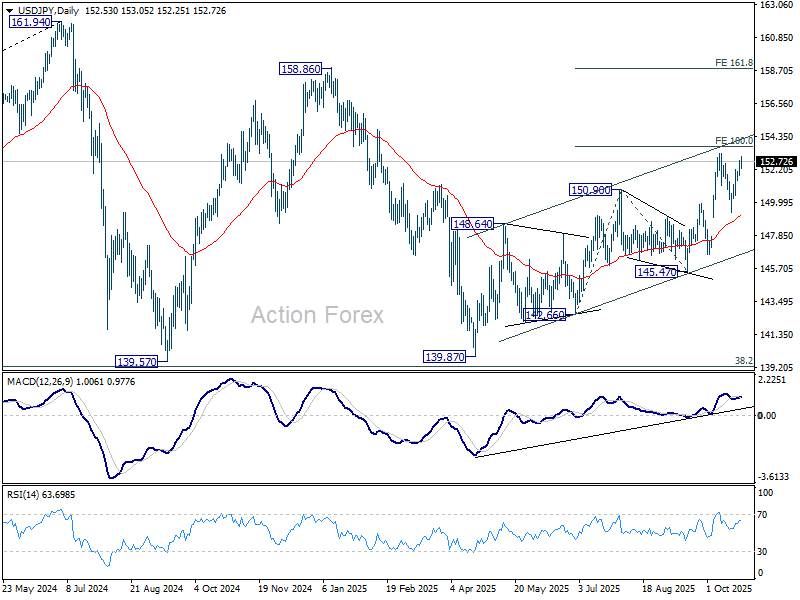

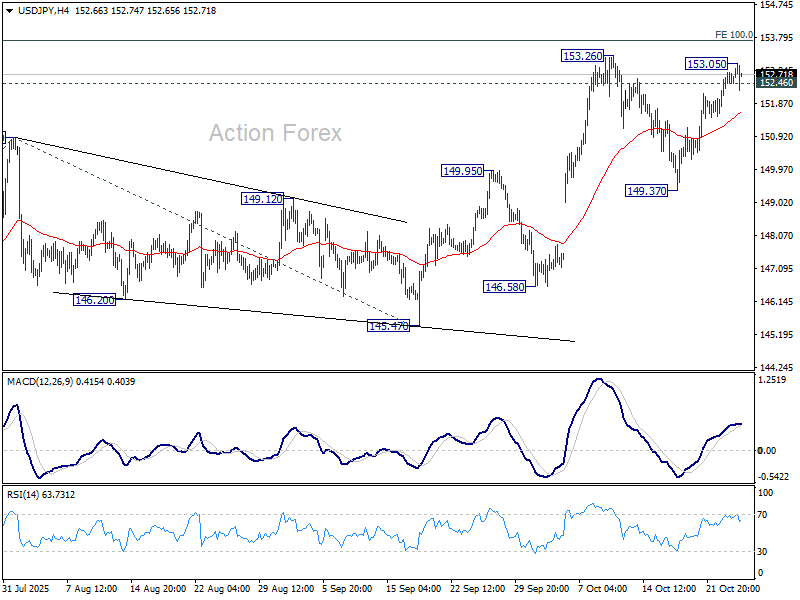

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.01; (P) 152.40; (R1) 152.99; More…

Intraday bias in USD/JPY is turned neutral with current retreat, and some consolidations would be seen. Another rise is in favor as long as 55 4H EMA (now at 151.56) holds. Above 153.05 will target 153.26, and then 100% projection of 142.66 to 150.90 from 145.47 at 153.71. Firm break there would prompt upside acceleration to 161.8% projection at 158.80.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.